Investing in Europe #14

Investing in Europe #14

Prosus, HomeServe, Deutsche Post and more

Welcome back to a new issue of Investing in Europe, a weekly newsletter on what’s happening in European companies and markets, filtered for what matters.

Welcome to our new subscribers! 🥂 Your feedback is welcome, please DM me on Twitter.

If you are not a subscriber, please sign up to get full access and never miss an update.

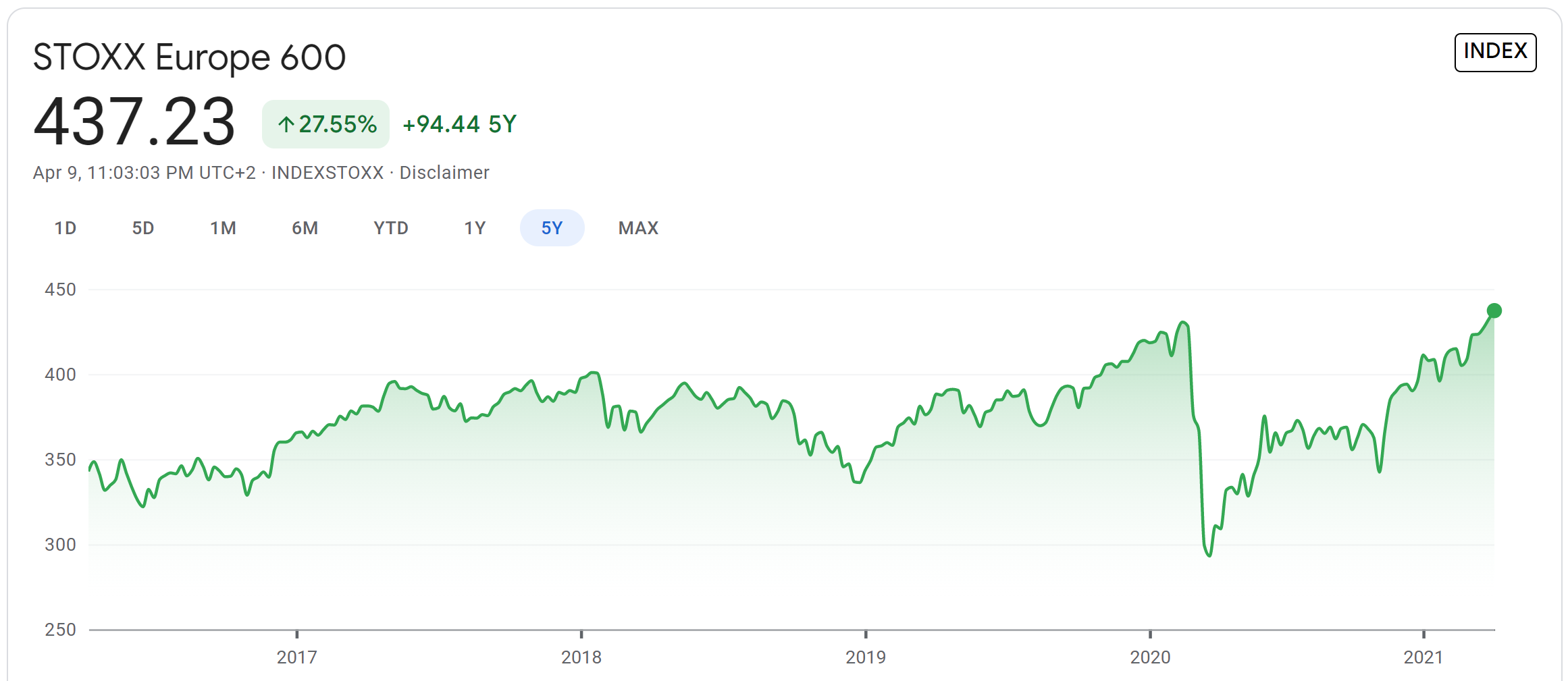

New high 📈

European stocks erased the pandemic's losses and reached new high this week.

It is a good time to post a long term chart:

A few points:

I remember last year people were arguing about the shape of the post-pandemic recovery: V-shape, U, L or some other letter-shaped. One year later we can say it looks like a W, somewhat. Case closed

On a more serious note, while celebrating the new high we should remember how we got here. Most countries and central banks reacted strongly and quickly to avoid a depression. Less so on containing the virus’ spread, sadly

It took 13 months for European markets to recover. Only 5 for the US. UK is still below pre-Covid peak

Company news and results

Prosus reduced its stake in Tencent from 30.9% to 28.9% ca, raising around $15bn.

Prosus intends to use the proceeds of the sale to increase its financial flexibility to invest in growth ventures, plus for general corporate purposes

Markets speculated this could mean food delivery. Just Eat Takeaway (JET) was strong this week. Prosus made an offer to buy Just Eat in late 2019, before Just Eat decided to merge with Takeaway.com. They are also invested in other food delivery companies: Delivery Hero, Swiggy and iFood - a leader in online food delivery in Latin America. JET has a 33% stake in iFood and received several bids for it, the highest was €2.3bn as reported in JET’s FY20 results. Prosus has been rumoured to be interested in buying that stake.

It could mean classifieds as well, another area where Prosus has been investing - and lost another M&A battle last year, to Adevinta.

HomeServe, the international home repairs and improvements business, issued a trading update. They expect adjusted profit before tax to be around £191mn in their financial year ended March 2021, which is +5.5% on 2020. This is in line with current market expectations. The Membership business, which sells policies that cover home repairs, saw customer growth of +7% to 4.7mn in North America, while UK customers decreased from 1.8mn to 1.6mn as the company is rationalising their client base. Checkatrade, the home experts marketplace, finished the year with +13% trades compared to last year.

Beiersdorf expects its Q1 to be above market expectations. Sales increased 6.3% in the first three months of the year. The consumer business (Nivea & co) was up 2.7%, while the self-adhesive business tesa +23.6%, as its industrial business is recovering. Beiersdord left its FY21 guidance unchanged. The guidance disappointed investors when it was released, mainly on profitability, which is expected to be in line with last year. Margin has been declining for a while.

Ryanair is cautious on this year recovery. FY22 traffic (which means March for them) is expected to be at the bottom end of their 80mn to 120mn passengers guidance. March traffic was down 91% due to travel restrictions around Europe.

we do not share the recent optimism of certain analysts as we believe that the outcome for FY22 is currently close to breakeven

Airlines are not a great business, but there are a few exceptions. Ryanair is one of the most efficient player in Europe. If Ryanair will be only close to breakeven, imagine how profitable could be those nice legacy carriers trading above pre-Covid peak. Air France is getting more money from the French government.

Asos reported its interim results for the first half of its financial year. Revenues increased 25%, with UK +39%. They expect FY21 to be in line with the first half. Margins improved thanks to some Covid benefits, including lower distribution and warehousing costs (lower return rates). They are in the process of integrating Topshop, a brand they bought from Arcadia’s collapse.

Deutsche Post reported its strongest first quarter ever and raised its guidance, for the third time. They experienced “sustained momentum in e-commerce and a significant stabilization in global trade”. It is a combination of booming e-commerce, recovering B2B and lower capacity. There is still a shortage of air cargo and DHL coltrols the largest airfreight capacity out there. Group EBIT tripled compared to last year.

M&A and IPO

Amundi Buys SocGen’s Lyxor in Bid To Reshape Europe’s ETF Sector (Bloomberg)

Goldman bought 75 million pounds of Deliveroo shares to prop up IPO price (Reuters) - its sounds bad but they basically bought half of the greenshoe, which was 10% of the offer. It is standard practice. Still, it was an awful IPO

Swedish online real estate firm Hemnet plans Stockholm IPO (Reuters)

Allfunds eyes Euronext Amsterdam IPO (IW)

Other news

Credit Suisse axes bosses and bonuses amid Archegos losses (BBC)

Sodexo and Uber Eats sign a partnership: if you are in France, you can pay on Uber Eats with your meal card

England's pubs, restaurants and shops prepare for Monday reopening (Yahoo) 🍺

Have a great week and good investing!

If you are not a subscriber, please sign up to get full access and never miss an update.

Disclaimer: this newsletter is for informational purposes only and does not represent investment advice. I might have a position in some of the stocks discussed. Always do your own research before investing.