Investing in Europe #17

Investing in Europe #17

Logistics, Dental Implants, Nicotine pouches, Condoms and more

Welcome back to a new issue of Investing in Europe, a weekly newsletter on what’s happening in European companies and markets, filtered for what matters. Welcome to our new subscribers! 🥂 Your feedback is welcome, please DM me on Twitter 🙏

If you are not a subscriber, please sign up to get full access and never miss an update.

Company news and results

It has been another busy week of results. We start with a sector that is not mentioned much as a Covid beneficiary: freight-forwarding. It has really boomed during the pandemic, thanks to a sustained strong demand coupled with disrupted supply chains. Freight-forwarding is a fragmented industry with some strong European players at the top. It is also one of those low margin / high turnover businesses which are able to generate high returns.

Kuehne+Nagel’s EBIT more than doubled in Q121 compared to last year, mostly thanks to extraordinary high margin. Conversion rate (EBIT/GP) went from 9.8% to 21.3% in 12 months, thanks to low containers/freight capacities, poor terminal productivity and good demand. Working capital remained relatively stable on an absolute basis, so return on capital exploded:

Similar story at DSV Panalpina: strong profits and guidance upgrade. More importantly, they announced the acquisition of Agility GIL for $4.1bn equity ($4.2bn EV) in an all-share deal. That’s 23.2x LTM EBIT or almost 1x sales. DSV is an M&A machine and bought a few businesses at cheaper multiples in the past, but Agility GIL seems better quality than average. DSV will become the number three player globally with $21.7bn revenues, up 2.5x from 2014 level (pre UTi acquisition).

These are both good companies but clearly overearning at the present time. Note that logistics disruptions are not only causing record-high profitability:

Moving to other sectors, Reckitt, the company of Dettol, Lysol and Durex condoms, reported a +4.1% increase in sales in the first quarter of 2021. Hygiene, the biggest division, grew +28.5% as demand remains robust. The pandemic is still here. The other two divisions, Health and Nutrition, reported negative growth. Health is impacted by lower demand for cold and flu products (no standard flu). Durex condoms delivered double-digit revenue growth, led by China, as restrictions are easing ❤️. Nutrition, which includes infant formula, has been impacted by border closure in Hong Kong / Mainland China and significantly lower birth rates. Ecommerce increased to 13% of group sales. Reckitt had an extraordinary year in 2020 and will experience tough comps in 2021: they “expect like-for-like revenue growth of between flat to +2%”.

Symrise reported a +10.5% increase in sales in Q1 2021. This is not their normal growth rate unfortunately. The company was impacted by a cyber-attack last December and had to do some catch-up. Q4 2020 growth was only +0.7%. The FY21 guidance is 5 - 7% organic growth, which is still fine for a defensive business. The Scent & Care division (fragrances, aroma molecules and cosmetic ingredients) grew +8.3%. The Flavor segment (food and beverages) was up +9.1%, while Nutrition (food, pet food, probiotics) grew +16.1%.

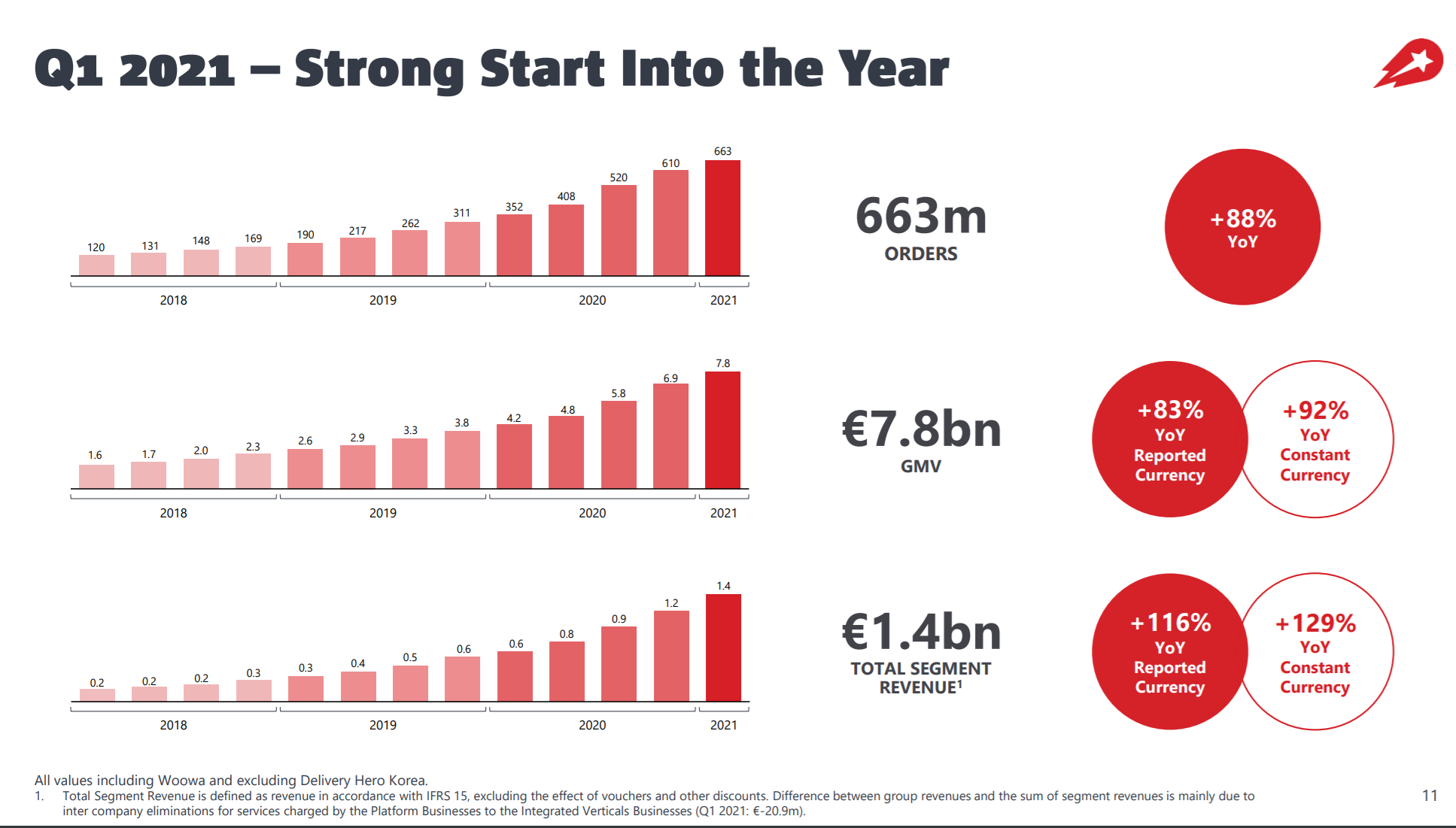

Delivery Hero orders increased +88% in Q1 2021, with GMV +83%. Strong growth pretty much everywhere. The Korean business Woowa is included on a pro forma basis from the 1st of January. Looking back at 2020 pro forma figures, Delivery Hero and Woowa combined processed 1.9bn orders, generated €21.8 billion GMV and €3.5 billion revenue. Share of own delivery increased from 38% in Q1 2020 to 48% last quarter. Delivery Hero is guiding for a 50% ca increase in GMV in 2021 to €31-34bn. The EBITDA/GMV guidance of -1.5% to -2.0% includes €550mn investments in new markets and verticals. Excluding these investments they could be profitable this year. In contrast to Just Eat Takeaway, they are investing in grocery deliveries.

Unilever reported a +5.7% growth in Q121. Not as impressive as Nestle last week but still above expectations. They announced a €3bn share buyback (2.4% ca). Growth was close to double-digit in Food and Emerging Markets, while Europe remains weak. 2021 guidance remained unchanged, at +3-5% sales growth and slightly better margin. Below how the different categories have performed through the pandemic: hygiene seems to be normalising after last year's surge, while out of home and personal care are slowly going back to normal.

Straumann is a dental implants company that has been hugely outperforming the S&P and Nasdaq over the past 20 years (see below). This week they reported a +34% growth in Q121 and raised their FY outlook to mid-to-high twenties. Over the past years the company has performed well and the stock rerated strongly on top, as multiples expanded. Congrats to the company and investors.

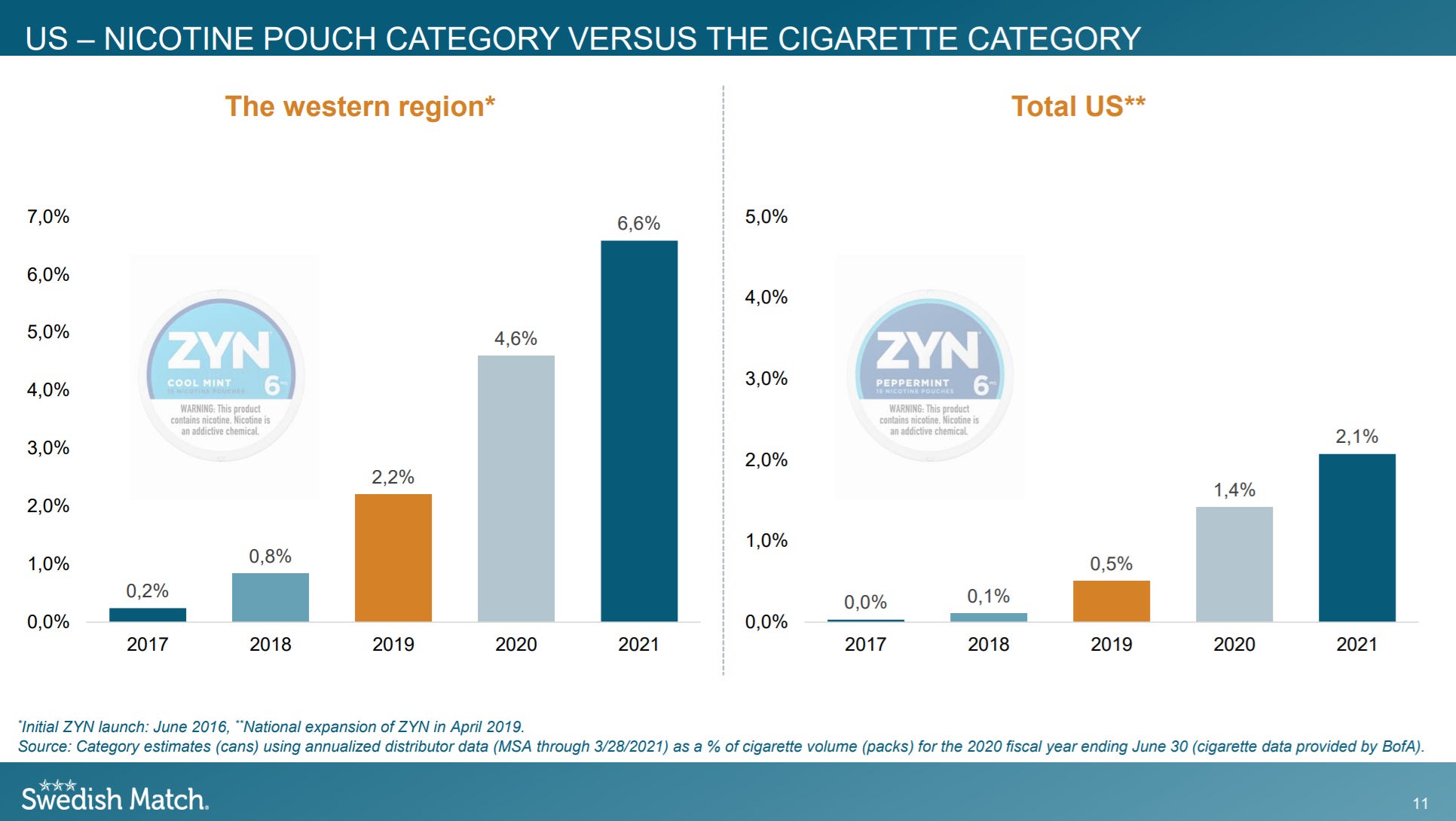

Last but definitely not least, Swedish Match reported excellent numbers. Sales increased +23% in the first quarter of the year. They sold almost 37mn ZYN nicotine pouches cans in the US, from 31mn ca last quarter and 25mn ca one year ago. Cigars did quite well too, with record shipments (some Covid boost). Nicotine pouches are growing fast but are still very small (2.1%) compared to the cigarette category in the US.

Nicotine pouches are also quite profitable. Swedish Match was the first mover in the US and should keep that advantage, but high growth + profitability = competition is increasing. Their distributor shipment market share declined to 65% ca compared to 74% one year ago. BAT’s Velo nicotine pouches reached a 17.6% share in US modern oral, from 8% ca last year. Altria is at 13% ca. According to the CEO, ZYN share is still above 70% in terms of value as competitors are running deep promotions. In any case, when you go from basically no competitors to a few, of course you lose some share. Growth is what matters. Actually, profitable growth: Swedish Match margin from product segments was 47.8% in the quarter, almost 52% in the core Smokefree segment. These are extraordinary high margins which should normalise as marketing expenses increase with reopenings, but still remain very healthy. Returns are quite high in the business.

Finally, a reminder that Swedish Match really likes its own shares:

M&A and IPO

Nestlé to acquire core brands of The Bountiful Company, expands health and nutrition portfolio (link)

Unilever to acquire Onnit (link)

DSV to acquire Agility GLI in an all-share transaction (in case you did not read above - link)

Darktrace shares soar 43% in London IPO (link)

Bernard Arnault and Jean Pierre Mustier Spac raises €500m in Amsterdam listing (link)

Other news

Solid first week (post reopening) for pub and restaurant groups in the UK (link)

FDA Plans to Ban Menthol Cigarettes (link) - note this is far from new and one of the reasons why the big tobacco companies have been underperforming / trade so cheap on multiples. As we discussed Swedish Match, remember that this is a niche player in the sector and they sold their cigarettes business in 1999. They still makes cigars, including flavoured ones, but 70% ca (and growing) of their operating profits is smokefree products. The CEO made some interesting comments in the Q1 call:

I think the honest answer there is that it's difficult to know with any degree of certainty when and if there will be any final proposals and not to mention also the regulatory process to enact such proposals. I mean, the FDA has as you're fully aware spoken about menthol ban since 2013 and since redeeming regulations in 2016, they are already then clearly stated that they intended to prohibit characterizing flavors in cigars and there have been advanced notices of proposed rule-making in various times thrown out there in terms of ambitions.

And at this point, there hasn't been any final rule. And as we indicated or as I commented, we think that this uncertainty that this creates with this type of system is not optimal from an industry point of view and particularly you start to see -- you have already in several states local flavor bans and so forth where actually the business continues to do well. But it would be certain advantages also with regulation that would be clearly defined and applicable to everybody. But we think it's more likely than not -- but difficult to know with certainty, but more likely than not that things will take quite some time and even uncertain whether it will really be implemented at all.

Have a great week and good investing!

If you are not a subscriber, please sign up to get full access and never miss an update.

Disclaimer: this newsletter is for informational purposes only and does not represent investment advice. I might have a position in some of the stocks discussed. Always do your own research before investing. Contact me on Twitter for any feedback or if you notice a mistake!