Investing in Europe #26

Investing in Europe #26

First half of 2021. Some positive trading updates. A study on luxury. European companies' revenues and more

Welcome to a new issue of Investing in Europe, a weekly newsletter on what’s happening in European companies and markets, filtered for what matters. Your feedback is very important, please comment below or DM me on Twitter 🙏

If you are not a subscriber, please sign up to get full access and never miss an update.

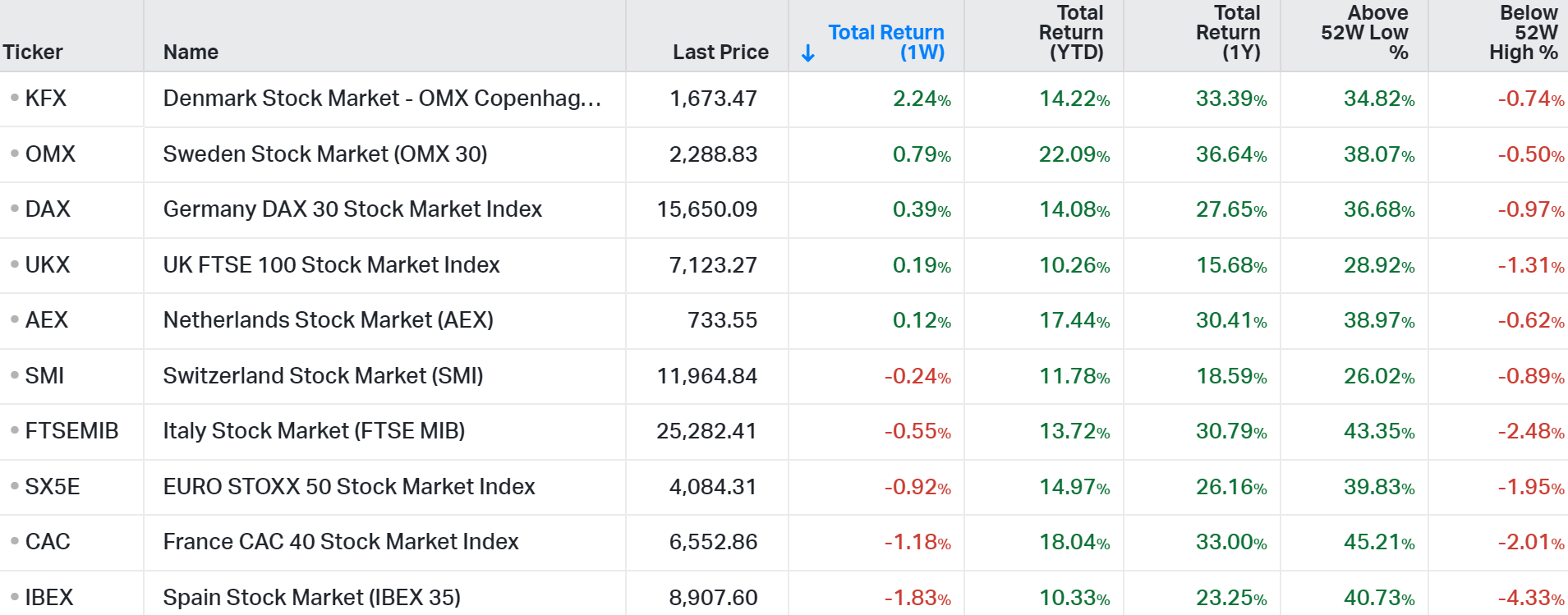

Weekly performance update

Dear investors and friends, the first half of the year is over. I hope you are doing well, and I am not just talking about performances. Thank you for reading this newsletter and please continue sending feedbacks here.

Europe (Stoxx 600) is up almost +16% year to date. Most of the sectors I tend not to invest in did great 😅. Banks were the strongest performers YTD in Europe, up +26%. As I mostly focus on quality companies, I don’t follow Banks because I don’t see much value creation, unfortunately. I feel no FOMO when the sector rallies. Utilities were the weakest performers and the only negative sectors YTD. Good news I don’t follow Utilities either.

Twitter is full of people posting amazing performance numbers. A bit of survivorship bias and short-termism of course. Still, non-professionals can beat professionals in this game, when they have a long term horizon, better focus, no short-term competitive pressure and fewer restrictions. Thanks to Twitter and this newsletter, I had the opportunity to chat with a few of them and I must say they know what they are doing. These are not people making money on meme stocks and leverage bets in a bull market, but serious investors who do their own research and think long-term. I am happy for them and I hope this newsletter is of some help. I am not talking about everyone on Twitter, of course. For those trading meme stocks, if you know you are gambling and not investing that’s fine, but please beware.

Company news and results

Moving to the usual news and results commentary, a few updates this week 👇

After almost five years at Burberry, the CEO Marco Gobbetti will step down to join Salvatore Ferragamo. Ferragamo probably needs to revamp its strategy more than Burberry did when Gobbetti joined, as the stock has not moved much in the last 8 years. Not that the job at Burberry is over, unfortunately. Burberry’s sales have been less resilient than peers during the pandemic, and the strategy still needs some fine tuning. Historically they had good ROIC 👇, what they need now is better growth.

Adidas announced a new share-buyback program of €550mn - 0.9% of the market cap - until the end of the year. They sound bullish about next years growth and cash flow generation:

Through its new strategy ‘Own the Game’ adidas expects to drive significant top-line growth and strong bottom-line expansion until 2025. As a result, the company will generate substantial cumulative free cash flow over the next five years. Adidas plans to share the majority of this –between € 8 billion and € 9 billion – with its shareholders through regular dividend pay-outs in a range of between 30% and 50% of net income from continuing operations, complemented with share buybacks.

A few companies that have been impacted by the pandemic upgraded their guidance, mainly on a better than expected recovery:

Sodexo, the French food services and facility management company, reported its Q3 results (May). Revenues are recovering gradually but are still below 2019 levels. In the second half of their fiscal year, they expect a return to full opening in Schools and a much better start to the new academic year in Universities. As for the Business & Administrations division, they still expect a 27% drop in office population post-Covid. Some people will continue to work from home, at least partially. Sodexo raised its H2 guidance to 15% organic growth and 3.5% underlying operating margin.

This is a labour-intensive, tough sector where Compass remains the best in class operator and should maintains industry-leading margin.

Primark’s owner ABF issued a trading update. Primark revenues reached £1.6bn in the third quarter. with the reopening of all stores and the opening of seven new stores. Revenues are back to 2019 levels, as like-for-like sales in the quarter were 3% up on a two-year basis.

Our forecast for full year sales at Primark has increased accordingly and adjusted operating profit, stated before repayment of job retention scheme monies, is now expected to be broadly in line with last year. Our outlook for the adjusted operating profit for the group, stated before repayment of job retention monies is now in line with last year.

On the other hand, H&M’s current trading update was weaker than expected, with June sales 4% below 2019 levels. A slowdown from last month update.

The UK sports-fashion retailer JD sports increased their profit before tax and exceptional items guidance for the full year, to no less than £550 million. The previous guidance was £475-500mn.

London Stock Exchange had an investor education event with a focus on some of their Data & Analytics segments: Enteprise Data, Trading and Banking, Customer and Third Party Risk. They estimate their total addressable market at £40-45bn, growing at +4-6% per year, compared to £5bn Data & Analytics pro-forma revenues in 2020.

The UK food-on-the-go retailer Greggs issued a trading update:

This level of sustained sales recovery is stronger than we had anticipated and, if it were to continue, would have a materially positive impact on the expected financial result for the year. We will provide an updated picture when we present our interim results on 3 August 2021

M&A and IPO

Ray-Ban owner (EssilorLuxottica) will go ahead with pre-pandemic $8.7 billion GrandVision buy despite fight with seller (link) - all that fuss for nothing

Acciona prices IPO of renewables unit at bottom end of range (link)

Instant grocery startup Getir makes its first acquisition to expand into Spain and Italy (link)

Richemont acquires Delvaux, the oldest luxury leather goods Maison in the world (link) - quite small and no material financial impact

Bridgepoint Seeks $2.8 Billion Value in Rare Buyout Firm IPO (link)

Other news

“LVMH live broadcast of the 2022 menswear collection on June 24 has reached more than 130mn views. The popularity has set a record for the highest number of live broadcasts in the luxury fashion industry." (link - in Chinese)

Ocado Retail ramps up CitrusAd retail media roll-out (link)

United Airlines unveils huge jet order in push for growth (link) - including 70 Airbus A321neo jets

BCG - Altagamma 2021 study on luxury (link) - a few points in the thread below:

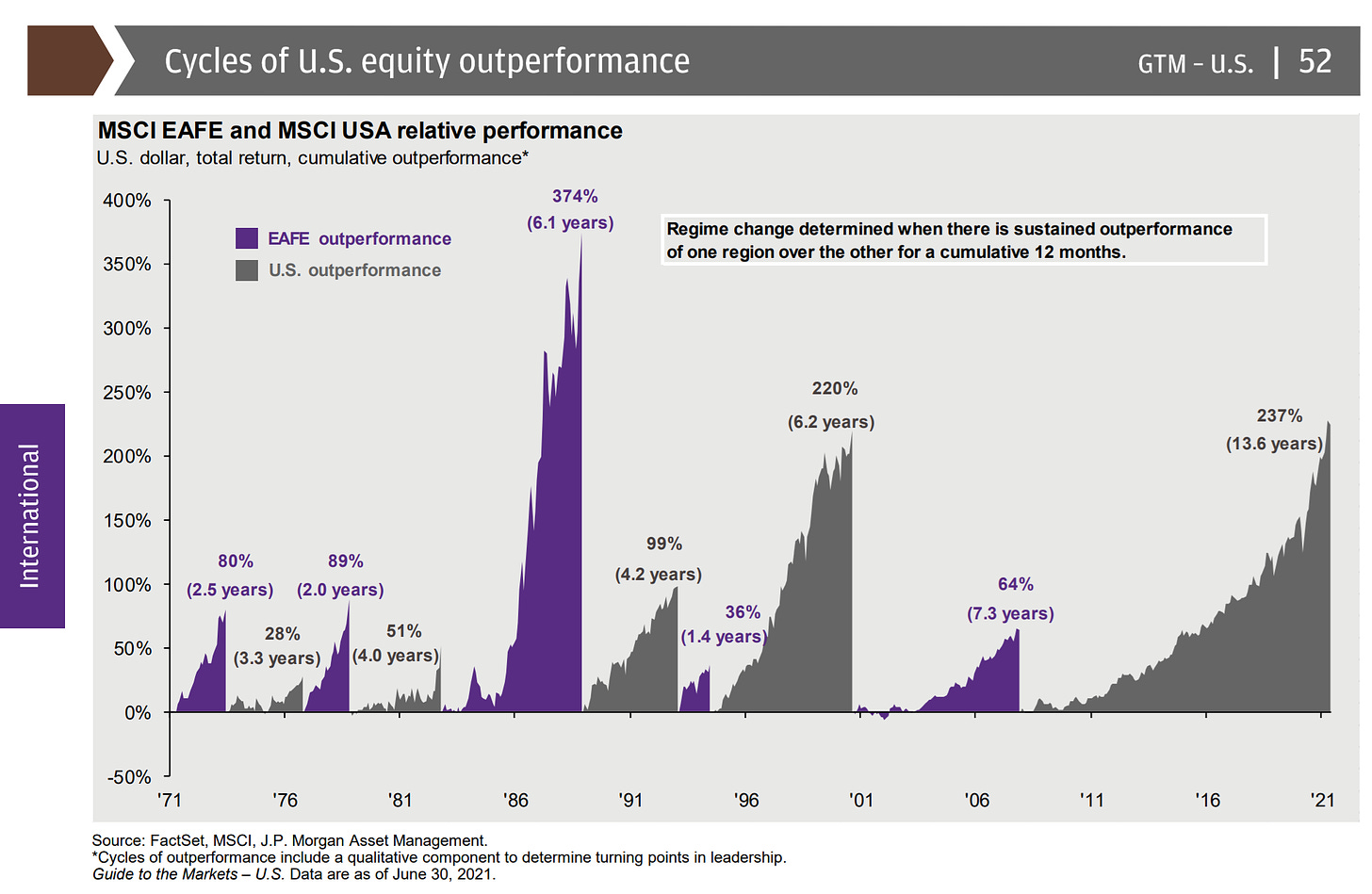

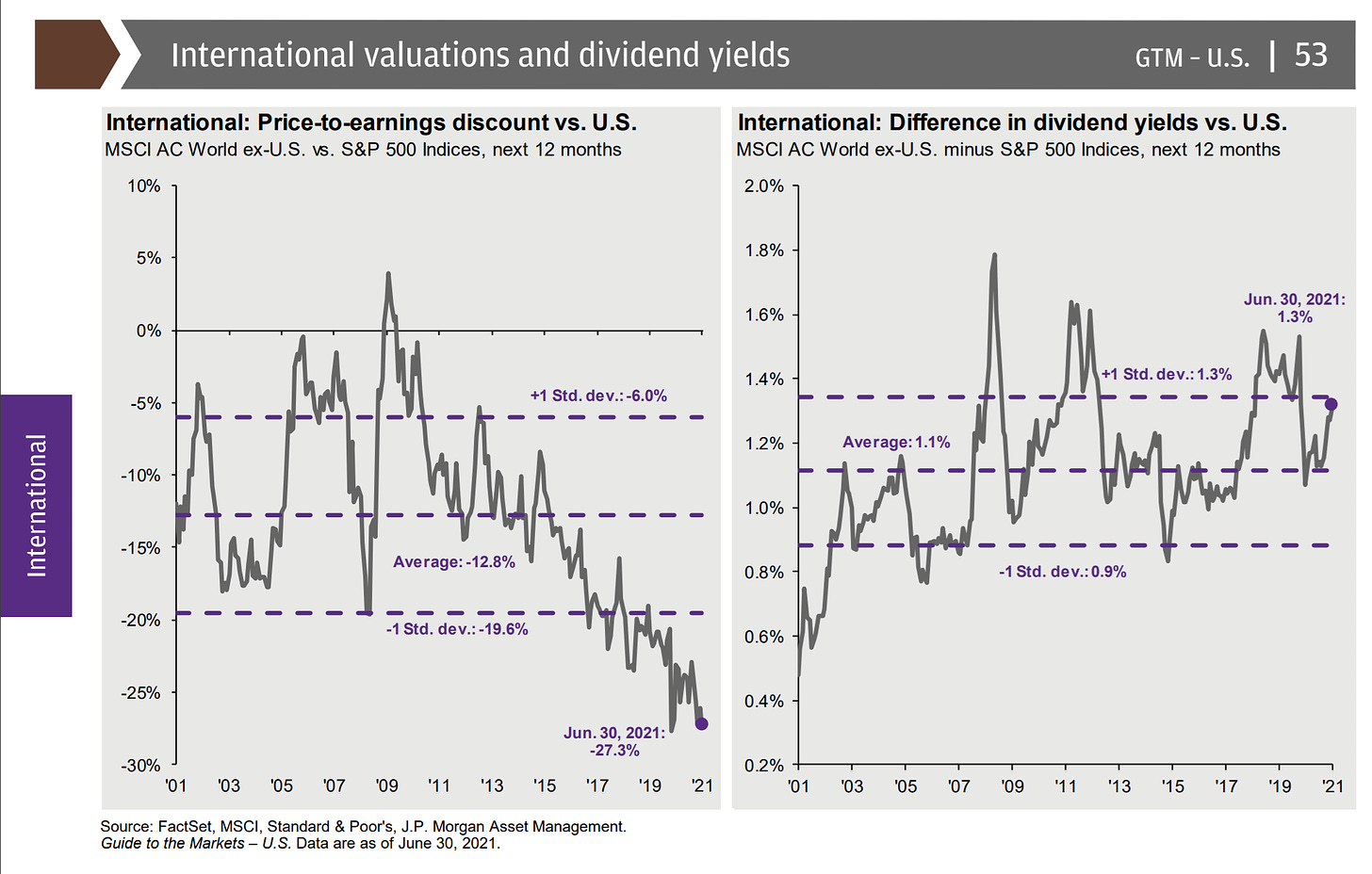

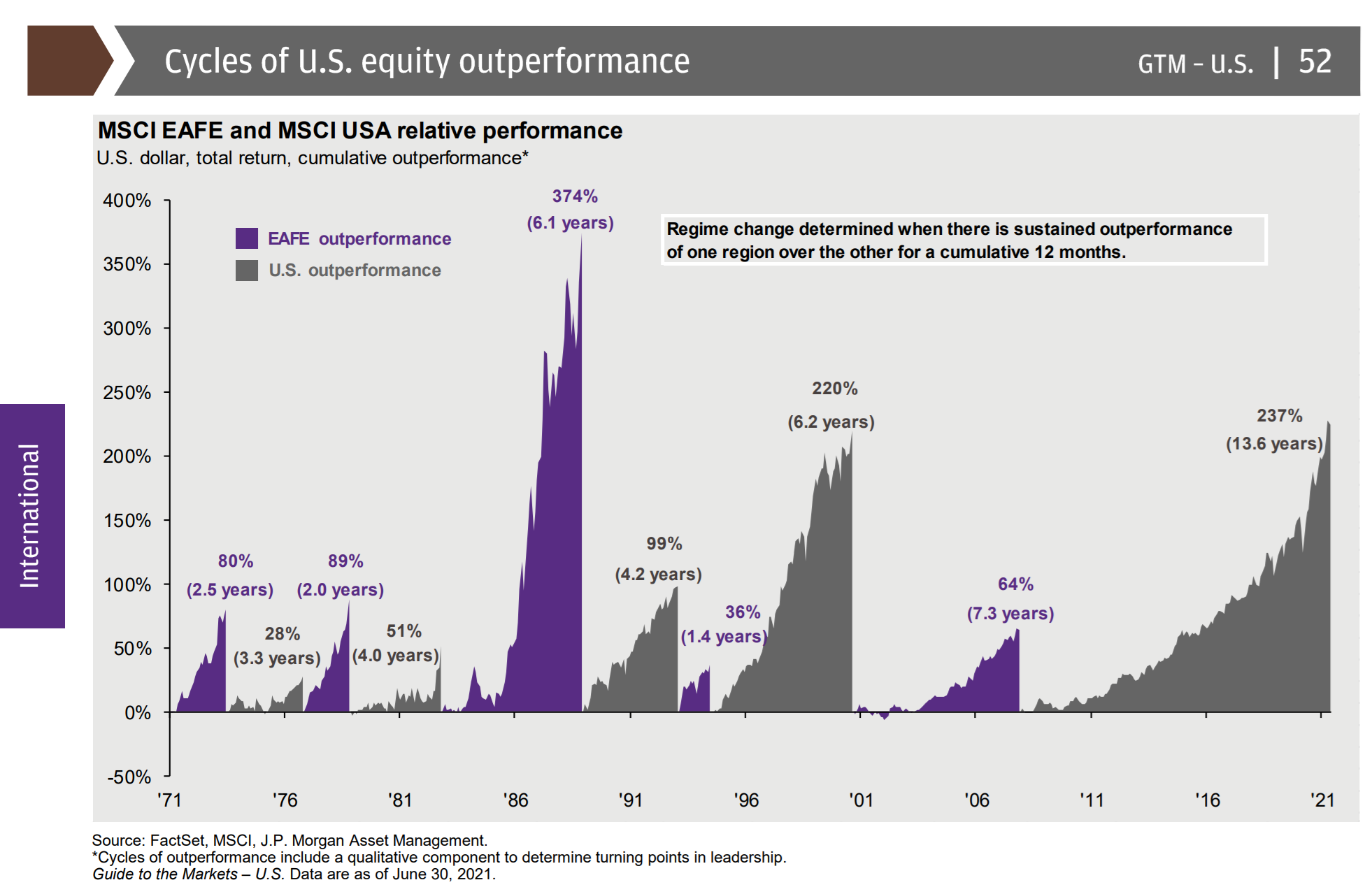

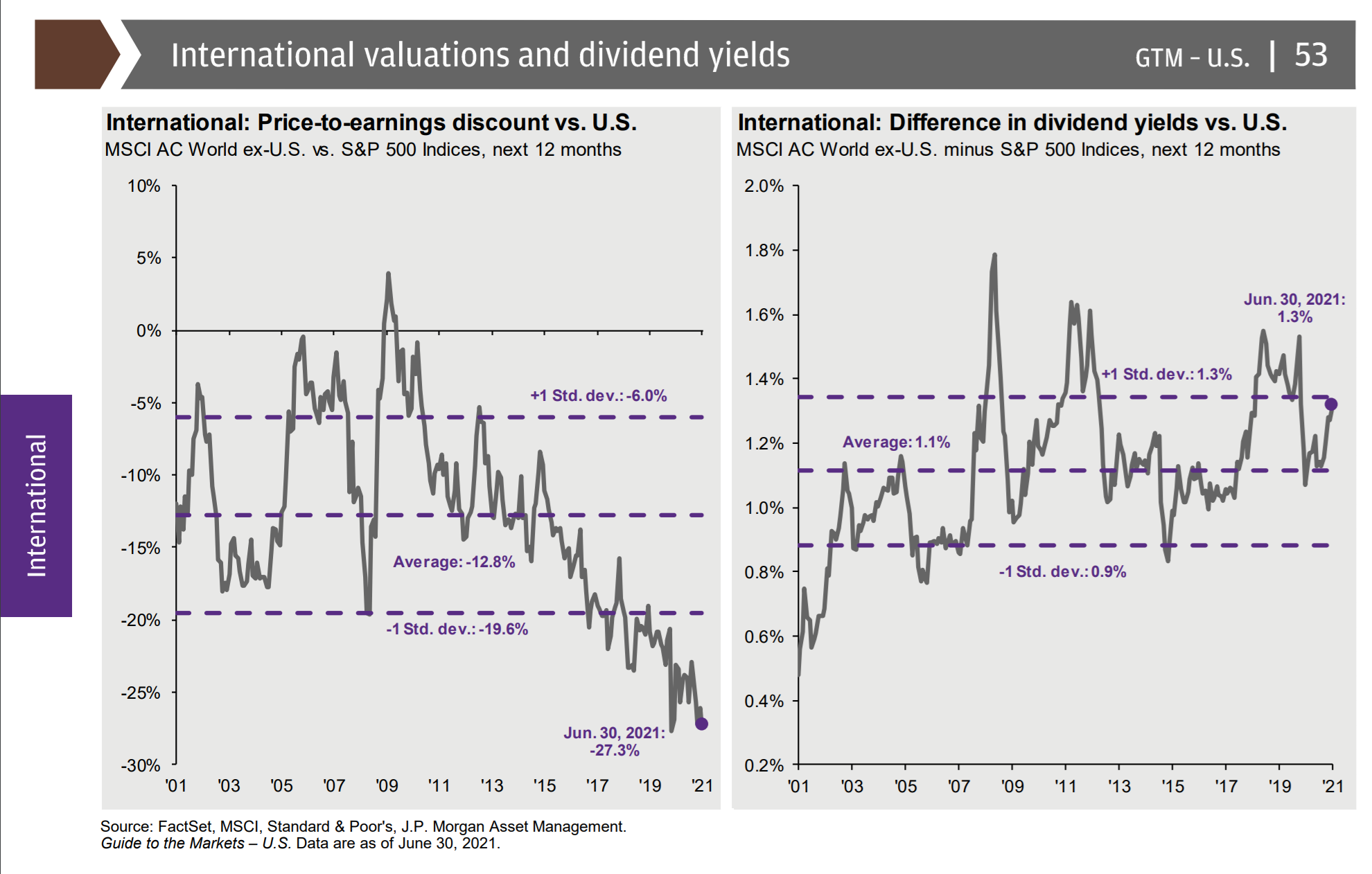

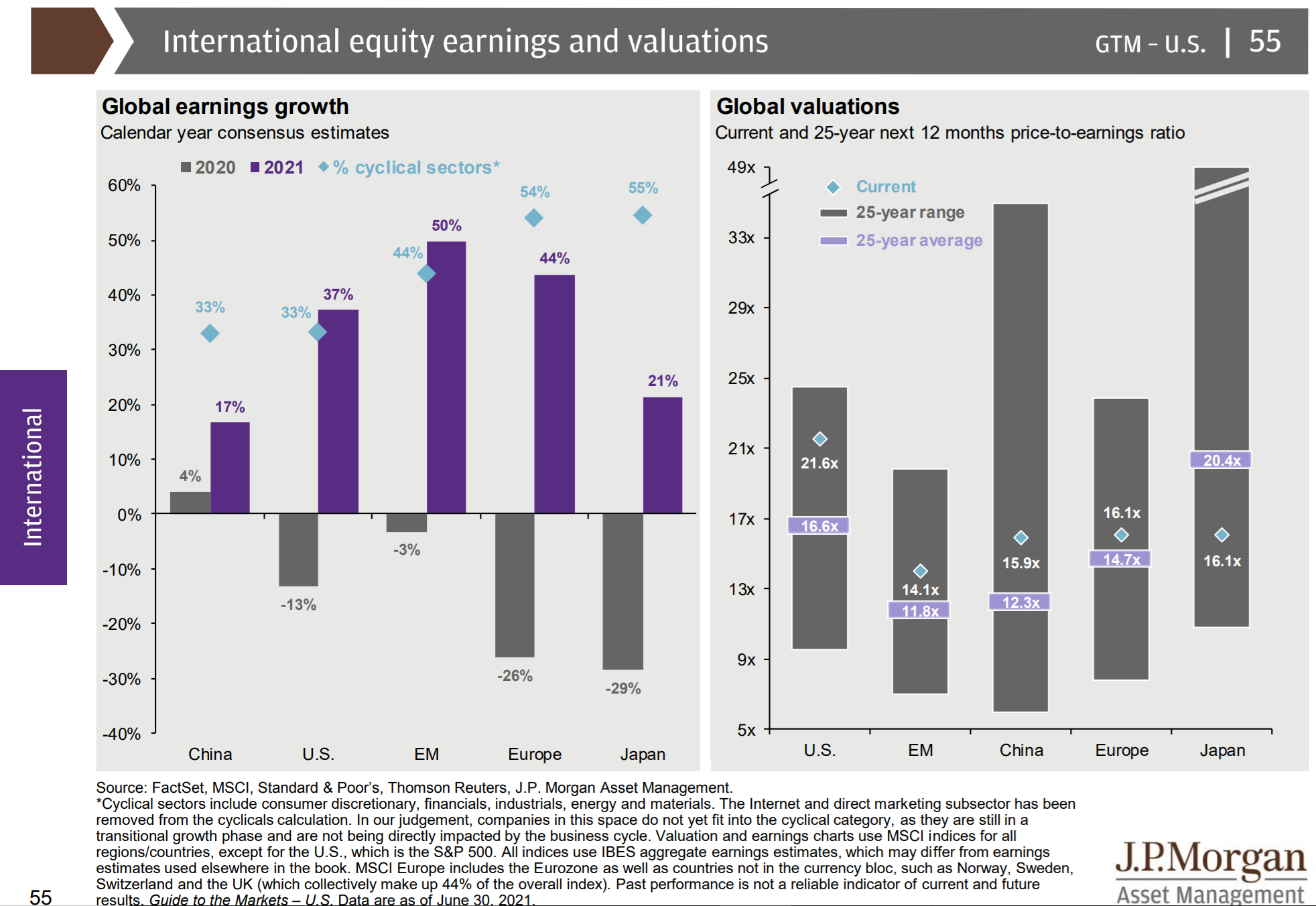

A few slides from the JPM Q3 Guide to the Markets. We are in the longest cycle of US outperformance by far, almost 14 years compared to the 6.2 years of the previous cycle. International markets trade at historically low multiples compared to the US. Europe is expected to be the second fastest-growing region in 2021, although it is mainly thanks to easy comparisons. 2020 was awful.

we are in the longest cycle of US equity outperformance by far

International “valuations” look cheap - but multiples are not valuations

Europe is expected to be the second fastest-growing region in 2021, although it is mainly thanks to easy comp vs 2020

A quick thread on European companies’ revenues and where they come from 👇

Have a great week and good investing!

If you are not a subscriber, please sign up to get full access and never miss an update.

Disclaimer: this newsletter is for informational purposes only and does not represent investment advice. I might have a position in some of the stocks discussed. Always do your own research before investing. Your feedback is important - please contact me on Twitter