Investing in Europe #20

Investing in Europe #20

Richemont, Ryanair, Fever-Tree, Sonova and more

Welcome back to a new issue of Investing in Europe, a weekly newsletter on what’s happening in European companies and markets, filtered for what matters. Welcome to our new subscribers! 🥂 Your feedback is welcome, please DM me on Twitter 🙏

If you are not a subscriber, please sign up to get full access and never miss an update.

Company news and results

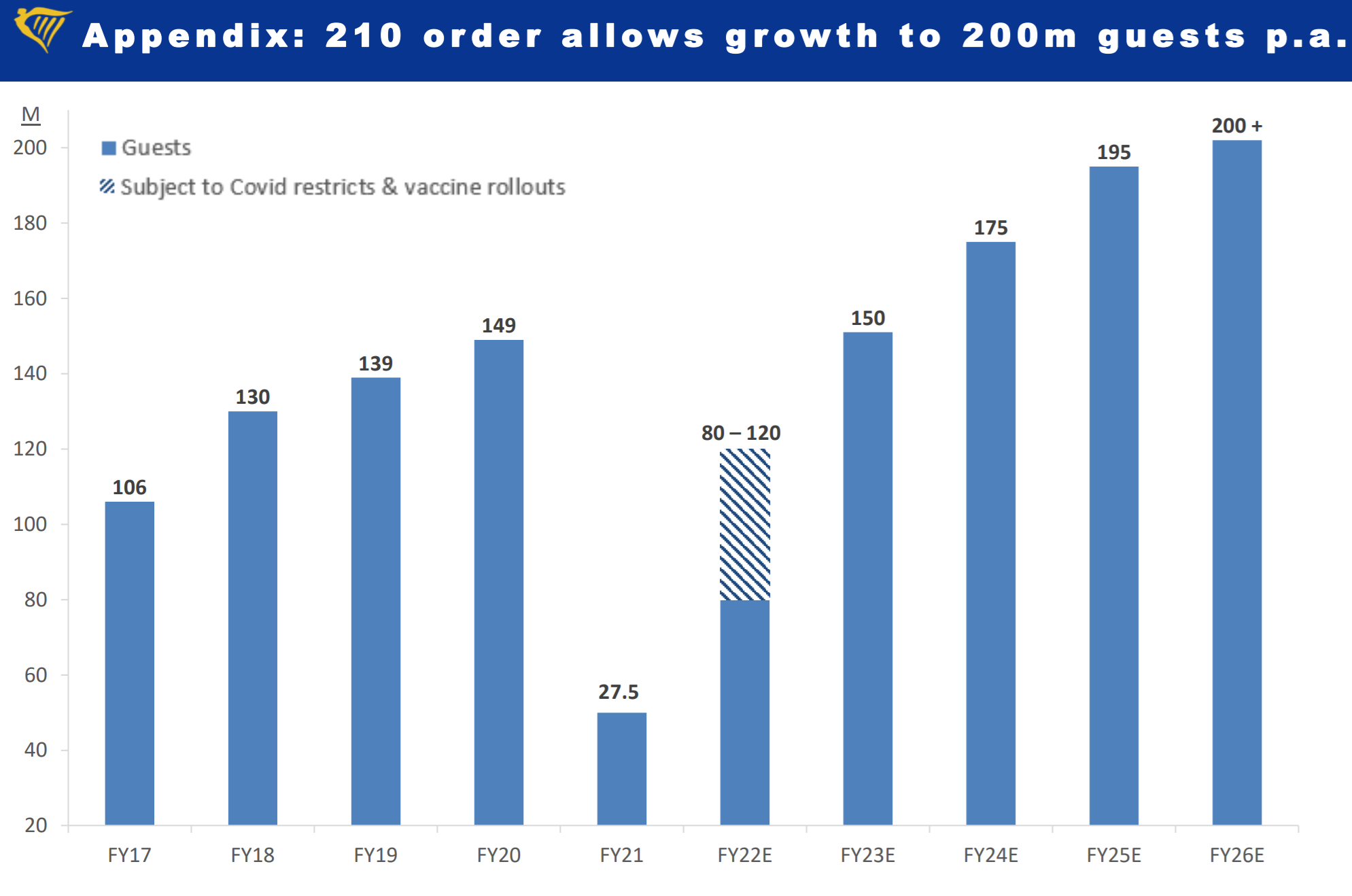

Ryanair reported its full-year 2021 results (March end). Traffic fell 81% in what they described as “the most challenging year in Ryanair’s 35-year history”. Ryanair needs at least another year for traffic to go back to 2019 level. For this year (March 2022) they expect traffic to be in the lower end of their 80mn to 120mn passengers guidance. This means they should be close to breakeven:

We also (cautiously) believe that the likely outcome for FY22 is currently close to breakeven – assuming that a successful rollout of vaccines this summer allows a timely easing of European Govt.

The long term 200mn passengers target is expected to be reached in 2026.

Ryanair will get the first new Boeing 737 MAX (or 737-8200 as they call it now) this month, two years after it was grounded due to two fatal crashes.

Vivendi gave a positive update on the UMG distribution:

the group is analyzing the opportunity of selling 10% of UMG shares to an American investor or initiating a public offering of at least 5% and up to 10% of UMG shares

They will also propose what seems a good set of governance principles. Neither Vivendi nor Group Bolloré intend to be represented on the Board.

HomeServe increased revenues by 15% in FY21, with North American Membership & HVAC up 22%. The company had already issued a preliminary statement last month. Including impairments (UK CRM system for £85mn), reported profit before tax was heavily down on the year. HomeServe expects “to deliver an acceleration in performance in FY22 “, with the on-demand Home Experts division expected to be profitable.

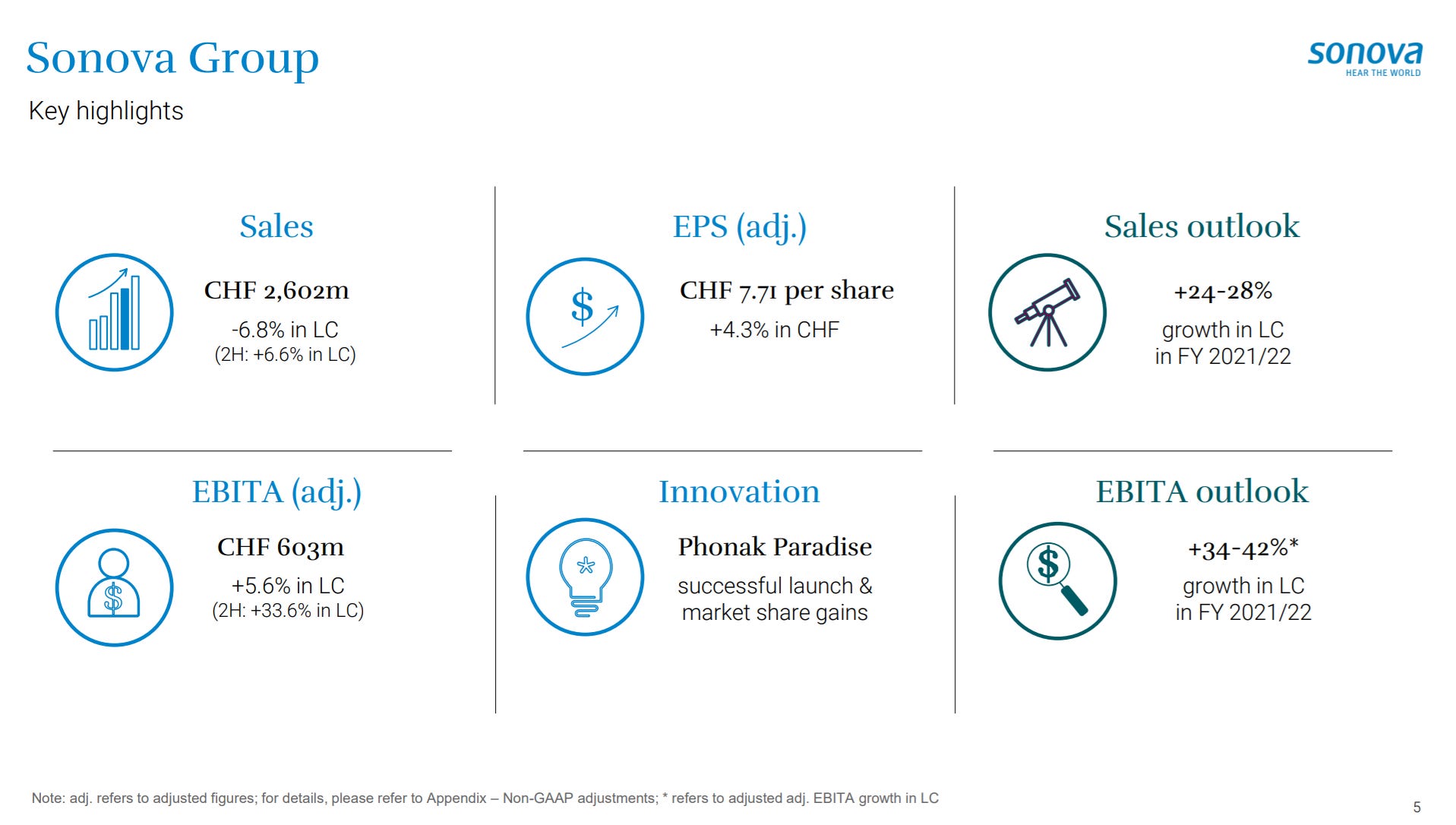

The hearing care company Sonova had a strong H2 of the fiscal year 2020/21 with sales up 6.6%. The hearing aid company is guiding for +24%-28% sales growth in 2021/22 and +34%-42% adj EBITDA growth.

UK pubs Marston and Mitchells & Butlers (over 3k pubs together) provided an encouraging post-lockdown update, although sales are still not back to normal (link)

The credit reporting company Experian reported a 4% organic growth in the full-year 2021 (March). For this year, they expect organic revenue growth in the range of 7-9%, total revenue growth of 11-13% and strong EBIT margin accretion.

Adyen launches its acquiring solution in Japan. The Japanese government has set a goal of increasing cashless payments to about 40% of all transactions by 2025, from about 20% currently.

Fever-Tree issued a trading update. The “world's leading supplier of premium carbonated mixers” is performing strongly on off-trade channels, while the on-trade is returning slowly. In the UK, off-trade was up +10.1% in the last 13 weeks to the 18th of April compared to last year. On-trade, which was 50% of UK sales pre-Covid, remains unpredictable. They estimate about 1/3 of premises reopened, at reduced capacity. In the US, off-trade was up +38.2% in the last 12 weeks to 27th March. Europe is lagging, while Australia is recovering, especially in suburban areas. Fever-Tree is “trading in line with the Board's expectations for the full year to 31 December 2021” 👇

Richemont last financial quarter was quite strong, with the Jewellery Maisons division up +28% compared to 2019. Jewellery Maisons was 42% of group sales but over 100% of group profits. For the full-year, sales declined -5% at constant currency as the Specialist Watchmakers division was heavily impacted by the pandemic. That’s fine. What is less fine is that the Online Distributors segment (which includes Net-a-Porter) was down too. In other news, Richemont’s chairman Johann Rupert admitted Kering Proposed a Tie-Up more than a year ago.

M&A and IPO

Kering discreetly tests investors’ appetite for its watch brands ($link)

Heineken in talks to buy majority of Distell (link)

ASOS may click with online beauty platforms Cult and Feelunique (link)

DSV Panalpina rumored to show interest in buying DB Schenker (link)

Oatly: Oprah-backed firm's shares soar in stock market debut (link)

Other news

Trainline shares plunge after government rail plans revealed (link)

Solutions 30 remains suspended as its auditor EY is not in a position to express an opinion on its 2020 financial statements…

Technogym’s founder sold almost 6% of the company to carry out the project that Technogym is considered "heritage of humanity" 🙏:

The transaction intends to carry out the project that Technogym is considered "heritage of humanity" as a promoter of Wellness as an opportunity for sustainability for the world. The founder's vision, since its origins, has always been to spread Wellness as a lifestyle, for people's health and well-being. The dream is to see Technogym continue to grow as a multinational Public Company that, regardless of its founder, develops a profitable and sustainable long-term growth in line with its social and economic mission, to the benefit of all stakeholders.

Eurostar lands bailout from investors and French state ($link)

DoorDash may be plotting European expansion (link)

Return to retail triggers spike in prestige make-up sales (link)

Have a great week and good investing!

If you are not a subscriber, please sign up to get full access and never miss an update.

Disclaimer: this newsletter is for informational purposes only and does not represent investment advice. I might have a position in some of the stocks discussed. Always do your own research before investing. Your feedback is important - please contact me on Twitter