Investing in Europe #11

Investing in Europe #11

Volkswagen, Zalando, Fever-Tree and others

Welcome back to Investing in Europe, a weekly newsletter on what’s happening in European companies and markets, filtered for what matters. Welcome to new subscribers! 🥂 Your feedback is welcome. You can find me on Twitter.

If you are not a subscriber, please sign up to get full access and never miss an update.

If you are a subscriber and like what you read, please share it to a friend. Thanks! 🙏

Companies news and results

Volkswagen, the second largest carmaker by sales after Tes… Toyota, presented its EV and battery strategy at the “Power Day” event. Volkswagen aims to sell 1mn electric vehicles this year, almost 10x compared to 2019, and to be the global market leader for electric mobility by 2025. With its partners, the German carmaker plans to build six cell (giga?)factories by the end of the decade, with a total capacity of 240 gigawatt hours. They expect the share of all-electric vehicles in Europe to rise to up to 60 % by 2030.

Volkswagen is outperforming Tesla since its CEO Herbert Diess joined Twitter 😀

To be fair, I should have used the more liquid preferred shares which were up +33% in the same period, but it is still quite a big gap. The price action in the ordinary shares is reminiscent of the mother of all squeezes that happened in 2008, when Volkswagen became the most valued listed company. This time, US retail investors seem to be involved, as volume in the ADR was nearly 12 times the 90-day average on Tuesday.

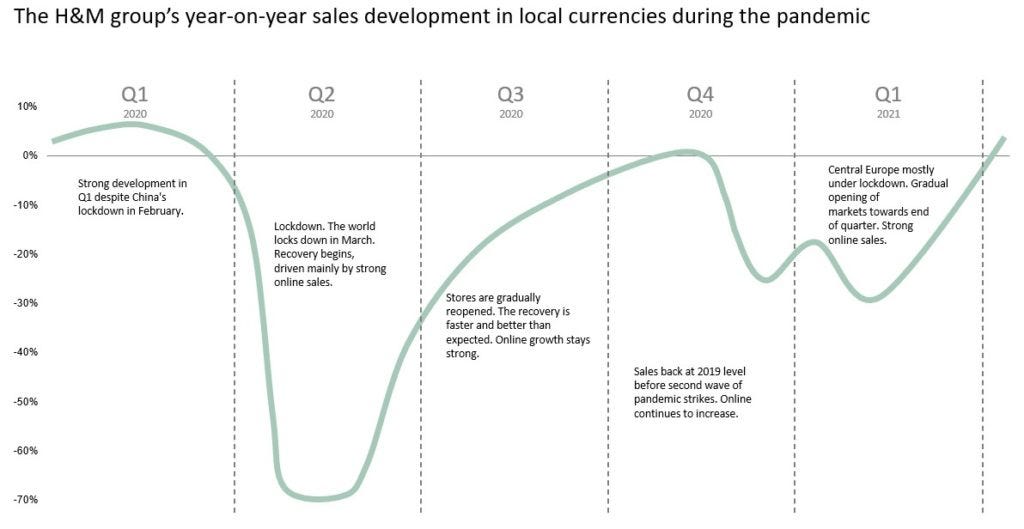

H&M released a trading update for its Q121 (Dec-Feb). Net sales decreased by 21% in local currencies as the business is still impacted by the pandemic:

Zalando, the German e-commerce company, had a CMD: they target more than €30bn GMV by 2025, which means a 23% CAGR from last year. Also, “the company aspires to serve more than 10% of the total EUR 450 billion European fashion market in the long-term”. Zalando reached 38.7mn active customers last year, up 25% from 2019. There is a list of new countries they are entering. No mention of the UK, where they are willing to expand. The marketplace offer, Partner Program, accounted for 24% of Zalando’s fashion store GMV last quarter and has more than 3400 stores as of last month.

Fever-tree, the British producer of premium drink mixers, “disappointed” market expectations with its 2021 guidance. The company expects revenues to grow +12-16% compared to -3% in 2020. That was ok. EBITDA margin is expected flat, after a 700bps drop in 2020. Consensus was expecting a recovery. There were plenty of one-offs and mix impacts. In terms of growth, the long term trends remain supportive: increasing spirits penetration, premiumisation, low penetration ex UK - they could growth 5x in the US.

Ocado Retail, the UK online grocer division of Ocado, issued a trading statement: revenues accelerated to +40% in the last 13 weeks, driven by a 36% increase in average basket size to £147. This is expected to normalise and comps will get tougher. The first UK lockdown was one year ago. Ocado expects a permanent shift to online grocery and is ramping up UK capacity by 40%. Finally, the call was hijacked 🙉:

Emmanuel Faber started the year as Danone’s CEO and Chairman. Under activists pressure, disappointed with the share price performance, he stepped down as CEO earlier this month but remained as chairman. That was not enough, as this week he was ousted by the board and left the company with this message on Linkedin:

Huge thank you to all my dear teams and all the people at Danone for « living » its unique mission every day. For 24 years of my life, you made me grow among you all, as a person and as a leader. It has been a privilege. Stay true to yourself. You rock. Proud of Danone.

Hargreaves Lansdown issued a trading update: similar to previous lockdown periods, trading volumes remain elevated and they expect June 2021 PBT to be modestly above the top end of analyst expectations (£360mn). This time they mentioned interest in US stocks, which is higher margin as they have a 1% FX fee.

Swedish Match published its annual report 2020. A few points:

The smokefree division is 72% of EBIT. ZYN nicotine pouches I think 1/4 ca

Smokefree EBIT doubled in 4 years and operating margins improved +730bps

ZYN reached 130mn cans worldwide: 114mn int the US, 13mn in Scandinavia

It is sold in 116k stores ex Scandinavia, from 79k last year. 100k stores in the US

Smokefree volumes in relation to cigarettes increased to 2.6% in the US, 75.3% in Sweden + Norway combined. Cigarettes went from ca 90% to 85% of total tobacco consumed globally last year

Swedish Match bought back 260.2 million shares since its share buyback program started in June 2020, at an average price of 148.08. A 64% reduction in shares. Current price is a devilish 666 so 4.5x times the average SBB price.

Other news

Uber Grants 70,000 U.K. Drivers Worker Rights After Ruling (Bloomberg)

Trading platform eToro to go public via SPAC merger in $10B deal (TechCrunch)

Gucci Is Selling $12 (Virtual) Sneakers (BoF) - I say too cheap. These digital sneakers sold out for $10k 😀

EU and AstraZeneca:

Vaccine rollouts - it will not be a normal summer in Europe at this pace:

A good thread on what happened with vaccines in the EU:

Have a great week and good investing!

Disclaimer: this newsletter is for informational purposes only and does not represent investment advice. I might have a position in some of the stocks discussed. Always do your own research before investing.