Investing in Europe #24

Investing in Europe #24

Boohoo, Just Eat in London and more

Welcome to a new issue of Investing in Europe, a weekly newsletter on what’s happening in European companies and markets, filtered for what matters. Your feedback is very important, please comment below or DM me on Twitter 🙏

If you are not a subscriber, please sign up to get full access and never miss an update.

Company news and results

Busy week at work and I am late, sorry. A quick recap:

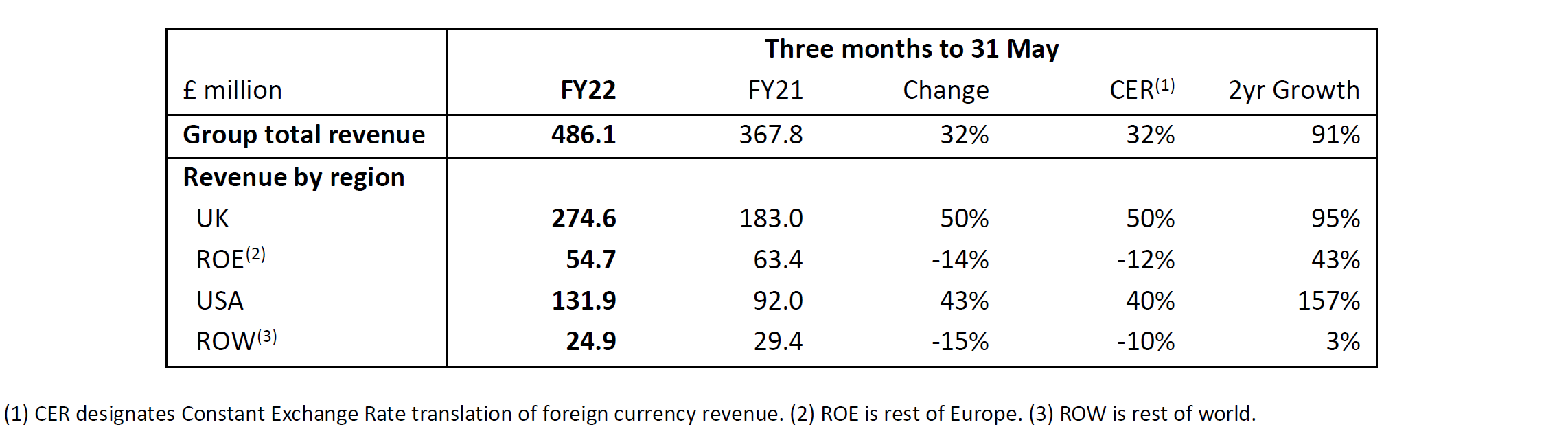

The UK online clothes retailer Boohoo issued a trading update for the first quarter of 2021 (May end). Revenue increased 32% compared to last year, or +91% compared to 2 years ago. UK and US, the biggest regions, performed the best: UK (56% of sales) was up 95% over 2019 and the US (27% of sales) up 157%. Rest of Europe was up +43%, Rest of the World was the weakest region, only up 3% in 2 years. Gross margin remained flat over the same 2 years period, at 55%.

A few things regarding the “issues” Boohoo had with working conditions in its supply chain last year: 1) customers did not care much, it seems; 2) there is a new report from Sir Brian Leveson; 3) Boohoo joined the Fast Forward audit program:

The forensic audit process helps to uncover audit evasion and hidden exploitation including indicators of forced labour and assesses adherence to employment laws and across ethical labour standards requirements.

Everything solved? We will see. Before the 18th June AGM, ISS and Glass Lewis had recommended investors to vote against the re-election of the co-founder and executive director Carol Kane.

According to the FT:

ISS said a vote against Kane was warranted because she “is considered ultimately accountable for the failures in governance, stewardship and risk oversight, which have caused significant reputational harm to the company in connection with the poor working conditions and pay in the company’s supply chain in Leicester.”

She survived. Only 12% of votes were in favour of removing her as executive director.

Going back to numbers, full-year 2022 guidance remained unchanged: Boohoo is expecting revenues to grow around 25% (including 5% from M&A) and EBITDA% (adj) at 9.5-10%.

Just Eat Takeaway updated its company presentation:

The slide below shows they are gaining market share in London from the green guys (should be Uber). As announced with the H2 results last year, Just Eat is implementing an aggressive investment program in the UK and other key European markets where they have been losing market share.

The program includes:

more logistic - 64% of total orders in the UK in Q121 were delivered by Just Eat’s own couriers, compared to less than 10% last year

better offer - more/better restaurants

more marketing

It seems to be working so far:

Lufthansa Group announced medium-term targets and made preparations for a capital increase (link)

A 10% ROCE is considered an “ambitious” mid-term target in the airline industry:

Based on the transformation of its operating model, the restructuring of the Group’s cost base to the New Normal and the goal of capitalizing on future opportunities to further strengthen the balance sheet, Lufthansa Group targets to reach an Adjusted EBIT margin of at least 8% by 2024. Combined with a disciplined investment policy and strict working capital management, this will support a return on capital employed (Adjusted ROCE excluding cash) of at least 10% by 2024.

Exor is investing more in luxury, as the holding company is joining forces with Hong Kong's WWICL to invest in Italian high-end consumer goods.

Daniel Loeb’s Third Point built a stake in Vivendi, while Bluebell Capital Partners and Artisan Partners are already lobbying to get better terms in the UMG spinoff (heavy tax bill to pay).

M&A and IPO

Morrisons says it rejected £8.7bn bid from Clayton, Dubilier & Rice (link)

Wise announces plans to go public via direct listing (link)

Spain's Acciona seeks $11.6 bln valuation with renewables IPO (link)

Made.com shares fall 7% after completing London IPO (link)

Other news

May’s delivery and takeaway sales at Britain’s leading restaurant and pub groups were 273% higher than in May 2019 (link)

Have a great week and good investing!

If you are not a subscriber, please sign up to get full access and never miss an update.

Disclaimer: this newsletter is for informational purposes only and does not represent investment advice. I might have a position in some of the stocks discussed. Always do your own research before investing. Your feedback is important - please contact me on Twitter