Investing in Europe #30

Investing in Europe #30

Luxury earnings. Staples and inflation. Long term compounders. And more.

Welcome to a new issue of Investing in Europe, a weekly curated newsletter on what’s happening in European companies and markets.

Your feedback is very important. Please comment below or DM me on Twitter. If you are not a subscriber, please sign up to get full access and never miss an update. 🙏

Company news and results

Dear readers, it has been a very intense week of earnings. More than 50% of companies have reported so far in Europe and earnings were in aggregate better than expected. The pandemic hit the most in Q2 2020 and now we are seeing a strong recovery. Inflation seems a common topic, and probably a good test of companies’ pricing power.

In the luxury space, LVMH, Kering and Hermes reported strong numbers.

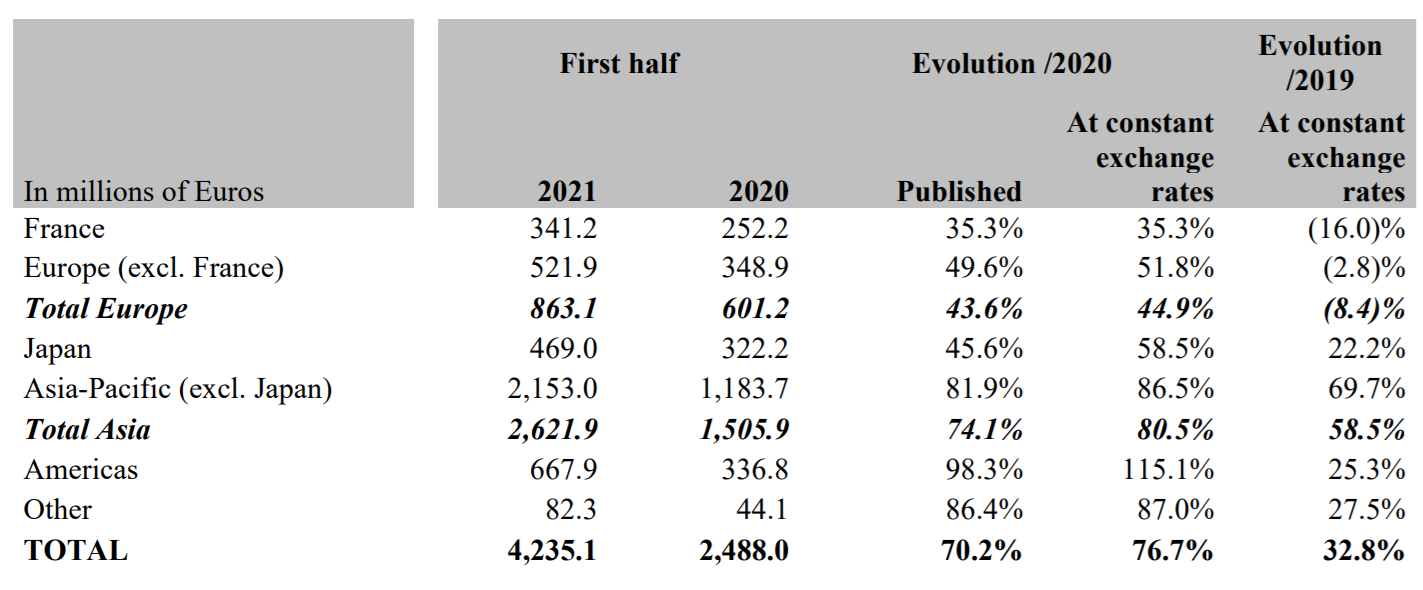

LVMH H1 sales were up +53% vs last year and +11% vs 2019. The key business group Fashion & Leather was once again the star, with a very strong +38% increase vs 2019. Compared to the depressed levels of 2020, growth is so strong that they measured it in multiples rather than percentages. Even more impressive than sales growth, profits were up +44% vs 2019 and operating free cash flow was 3x. Growth accelerated in Q2, driven by the US. Europe remains depressed due to lack of tourism, but demand from local customers seems to be very strong. We discussed in the past editions how LVMH navigated the pandemic so well: repatriation of Chinese demand, strong underlying demand, brands, efficiencies.

Bernard Arnault, Chairman and CEO of LVMH, said:

The creativity, the high-quality and enduring nature of our products and the sense of responsibility that drives us, have been critical in enabling us to successfully withstand the effects of the pandemic

Kering showed similar trends. H1 2021 sales were up +54% YoY and +8% on a 2 year stack. Note the +8% is not comparable to the +11% of LVMH, due to a different mix. Kering was less resilient than LVMH during the pandemic. Still, Gucci returned to 2019 levels with a strong acceleration in Q2 and the company seems to be optimistic about the second part of 2021.

Hermes reported almost a +33% increase in sales compared to 2019. Operating margin reached almost 41%. All regions except France were above 2019 levels in Q2. By sector, ready-to-wear, accessories, jewellery and home products posted the strongest growth rates. Overall, impressive.

Input cost inflation is a common theme for Consumer Staples this quarter. Generally speaking, the more commoditised the product, the higher the pressure.

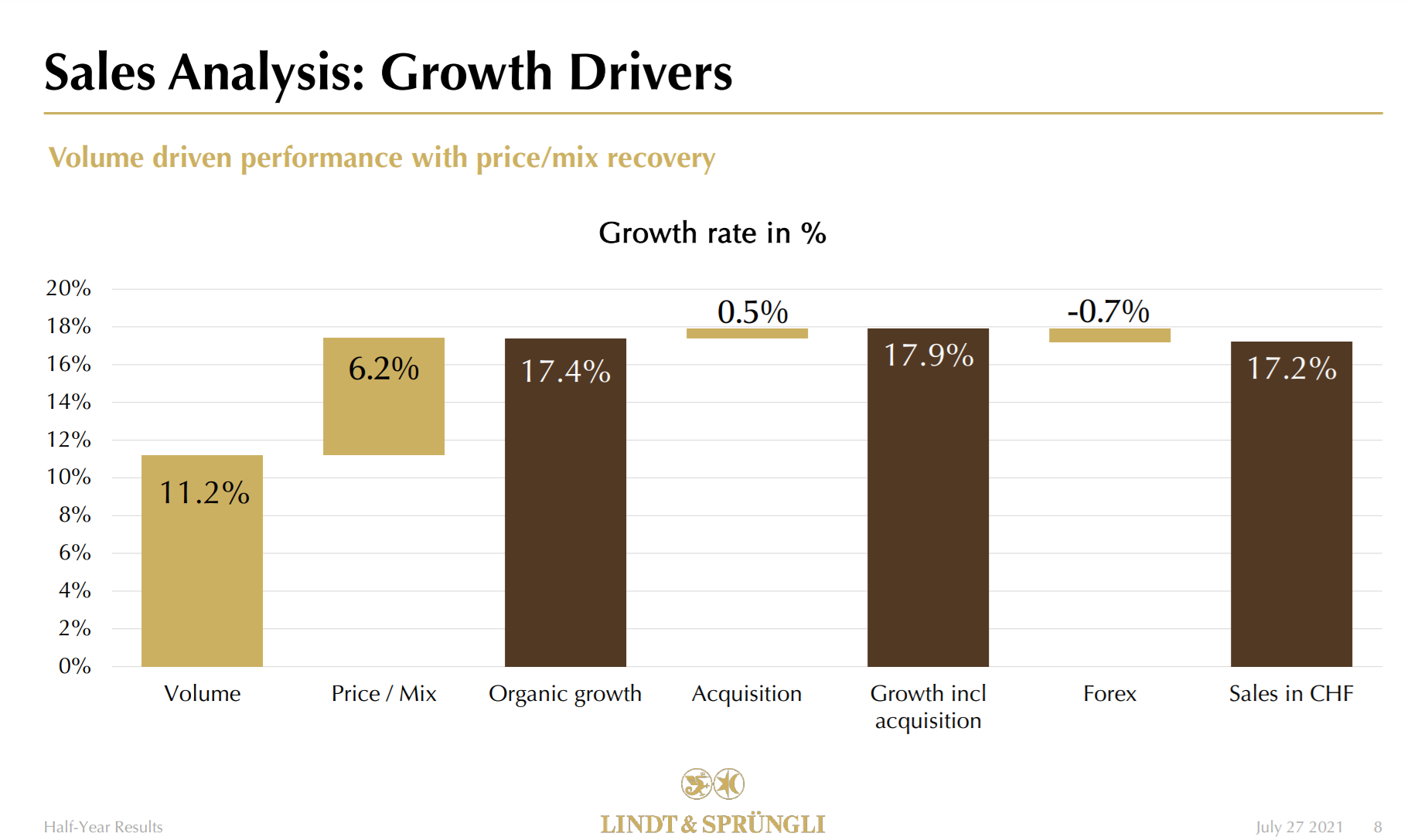

Let’s look at the Swiss chocolatier Lindt: H1 results showed no inflation pressure and a +6.2% price mix. Guidance improved: for the full year, they expect organic sales growth in low double-digits vs 6-8% previously; EBIT% at the upper end of previous 13%-14% guidance.

On the other hand, Reckitt was one of the weakest stocks this week as they highlighted an acceleration in cost inflation. They are also facing tough comps as last year there was an extraordinarily high demand for their hygiene and disinfectant products.

“Cost inflation accelerated in the second quarter and it will take time to offset this headwind with productivity and pricing actions being implemented in the back half of the year and early next year. This will largely offset the margin accretion in 2021 from the disposal of IFCN China. As a result, our guidance, which now excludes IFCN China, is for the adjusted operating margin to be between 22.7% to 23.2% which is 40 to 90bps lower than the 23.6% reported for the full year 2020.

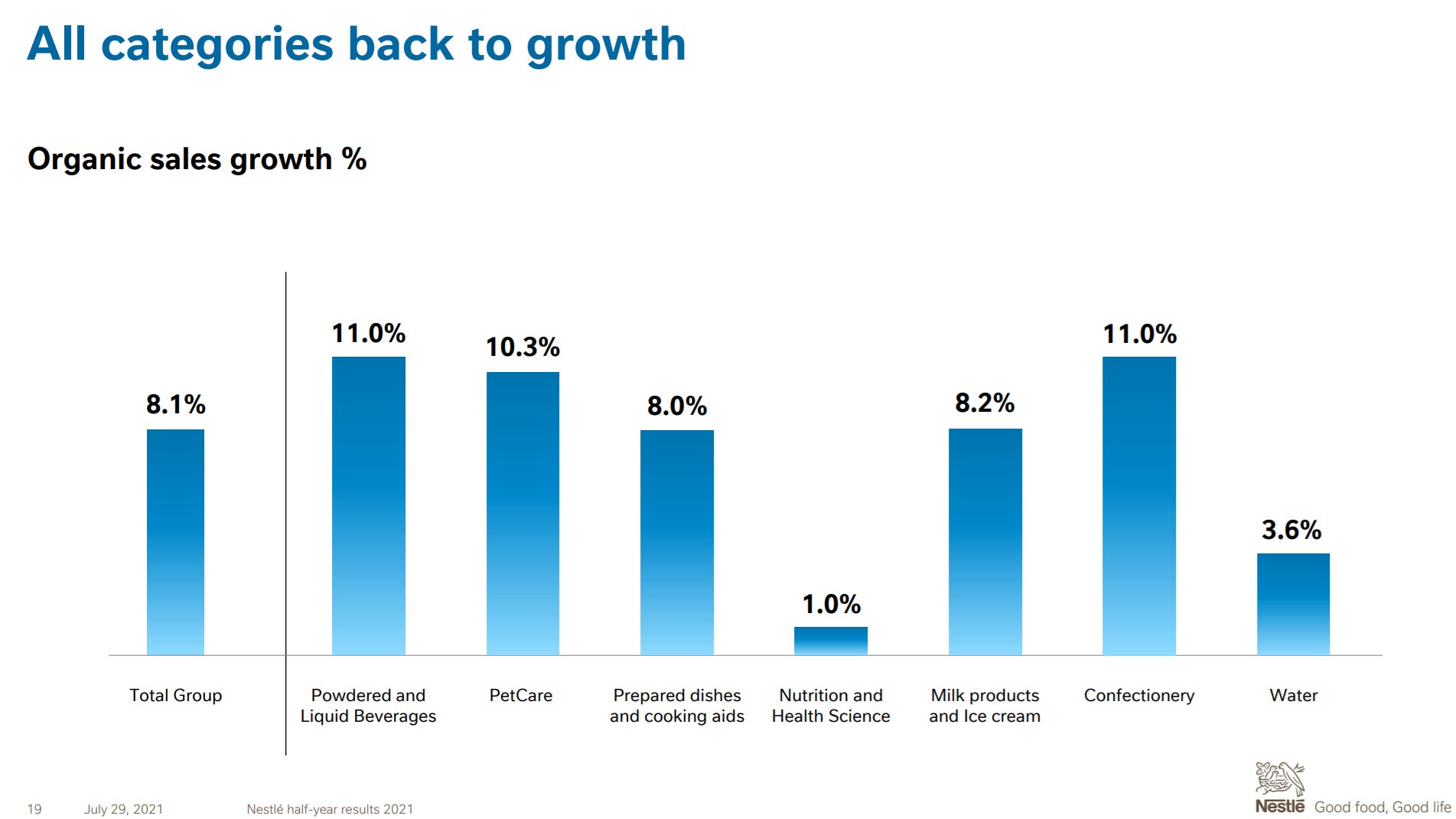

Nestle reported a strong +8.1% organic sales growth in the first half of the year, the highest in a decade. They raised its full-year organic sales growth guidance to 5-6%. Coffee was the largest contributor to organic growth. Nestle highlighted some short term margin pressure as well, but Mr Market was ok with that.

We expect full-year organic sales growth between 5% and 6%. The underlying trading operating profit margin is now expected around 17.5%, reflecting initial time delays between input cost inflation and pricing as well as the one-off integration costs related to the acquisition of The Bountiful Company's core brands. Beyond 2021, our mid-term outlook for continued moderate margin improvement remains unchanged. Underlying earnings per share in constant currency and capital efficiency are expected to increase this year.

All categories are growing:

Spirits have good pricing power and don’t seem to care much about cost inflation.

Campari celebrated 20 years on the stock market, and a 16% TSR since IPO, with a +22.3% organic growth vs the first half of 2019. On-premise channels bounced back while home consumption remains resilient. EBIT margin expanded 190bps vs 2019.

Campari Group celebrates 20 years on the stock exchange: 15 times increase in market capitalisation to €13 billion and annualized Total Shareholder Return of 16% since IPO1, with significant outperformance of market index and industry peers

Diageo is a giant and not growing as fast as Campari, but still its FY21 preliminary results showed sales 6% above 2019 levels, with North America leading at +24%.

Diageo did not want to feel left out and, similar to Campari, reminded us it has been a good investment: +13% CAGR in the last 10 years. I don’t know why they went back 10 years only, as Diageo has been compounding at 13% ca for 30+ years!

Beers are not spirits. ABInbev Q2 2021 results, the first in the Post-Brito era, showed revenues +3.2% above 2019 levels. Growth was above expectations but margins disappointed. Similar to Reckitt, the stock did quite poorly this week.

Cosmetics is another category with good pricing power. No mention of inflation in L'Oréal H1 results. Revenues grew almost 21% and margins expanded. E-commerce accounts for 27.3% of sales.

The first-half results increased sharply and are of excellent quality. They are evidence of the L’Oréal virtuous circle: a strong improvement in gross margin combined with good cost control has enabled us to invest significantly in developing our brands and deliver once again an increase in profitability.

Moving to other sectors, the pest control and disinfection services Rentokil posted good numbers and “expect market consensus to increase”:

“Assuming trading conditions around the world continue to improve and are not significantly impacted by rising cases of new COVID-19 variants, we anticipate mid-single digit organic growth in our core businesses for 2021 and, despite the anticipated tapering off in disinfection presenting more challenging comparatives in the second half, we expect market consensus for full year adjusted pre-tax profit to increase by around £10m to £15m.”

Ryanair, the largest European airline, increased their traffic outlook:

Ryanair… believes that FY22 traffic (March 2022) has improved to a range of 90m to 100m (previously guided at the lower end of an 80m to 120m passenger range) and (cautiously) expect that the likely outcome for FY22 is somewhere between a small loss and breakeven. This is dependent on the continued rollout of vaccines this summer, and no adverse Covid variant developments.

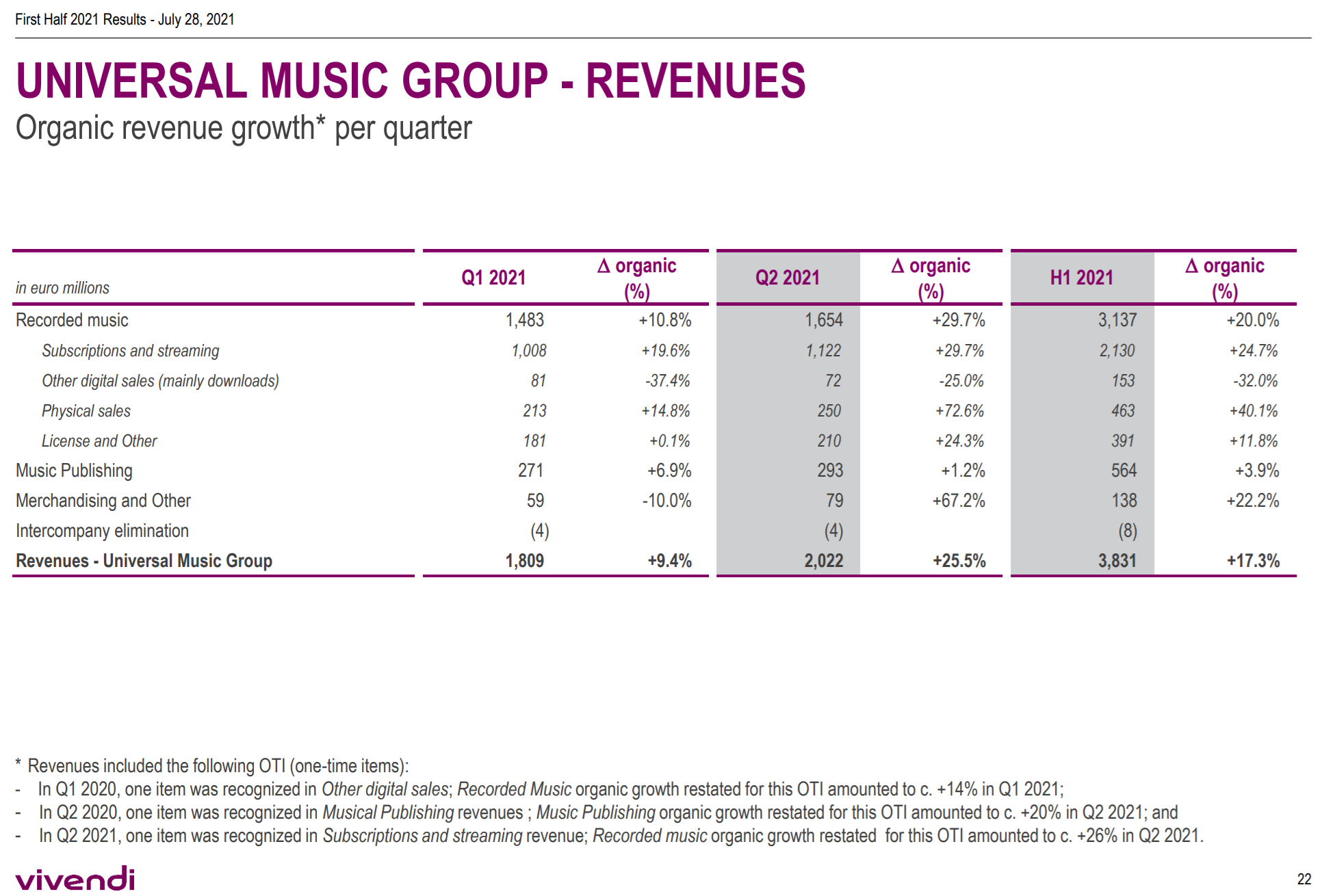

Vivendi sales increased +11.9% in the first half. UMG sales were up +17.3% (recorded music +20%). UMG will be listed on September 21st.

Other news

CatRock complained about Just Eat Takeaway communication (link)

Tencent Investor Prosus Slumps Amid China’s Ed-Tech Crackdown (link)

Is the hard seltzer boom starting to fizzle out? (link)

Deliveroo could leave Spanish market ahead of on-demand labor reclassification (link)

Bernard Arnault passed Jeff Bezos to become the world's richest person

Have a great week and good investing!

If you are not a subscriber, please sign up to get full access and never miss an update. If you like what you read, please share it with your colleagues and friends.

Disclaimer: this newsletter is for informational purposes only and does not represent investment advice. I might have a position in some of the stocks discussed. Always do your own research before investing. Your feedback is important - please contact me on Twitter