Investing in Europe #19

Investing in Europe #19

Prosus, Ubisoft, Food delivery in Germany and more

Welcome back to a new issue of Investing in Europe, a weekly newsletter on what’s happening in European companies and markets, filtered for what matters. Welcome to our new subscribers! 🥂 Your feedback is welcome, please DM me on Twitter 🙏

If you are not a subscriber, please sign up to get full access and never miss an update.

Company news and results

In a new effort to reduce its discount to NAV, Prosus announced a voluntary offer to acquire 45.4% of Naspers shares, followed by a new $5bn share buyback. It is not a straightforward transaction but will improve Prosus’s liquidity and float.

Ubisoft reported its full-year results. The French videogame company has been disappointing investors for a few quarters now, due to production delays and weaker than expected guidance. 2021/22 guidance sees net bookings up by single-digit and adjusted EBIT between €420-500mn. Consensus expected more. Ubisoft dropped its target to publish 3-4 AAA games per year and is shifting its strategy to focus on more free-to-play games. It does not mean that AAA games are going away, but free-to-play will be larger. It is about finding the best return on investment/monetisation strategy and could be the new normal for big franchises. Ubisoft is trading at lower multiples than peers but needs better execution to rerate.

Compass reported its H1 2021 results. While revenues remain depressed and did not improve much from Q1, the 4.2% Q2 operating margin was +150bps better than the previous quarter and slightly above the pre-close update issued last March. The foodservice company expects a gradual improvement in revenues in Q3 and a margin between 4.5% and 5%. They remain confident in rebuilding the above 7% margin before returning to pre-Covid volumes. Compass sees food inflation around 3.4% and labour inflation around 4%, higher in the US. The shareholder return program has not resumed yet, as the leverage remains above their target: the problem is not with the absolute debt level, but with the numerator as the business hasn't fully recovered yet.

Diageo issued a trading update and expects organic operating profit growth to be at least 14% in fiscal 2021 (June). The £4.5 share buyback program halted during the pandemic is restarting, with £3.25bn remaining until June 2024. £1bn will be completed this fiscal year, 1.3% ca of current market capitalisation.

Delivery Hero is returning to Germany two years after selling its local business to Takeaway.com (the non-compete agreement expired). Delivery Hero will soft launch in Berlin before expanding to other cities. The offer includes grocery.

On the same day, Just Eat Takeaway announced they will launch grocery delivery in Germany. They are also “investigating a similar approach in other key markets such as the UK and the Netherlands”. Germany represented 19% of Just Eat Takeaway orders, 16% of revenues (€374m) and 49% of EBITDA in 2020.

When the facts change, I change my mind - what do you do, sir?

The UK investment platform Hargreaves Lansdown issued a trading update for the four months to April 2021. Assets under administration increased 28% to £132.9bn, with £4.6bn net new money. Revenues were up 19%, boosted by record dealing volumes. They reported 6mn deals for the period, up 1.5x compared to last year. People have been trading more during the pandemic.

Where daily share dealing volumes settle, as we ease out of lockdown and life returns to more normal, is difficult to say. Similar to when previous lockdowns have been lifted, we have begun to see a reduction in share dealing volumes in both UK and overseas trades. However, given our focus on engaging with an ever-growing client base, helping to build their financial knowledge and confidence, ensuring the simplicity of investment via our platform and the breadth of equities available, we are confident that we will see a higher base level of dealing volumes than we did pre COVID-19. We will update our guidance on the shares revenue margin and other revenue margins when we announce our full year results on 9th August 2021.

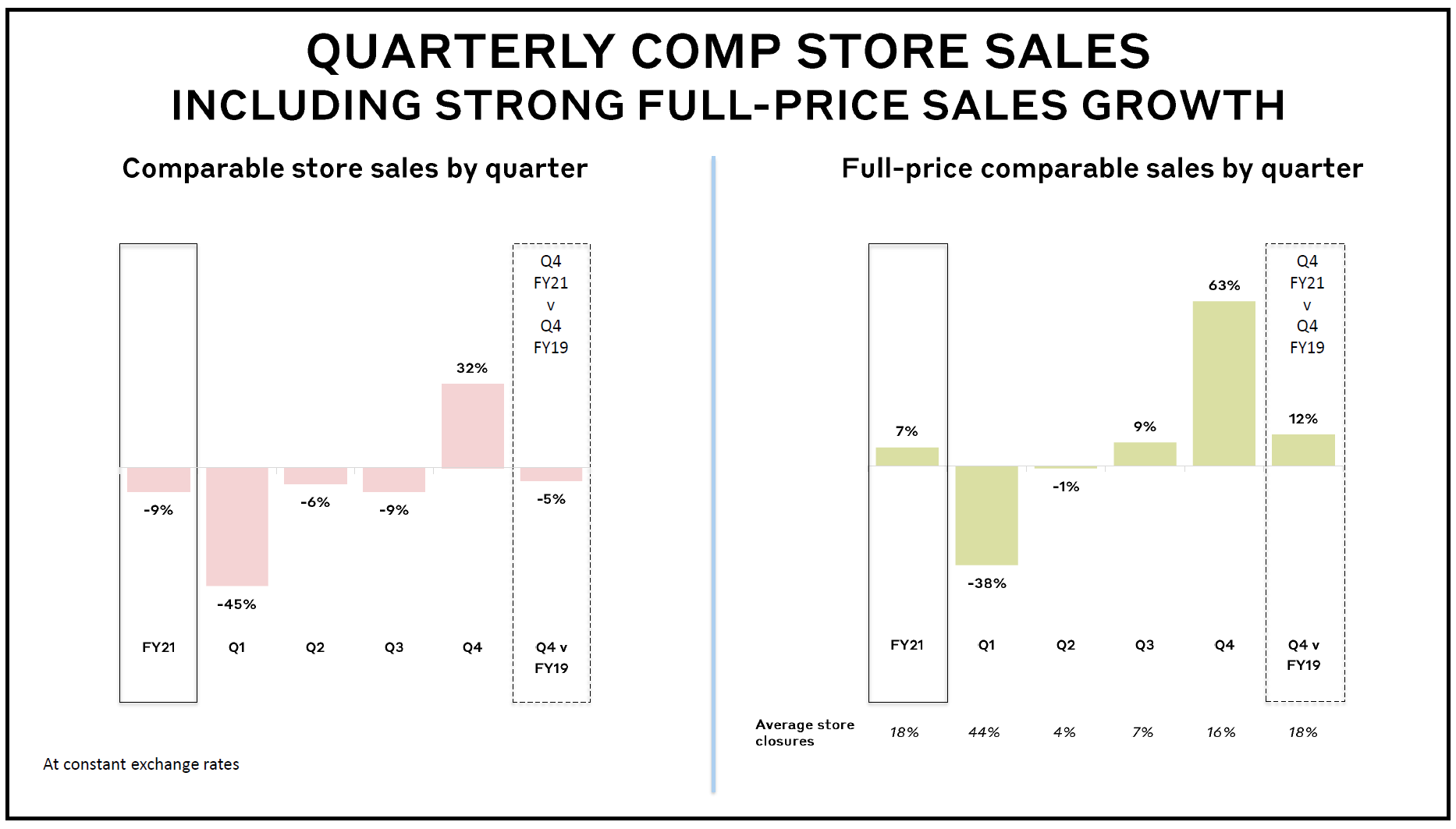

Burberry’s sales have not returned to pre-Covid levels yet. Q4 2021 (March) sales increased 32% compared to last year but are still down 5% to 2019 levels. In comparison, LVMH last quarter sales were up 8% vs 2019 and Hermes +33%. The British luxury company is focusing on accelerating growth and guiding for a high single-digit sales CAGR in the medium term. FY22 will be impacted by headwinds from a reduction in markdowns.

I ran a poll on Twitter

Try and think of your own answer before clicking on the tweet 🤔

M&A and IPO

Alphawave slumps 21% on debut as London IPO market stutters again (link)

Commodities broker Marex eyes London IPO of 500 mln pounds (link)

Danone intends to sell its stake in Mengniu (link) + is aiming to recruit new CEO soon (link)

Other news

SoftBank leads $1 bln investment in e-commerce company THG (link)

Moet’s Bubbly Chandon Spritz Aperitif Takes On Aperol (link)

Vivendi to list Universal Music Group by the end of September (link)

Have a great week and good investing!

If you are not a subscriber, please sign up to get full access and never miss an update.

Disclaimer: this newsletter is for informational purposes only and does not represent investment advice. I might have a position in some of the stocks discussed. Always do your own research before investing. Contact me on Twitter for any feedback or if you notice a mistake!