Investing in Europe #10

Investing in Europe #10

Just Eat Takeaway, Adidas, Domino’s Pizza Group, Burberry and others

Welcome back to Investing in Europe, a weekly newsletter on what’s happening in European companies and markets, filtered for what matters. Welcome to new subscribers! 🥂 Your feedback is welcome. You can find me on Twitter.

If you are not a subscriber, please sign up to get full access and never miss an update.

If you are a subscriber and like what you read, please share it to a friend. Thanks! 🙏

This is the 10th edition of IIE. I want to thank all the readers who joined me in this new project. I started this newsletter as a place to organise and share some of my high level thoughts on European companies. A sort of investor’s diary. We are in the early days and I am still thinking about the best format: I might do a light version on weekends and some deep dives once in a while. What would you find most interesting? Send me your comments at @AnalystInvestor - DM open. Thank you!

Company results

It has been another busy week, full of companies reporting their earnings. Let’s have a look at a few interesting results:

Just Eat Takeaway (TKWY), the global online food delivery company with a leadership position in Europe, delivered a very confident FY20 results presentation.

First message: TKWY wants to consolidate its leadership position in Europe and is investing in logistic to regain market share in underinvested Just Eat legacy markets. They expect order growth to accelerate in 2021, compared to the +42% reported in 2020. This is not an easy statement to make in March, especially after a lockdown year. Restaurants were mostly closed and we ordered more food at home. TKWY is investing in growth: they are using the resources from the high margin and cash flow marketplace business to finance a massive expansion in logistic, especially in markets were they have been losing share. First of all the UK, and in particular London where they are planning to aggressively expand Scoober, their own delivery service. The share of delivery orders increased from 18% to 26% in 2020. This is not a marketplace business anymore, but a hybrid model. It probably will not be as profitable as we imagined a few years ago, at least in the short term, but will have a bigger addressable market. TKWY is positioning itself as the most attractive price-value option, offering lower than peers delivery fees (zero in some cases), while onboarding new restaurants.

Second message: we should probably update our SOTP valuation. TKWY disclosed they received several bids for its 33% stake in iFood (Brazil): the highest amounted to €2.3bn. The stock was one of the top 10 best performers in Europe this week.

Adidas had a capital market day. The company expects revenues to increase 8-10% pa in 2021-2025, and operating margins to reach a level between 12-14%. There will be a further push to a DTC-led business model, with a 50% target by 2025. E-commerce sales should double from more than €4bn last year. Sustainability was another key topic, as they expect 9 out of 10 articles to be made from sustainable materials by 2025.

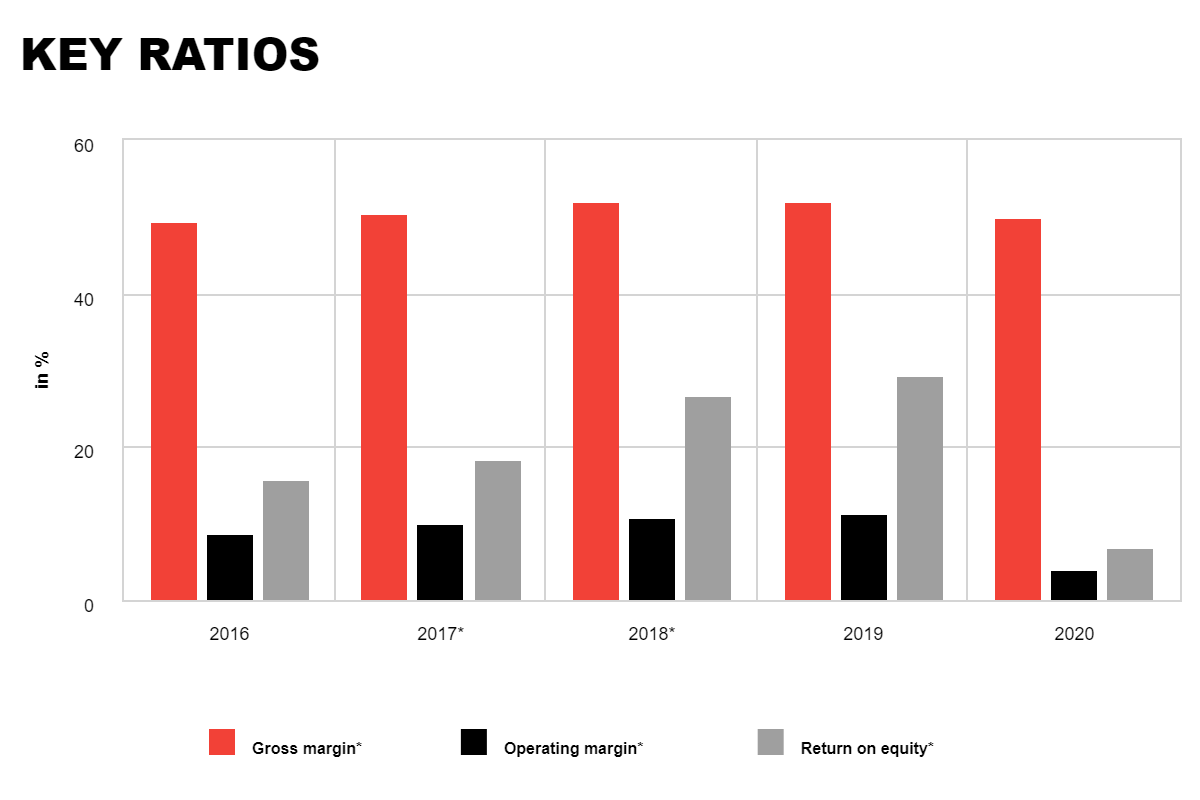

How they did in 2016-2020:

Pandora, the jewellery company, released a trading update. The number of stores closed due to COVID-19 decreased to around 25% at the end of February. Total sell-out growth was +7%. In 2021, they expect organic growth above 8% and EBIT margin above 21%.

JDE Peet’s, the coffee company which IPOed last year from a combination of Peet’s Coffee with JDE, reported its FY20 results. They “adjusted” their medium to long term targets downward: EBIT is expected to growth mid-single-digit from 5-8% before. Not the message you want to give less than a year after the IPO. 2021 EBIT growth is expected to be even lower, at low single-digit. 🤷♂️

Symrise, the flavours and fragrances producer, expects sales growth of 5 to 7 % and EBITDA margin of around 21 % (link)

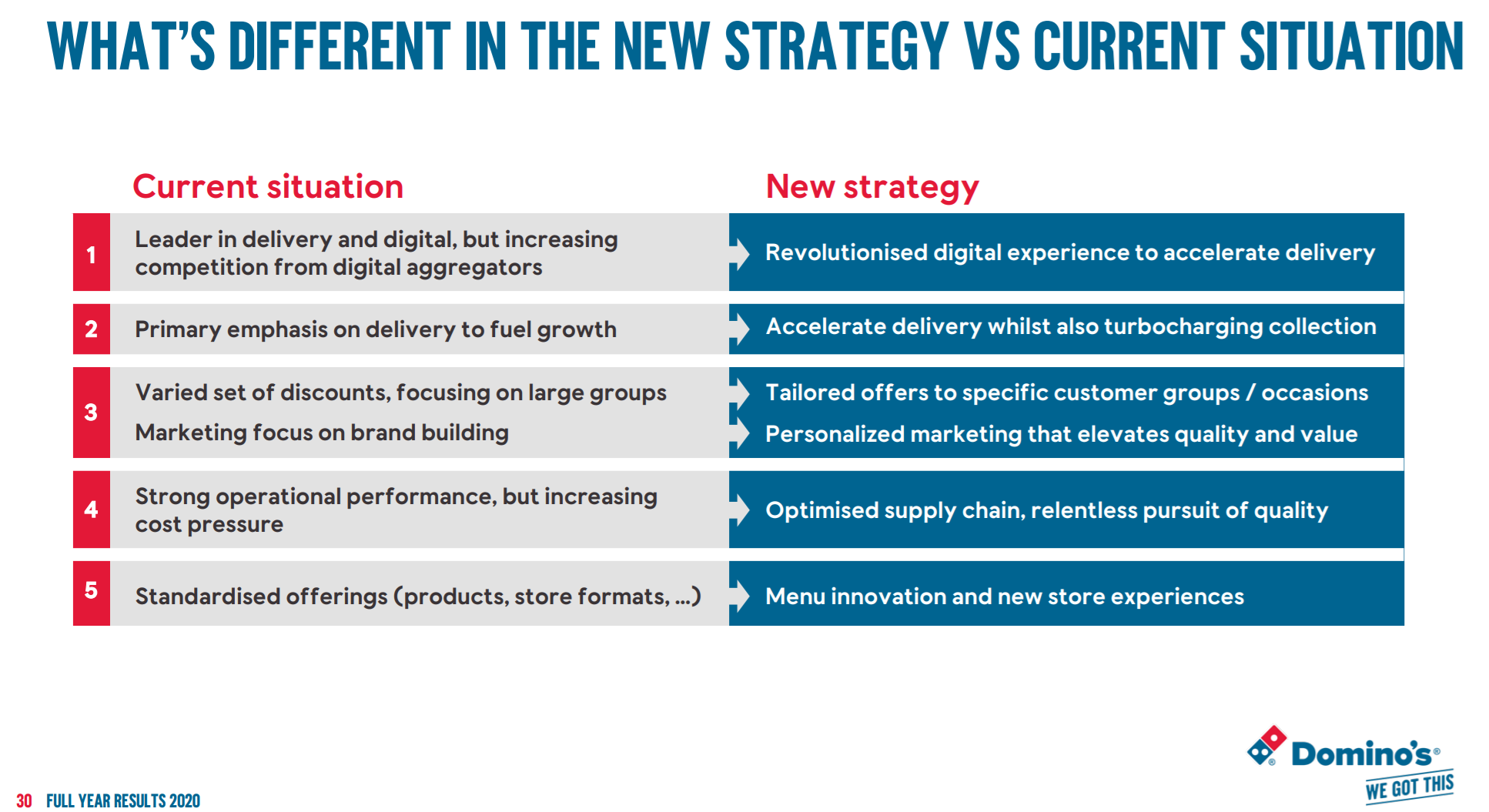

Domino’s Pizza Group, the UK master franchise of Domino’s Pizza, reported a +11.4% LfL system sales growth. They also introduced a new strategy focused on accelerating growth, with ambition to deliver £1.6bn -£1.9bn of system sales. DPG had some issues with its franchisees in the UK in the past. They “made an attractive offer to Domino’s franchisees to seek alignment & accelerate growth” which means they are still working on an agreement. Finally, as part of the planned exit from the (underperforming) international markets, they also announced the disposal of their Sweden business.

Continental Sees Muted Returns on Chip Shortage, Pandemic (Bloomberg link). The stock was one of the worst performer in Europe this week.

Dufry, the global travel retailer, reported an organic decline of almost 70% in 2020 due to the pandemic. 55% of stores were open as of the end of February.

Burberry, the British luxury company, issued a positive trading update ahead of its FY20 results:

Since December, we have continued to see a strong rebound and now expect revenue and adjusted operating profit to be ahead of consensus expectations. Comparable store retail sales in Q4 FY2021 are expected to be in the range of +28% to +32% higher than the same period last year. For the full year, we expect group revenue to decline by -10% to -11% and the adjusted operating margin to be in the range of 15.5% to 16.5%.

The stock was one of the top 10 best performers this week in Europe.

M&A and IPO

Diageo acquires the Lone River Ranch Water brand (link)

EssilorLuxottica Bid for GrandVision Poised for EU Approval (link)

Exor snaps up 24 percent stake in Christian Louboutin (link)

Vodafone Seeks $2.4 Billion From Vantage Towers IPO (link)

And of course, Deliveroo IPO (see also TKWY above)

Have a great week and good investing!

Disclaimer: this newsletter is for informational purposes only and does not represent investment advice. I might have a position in some of the stocks discussed. Always do your own research before investing.