Investing in Europe #21

Investing in Europe #21

Airbus, Intertek and more

Welcome back to a new issue of Investing in Europe, a weekly newsletter on what’s happening in European companies and markets, filtered for what matters. Welcome to our new subscribers! 🥂

Your feedback is very important, please comment below or DM me on Twitter 🙏

If you are not a subscriber, please sign up to get full access and never miss an update.

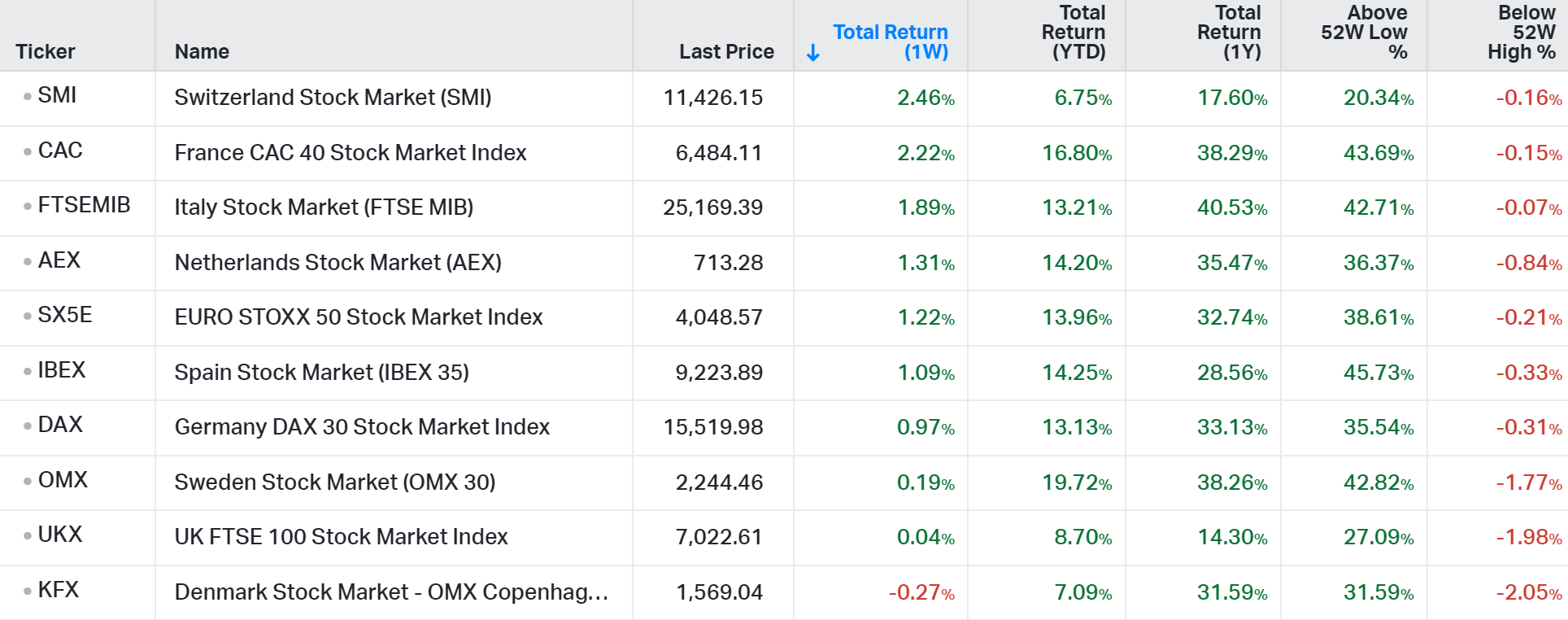

How was the week?

Company news and results

The quality assurance company Intertek reported a trading update for the first four months of 2021. Revenue growth was 2.7% in the period, down 4.1% in Jan-Feb and up +9.3% in Mar-Apr. Mr Market expected more. The Products business (82% of group profit) was up 7.4%: most of the business lines were up double-digits except building and construction and transportation technology, which were down. Intertek is on track to deliver its FY21 targets of “good” revenue growth and margin improvement.

Airbus, the world's largest airliner manufacturer, provided a positive update on its production rates for 2023 to 2025, when they expect the commercial aircraft market to recover to pre-Covid levels:

A320 Family: Airbus confirms an average A320 Family production rate of 45 aircraft per month in Q4 2021 and calls on suppliers to prepare for the future by securing a firm rate of 64 by Q2 2023. In anticipation of a continued recovering market, Airbus is also asking suppliers to enable a scenario of rate 70 by Q1 2024. Longer term, Airbus is investigating opportunities for rates as high as 75 by 2025.

A220 Family: Currently at around rate five aircraft per month from Mirabel and Mobile, the rate is confirmed to rise to around six in early 2022. Airbus is also envisaging a monthly production rate of 14 by the middle of the decade.

A350 Family: Currently at an average production rate of five per month, this is expected to increase to six by autumn 2022.

A330 Family: Production remains at an average monthly production rate of two per month.

A lot of planes. The A320 numbers are above the pre-Covid rate of 60 per month and (again, pre-Covid) target of 63 per month they had for 2021. These are narrow-body planes so we are talking about short-haul / regional traffic, which Airbus expects to recover faster than most expected. Where is the acceleration coming from? It could be higher industry demand or higher market share (vs Boeing). We’ll see.

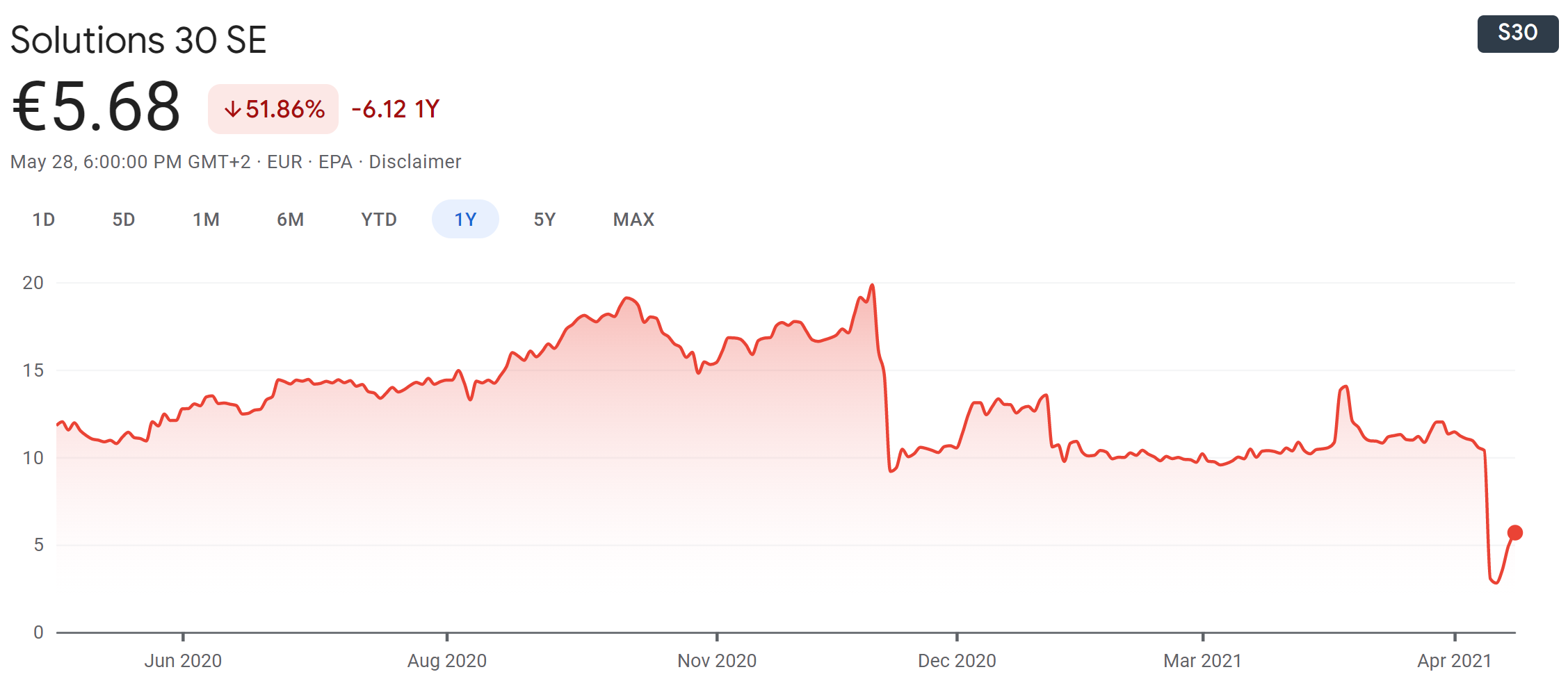

After being suspended since the 7th of May, Solutions 30 reopened - and crashed:

This is more a detective story than anything else, and quite a complicated one. The FT has covered it quite well here: Solutions 30: from Romania to Mauritius, with love (link)

Muddy Waters published an interesting note too - big respect for him and all the short-sellers trying to expose frauds:

M&A and IPO

Volkswagen Group receives (and rejects) €7.5bn offer for Lamborghini (link)

Glovo buys Delivery Hero Central and Eastern Europe brands (link)

Vonovia and Deutsche Wohnen to combine in €18bn real estate deal (link)

Klarna seeking new funds at close to $50 bln valuation (link)

Fashion Retailer About You Seeks $732 Million in German IPO (link)

Other news

SPAC activity in Europe:

So far this year, 293 blank-check vehicles have gone public in the US, raising a total of €15.8 billion (around $19.2 billion), according to PitchBook data. Europe has lagged behind the US in 2021 with only 17 listings worth €2.2 billion, but SPAC activity is increasing on the continent

Kering sells part of its Puma stake (link)

Just Eat Takeaway.com and Sodexo sign a global partnership (link)

Unilever teams up with plant-based protein start-up Enough to expand vegan food range (link)

Have a great week and good investing!

If you are not a subscriber, please sign up to get full access and never miss an update.

Disclaimer: this newsletter is for informational purposes only and does not represent investment advice. I might have a position in some of the stocks discussed. Always do your own research before investing. Your feedback is important - please contact me on Twitter