Investing in Europe #22

Investing in Europe #22

Reading press releases, drinking cognac, travelling. And more

Welcome back to a new issue of Investing in Europe, a weekly newsletter on what’s happening in European companies and markets, filtered for what matters. Welcome to our new subscribers! 🥂

Your feedback is very important, please comment below or DM me on Twitter 🙏

If you are not a subscriber, please sign up to get full access and never miss an update.

Weekly performance update

Company news and results

Hello friends. It was a great week for fundamental meme stock investors. I am afraid I have no story about massive short squeezes in Europe, where I guess the Volkswagen 2008 squeeze will never be beaten. What I have is a summary that I hope will help you better navigate through companies’ reportings and updates. As usual, your feedback is very important, please comment below or DM me on Twitter 🙏

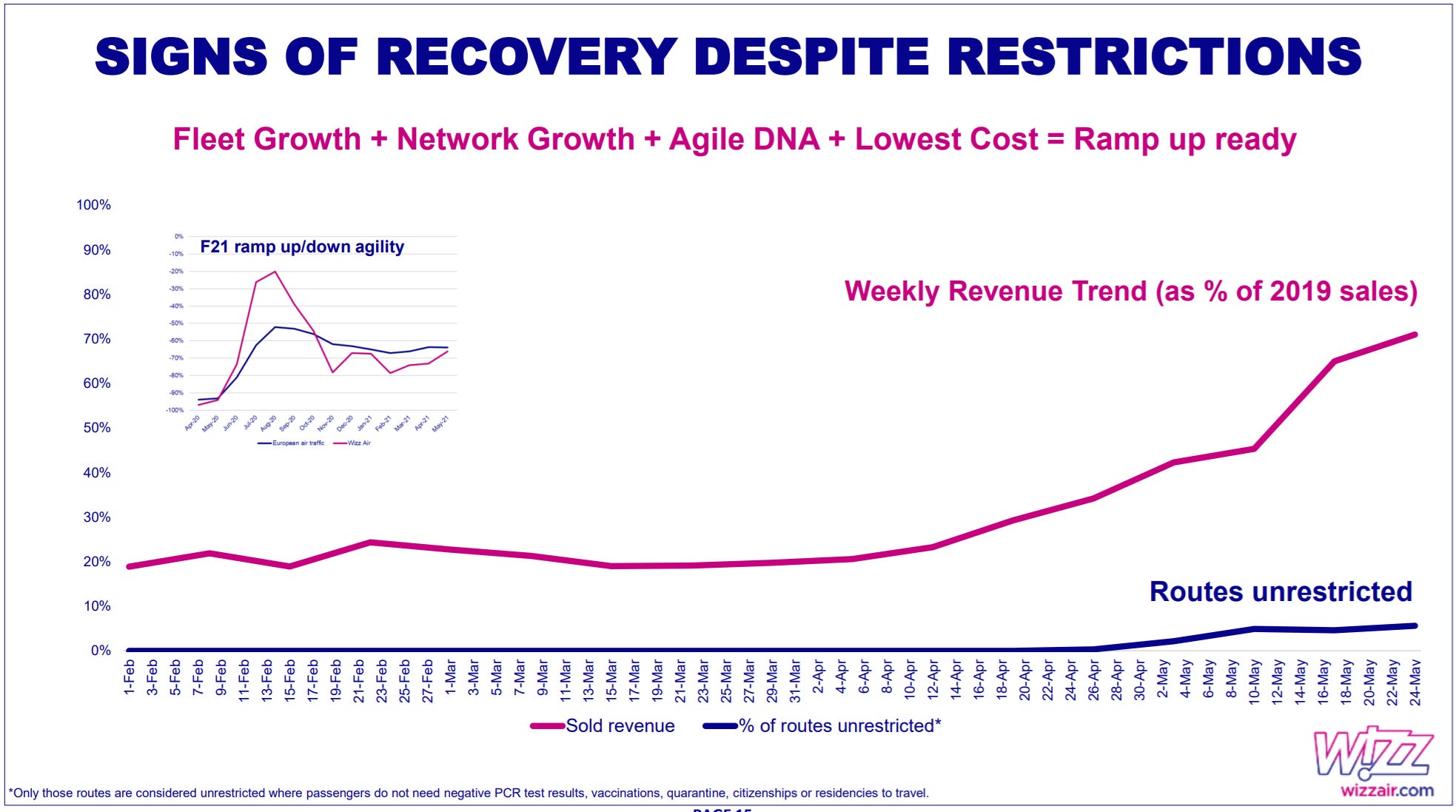

Wizz Air lost €482mn in its last financial year, close to the midpoint of last April’s guidance range. Including ineffective fuel hedges, they lost €576mn. Pre-Covid, Wizz Air hedged a minimum of 50% of the projected USD and jet fuel requirements for the next twelve months. With a 75% drop in passengers and little revenues, most of those hedges were simply a cost.

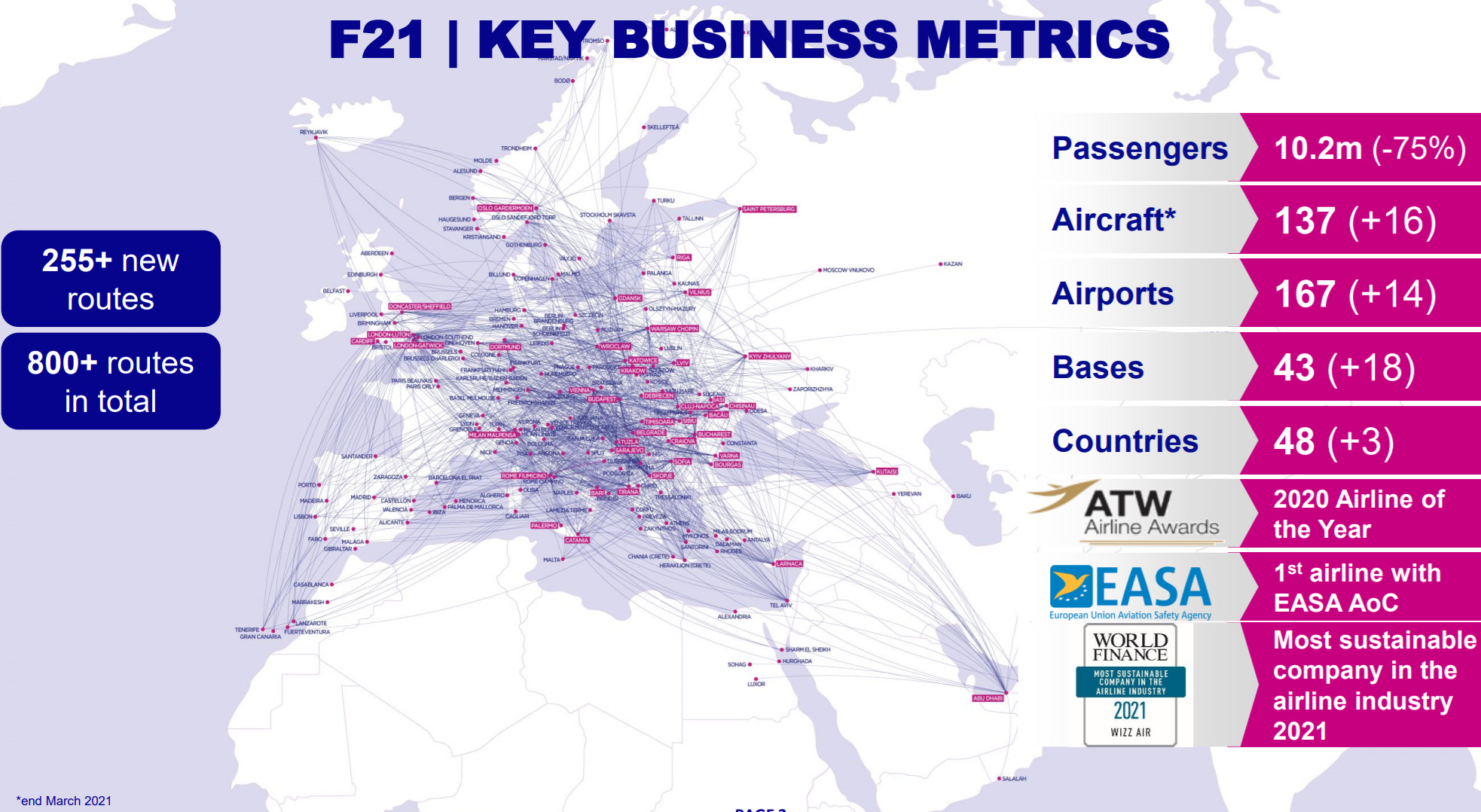

Wizz Air is a very decent company in one of the worst sectors to invest in. Last year ROCE was 21% 🛫. Courtesy of Covid, it went down to -19.4% 🛬.

They flew only 10mn passengers last year, with a 64% load factor, a low level for a low-cost airline. In contrast with other airlines cutting capacity, Wizz Air expanded their fleet by +13% to 137 aircraft. Their market share in CEE increased from 17.5% to 20.9% (45.9% in the low-cost segment).

I found it interesting that ancillary revenue (ie what you pay on top of the basic ticket) kept increasing, to 54% of total sales:

Wizz Air expects FY 2022 (Mar 22) to be a transition year where net profit will be negative. They have plenty of liquidity and burnt only €28mn per month in the last quarter. FY 2023 should be a year of full capacity.

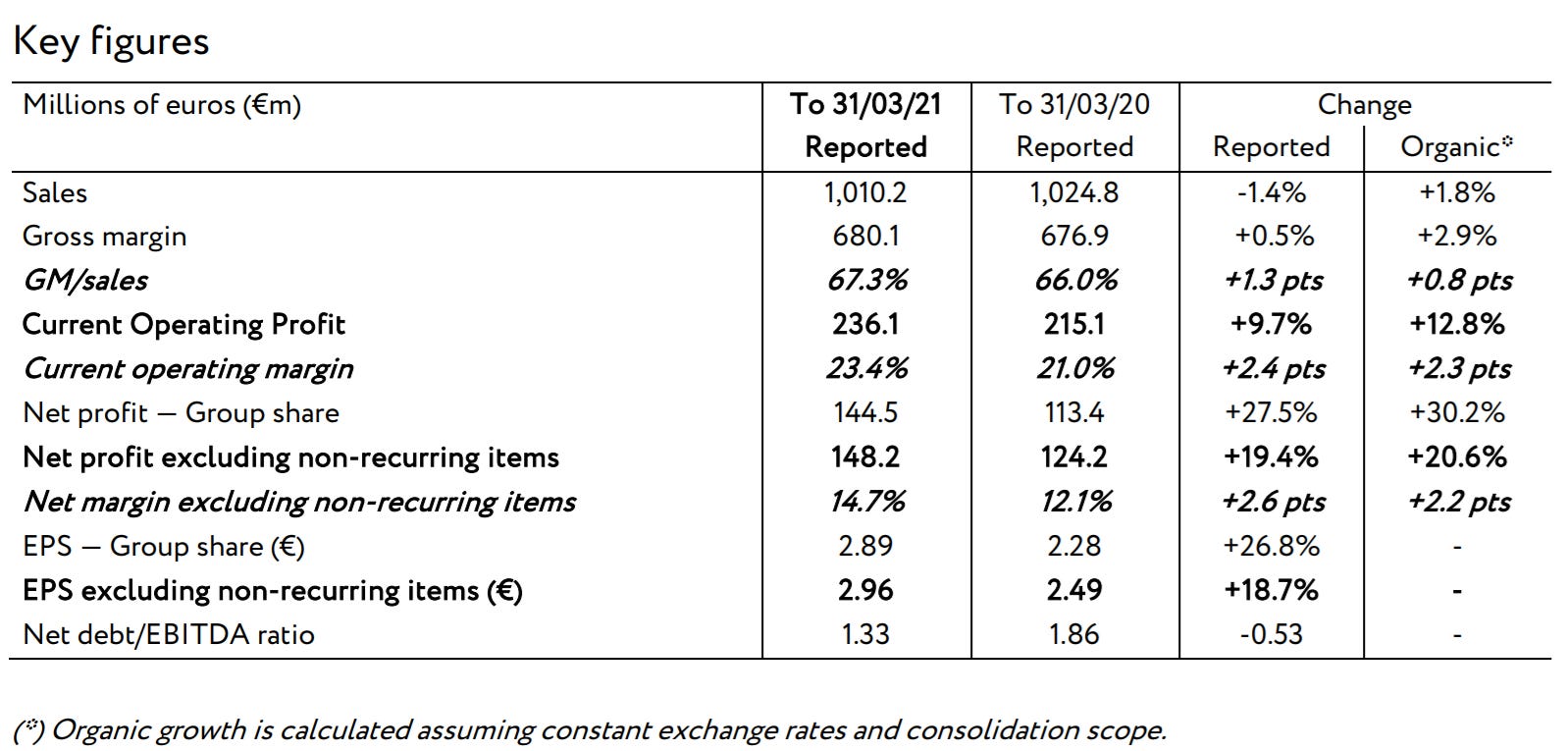

Remy Cointreau business is long term in nature: it takes 10+ years to age a XO Cognac, even 100 years for the highest quality Hors d'Age like Louis XIII. That’s why they are talking about 2030 targets with “increased confidence”.

Mar 21 sales were reported in April, up +1.8% YoY. This week, Remy Cointreau reported its operating margin increased +2.3 pts to 23.4% and gave a qualitative guidance on Mar 22:

For financial year 2021/22, the Group is confident in its ability to continue to win market share in the exceptional spirits sector. In particular, the Group is anticipating an excellent start to its financial year, underpinned by very favourable base effects, shipment phasing effects, and new, structurally more buoyant consumption trends in the United States.

By segment, cognac sales were up +3.7% FY with the second half of the year up +27%, thanks to the US and China. Cognac is 73% of group sales and approx 85% of EBIT. Liqueurs & Spirits division was down 3.2%. Group ROCE improved +60bps to 17.1%.

They also announced a 1mn shares buyback, small (< 2% of shares) but better than nothing. FX is not helping but that doesn’t matter much long term.

The UK variety retailer B&M reported a +25.9% increase in revenues in its financial year 2021 (Mar). Margin improved 407bps to 13%. Covid helped, which means they will face tough comparisons this financial year: UK LfL sales are down 1% in the first 9 weeks.

Trading continues to be volatile at a weekly and product category level, in particular since the recent easing of lockdown restrictions. This is likely to remain the case for the whole of FY22, as the business annualises against the very strong comparatives throughout last year. As such, the B&M UK business expects to see a decline in LFL revenues in FY22 compared to FY21, but is focused on delivering a healthy two year LFL versus FY20.

The long term target remains unchanged, as B&M expects to rollout at least 950 stores in the UK, from 681 as of March.

The “American investor” in last month Vivendi’s press release was…Bill Ackman. Vivendi has been updating us on UMG quite frequently. The “opportunity of selling 10%” to an investor before the distribution/listing was mentioned less than a month ago. Nonetheless, it was a great deal on Twitter, with a lot of misunderstanding. I realised not everyone commenting reads press releases or clicks on links 😅

If you are interested in more details on the deal, Matt Levine here and Steven Wood 👇 wrote some interesting comments I agree with:

Informa, the publishing, business intelligence and exhibitions company, issued a trading update:

Following Informa’s 2020 Full Year Results published on 22 April 2021, the Group has continued to trade in line with expectations and remains on track to deliver the baseline revenue target for the year of at least £1.7bn, as well as remaining cashflow positive,underpinned by improving underlying revenue growth in our two subscriptions-led businesses.

CD Projekt is one of the worst performers in Europe this year, down 40% YTD. Cyberpunk’s maker profits fell more than half in Q1 2021 compared to last year. Cyberpunk 2077 was delayed 3 times and then released with still some bugs. The game is still not available on Playstation, after being removed.

M&A and IPO

French indie distribution and services company, Believe, has launched its IPO on the Paris Euronext (link)

AI-Health App Babylon Plans $4.2 Billion SPAC—And Push Into U.S. (link)

Other news

Tmall, Givaudan Partner for Accelerated Scent Creation in China (link)

Nestlé document says majority of its food portfolio is unhealthy ($link)

The 10 most valuable beer brands ranked (link):

Have a great week and good investing!

If you are not a subscriber, please sign up to get full access and never miss an update.

Disclaimer: this newsletter is for informational purposes only and does not represent investment advice. I might have a position in some of the stocks discussed. Always do your own research before investing. Your feedback is important - please contact me on Twitter