Investing in Europe #31

Investing in Europe #31

Beers and pizzas. Sportswear, sports cars and more

Welcome to a new issue of Investing in Europe, a weekly curated newsletter on what’s happening in European companies and markets.

Your feedback is very important. Please comment below or DM me on Twitter. If you are not a subscriber, please sign up to get full access and never miss an update. 🙏

Company news and results

Dear reader, another exhausting week of earnings is over. We are almost done, 80%+ of European companies have reported. Numbers are “better than expected”, which in many cases means last year was awful (it was). Expectations matter and probably explain a lot of the short term price changes after earnings, but the underlying business fundamentals are what matters the most.

In the first half of 2021, Heineken net revenue increased +14.1% organically compared to 2020, but remained below 2019 levels as the on-trade channels have not fully recovered yet. The operating margin was strong, with some help from cost-cutting and lower marketing expenses.

Profitability was much better than expected but, similar to other staples companies, the H2 outlook sounded cautious due to inflation pressures:

Yet there is reason for caution too. Firstly, COVID-19 remains a factor, with the biggest impact currently in key markets in Asia and Africa. Secondly, we see a rise in commodity costs, which, at current levels, will start affecting us in the second half of this year and have a material effect in 2022. Overall, we expect full year financial results to remain below 2019."

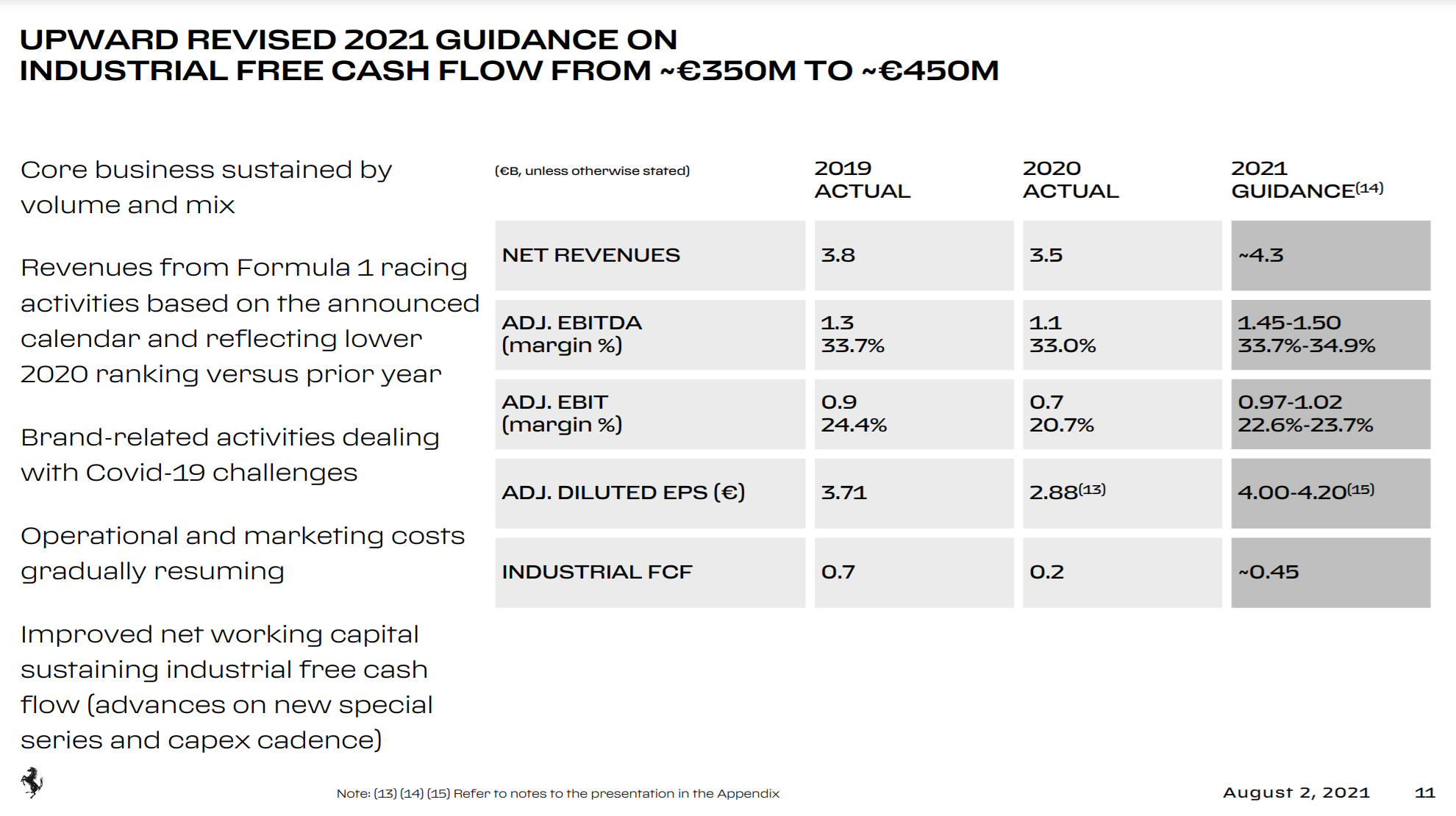

Ferrari revenues increased +5.2% in the second quarter of 2021 compared to 2019 (1.8x vs 2020…). Operating profit was up almost 15% on a 2-year stack, as margin expanded from 24.3% 2 years ago to 26.5% last quarter. June was a record month in terms of orders. The Free Cash Flow guidance was upgraded, from €350mn to €450mn.

Chairman and Acting CEO John Elkann said:

This excellent second quarter confirms the strength of Ferrari and of its unique business model. With each Ferrari we unveil we are setting new benchmarks for innovation, beauty and distinctiveness which is the only true luxury. As we move towards our 75th anniversary next year, our opportunities have never been wider and greater.

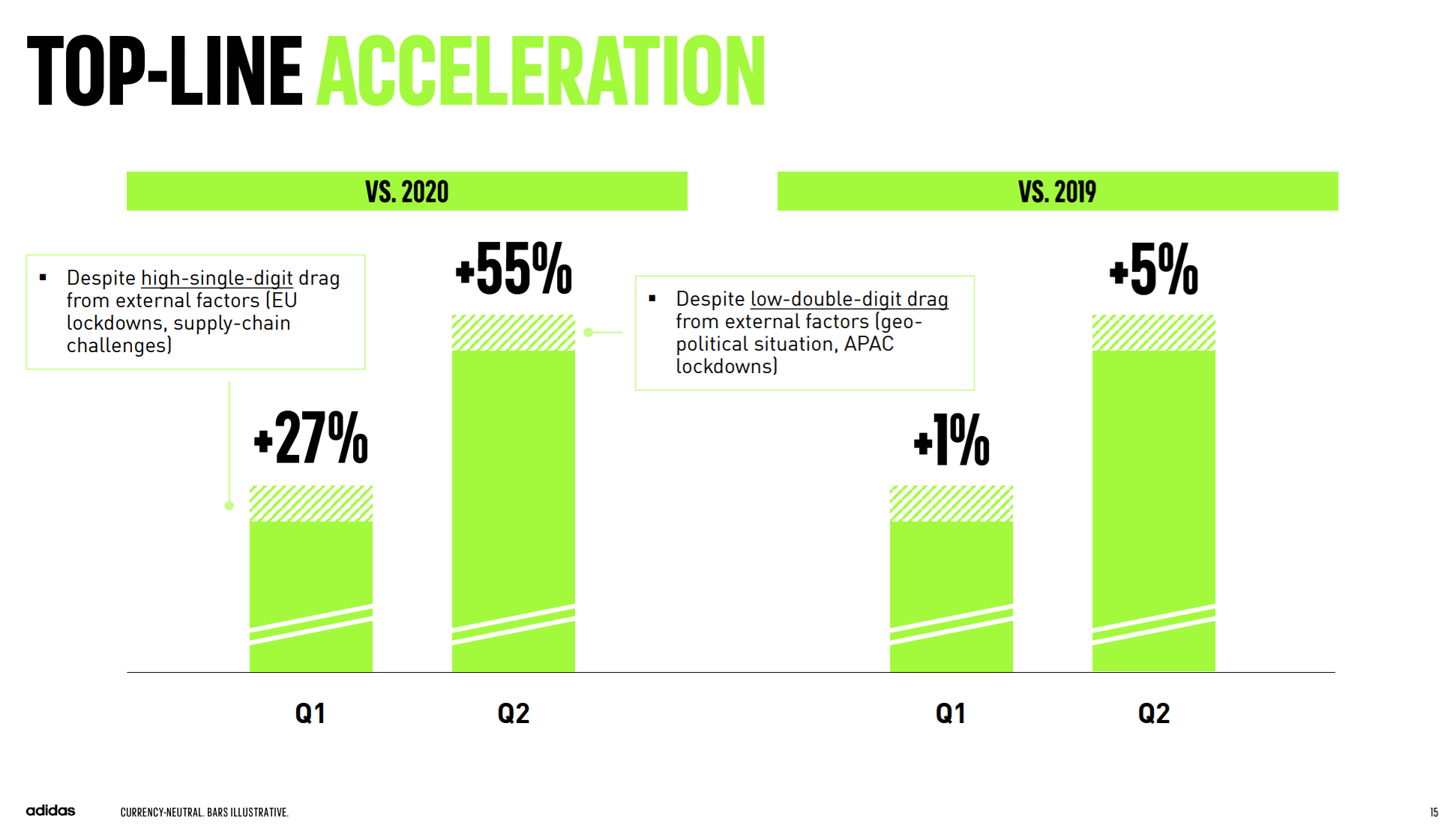

Adidas reported a +55% increase in sales in Q2 compared to last year and +5% vs 2019. China was the weak spot, as revenues declined 16% during the period. The geo-political tension eventually had an impact, it seems. Sales trend in China improved toward the end of the quarter, they commented.

2021 sales guidance was increased from high-teens net sales growth to up to 20%. Net income to €1.4-1.5bn:

While Adidas continues to be impacted by Covid-19-related lockdowns, industry-wide supply chain challenges and the geo-political situation, the company has increased its top- and bottom-line outlook for 2021.

Given the accelerating top-line momentum, the company now expects currency-neutral sales to increase at a rate of up to 20% year-over-year in 2021, driven by strong double-digit improvements in all markets. This new outlook reflects sales growth of up to 7% in the second half of the year compared to the 2020 level…

…The company’s full-year gross margin forecast continues to be for a level of around 52.0%. The operating margin is now expected to increase to a level of between 9.5% and 10% (previously: 9% to 10%). Net income from continuing operations is now projected to increase to a level of between € 1.4 billion and € 1.5 billion (previously: € 1.25 billion to € 1.45 billion).

Wolters Kluwer, the Dutch publishing and information services company, reported a 5% increase in revenues in the first half of 2021 and a 170bps expansion in operating margin.

HelloFresh updated its FY21 guidance. Stronger sales but weaker profitability, explained by higher investments:

Based on the Company's strong growth performance year-to-date, driven by strong customer growth and continued high order rates, its management board decided today to increase the Company's full year 2021 revenue growth outlook for the HelloFresh Group on a constant currency basis from previously between 35% and 45% to now between 45% and 55%.

…the Company now expects a full year 2021 AEBITDA margin for the HelloFresh Group between 8.25% and 10.25% compared to previously between 10% and 12%

Domino’s Pizza Group, the UK master franchise of Domino’s, reported a +5.5% increase in system sales (ex store splits and the benefit of the VAT cut introduced in July 2020). Total orders were up 3.5% in the first half. In case you are wondering, the England vs Scotland match was their highest recorded trading day this calendar year.

As for the relationships with franchisees:

Constructive engagement with our franchisees continues as we work together to reset our relationship to drive growth of the system – implemented new incentives to accelerate new store openings

Novo Nordisk’s net profit increased by 10% in the first six months of 2021. Stronger than what most expected. The outlook was increased:

For the 2021 outlook, sales growth is now expected to be 10-13% at CER (previously 6-10%), and operating profit growth is now expected to be 9-12% at CER (previously 5-9%)

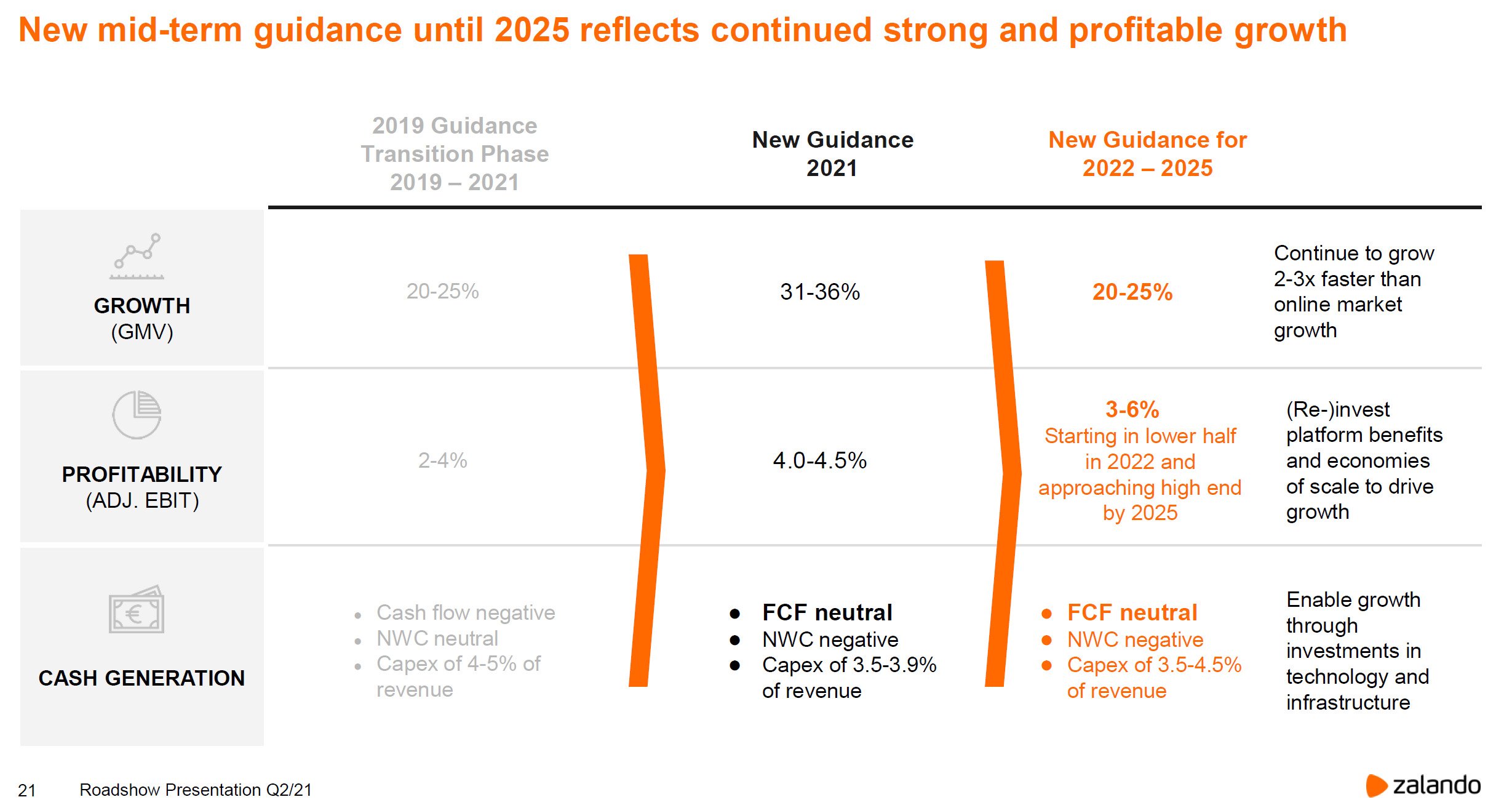

The online fashion platform Zalando delivered GMV growth of +40% in Q2 to €3.8bn. Adj EBIT% was 6.7%. They reached 44.5mn customers at the end of the quarter, with average orders per active customer reaching a new all-time high of 5.0. Zalando raised its adj EBIT guidance to the upper half of the previously guided range of €400-475mn, but kept the GMV guidance unchanged at +31-36%. The partnership with Sephora will start in Q4.

London Stock Exchange Group reported a +4.6% growth in total income in H1. Adj EBITDA margin was 49.4%. As for the integration of the data business Refinitiv:

Good progress on the integration of Refinitiv with £77 million of run-rate cost synergies realised at H1; full year guidance for run-rate cost synergy delivery increased from £88 million to £125 million; and 27 new products launched as part of revenue synergy programme

Symrise, the flavours and fragrances company, reported a 9.7 % increase in sales in the first half of 2021 (Q2 +8.8%) and upgraded its full-year guidance to above 7%, from 5-7% before.

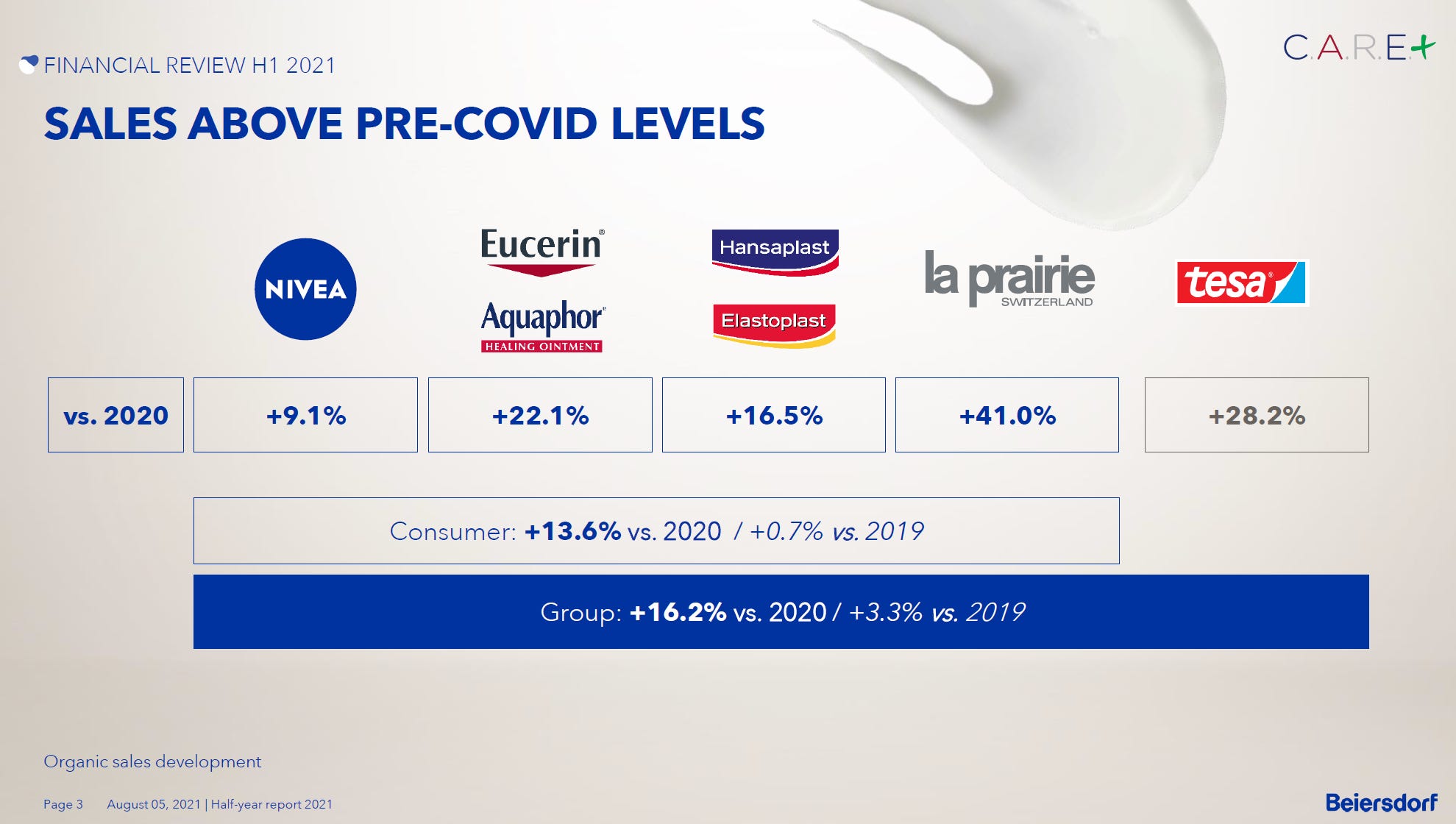

Nivea's producer Beiersdorf reported in H1 a +16.2% increase in sales vs 2020, +3.3% vs 2019. EBIT% recovered to 15.3% in the first half but, for the full year, is still expected at previous year’s level of 12.9%, as guided before. Sales guidance remained unchanged as well (high single-digit growth).

M&A and IPO

DoorDash in talks to invest in German grocery app Gorillas - at a valuation of about $2.5bn (link)

SoftBank Builds a $5 Billion Stake in Pharma Giant Roche (link)

UK's Morrisons agrees to raised $9.3 bln offer from Fortress-led group (link)

Carlyle Raises Offer for Vectura, Elbowing Out Philip Morris (link)

Other news

A new research note by Mauboussin - Everything Is a DCF Model

A Mantra for Valuing Cash-Generating Assets

We suggest the mantra “everything is a DCF model.” Whenever investors value a stake in a cash-generating asset, they should recognize they are using a discounted cash flow (DCF) model.

This suggests a mindset that is very different from that of a speculator, who buys a stock in anticipation that it will go up without reference to its value.

The topic deserves attention because many market participants don’t think DCF models are relevant, and many use heuristics for value without recognizing the purpose and limitations of the shorthands.

The intrinsic value, determined by the present value of future cash flows, attracts the price like a magnetic force. This means it is useful for investors to keep in mind the value drivers of a discounted cash flow model.

The Tokyo Olympic Games are over. Here’s who won what.

Have a great week and good investing!

If you are not a subscriber, please sign up to get full access and never miss an update. If you like what you read, please share it with your colleagues and friends.

Disclaimer: this newsletter is for informational purposes only and does not represent investment advice. I might have a position in some of the stocks discussed. Always do your own research before investing. Your feedback is important - please contact me on Twitter