Investing in Europe #33

Investing in Europe #33

Just Eat Takeaway, Carlsberg, Adyen and more

Dear reader, hope you are having a good summer 🕶️

A few things that happened in Europe this week 👇

Company news and results

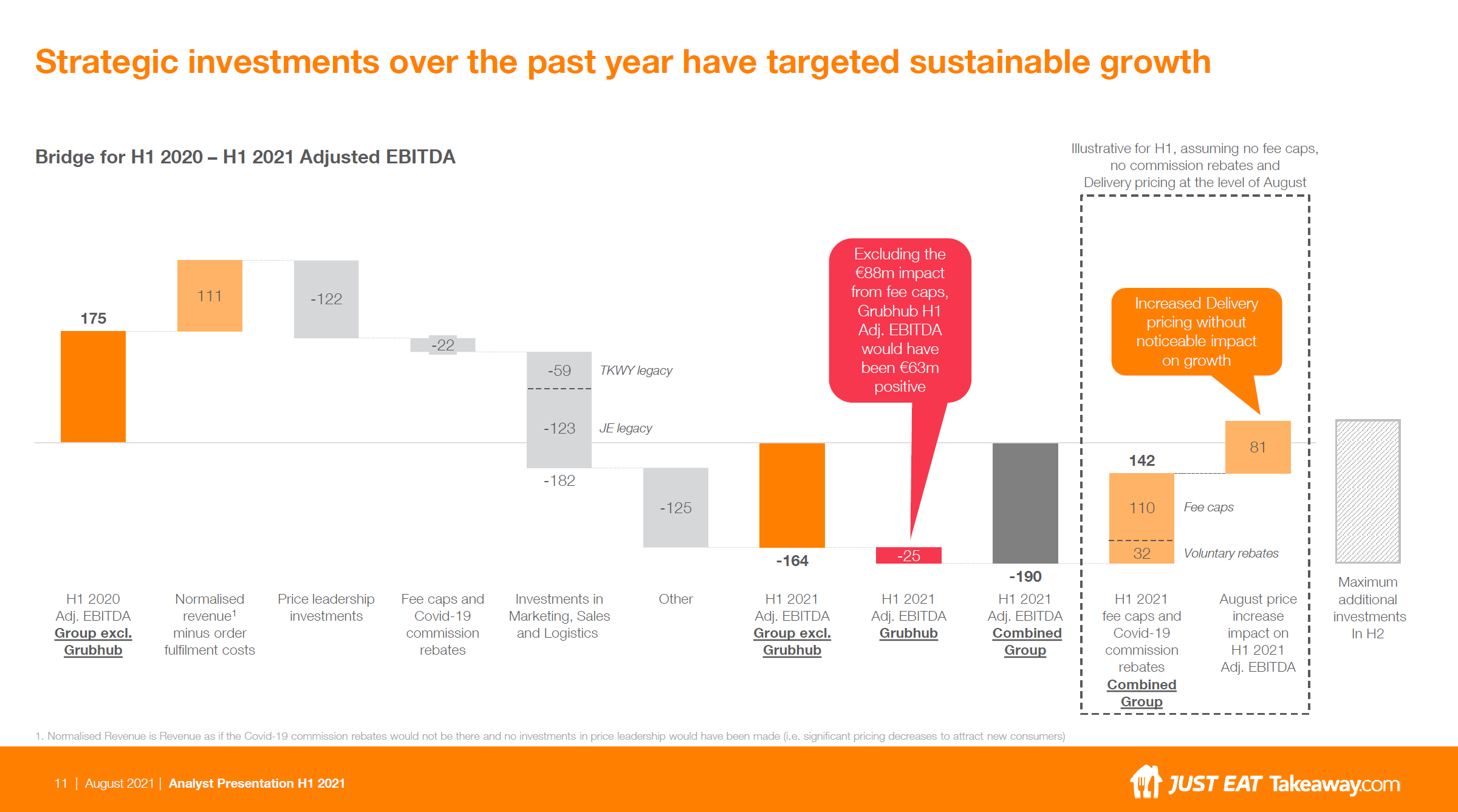

Just Eat Takeaway reported its half-year 2021 results. Orders (+51% pro forma) and GTV (+50% constant currency) were pre-released last month. This week it was about revenues and profits.

Key “takeaways” 😐:

Revenues increased +52% to €2.6bn, including Grubhub, or +63% excluding it. The growth rate is higher than both orders and GTV as delivery orders went from 31% to 43% of total (higher commissions)

That jump in delivery orders was quite painful: EBITDA adj went from EUR +175mn to -190mn. Most of the investments went to Just Eat legacy markets, as already discussed

They showed EBITDA would have been positive excluding Covid-19 related fee caps and commission rebates, and assuming delivery pricing at the level of August (no more free-delivered McDonald's in London)

The 2020 cohort has ordered nearly as much in H1 2021 as in the whole year 2020

Covid-19 related commission fee caps (€142 impact in H1) have been prolonged in some regions, but the full-year guidance has been reiterated

Groceries: in Canada, they are testing dark stores; in Europe, partnerships

The logistic company DSV completed the acquisition of Agility GIL and raised its 2021 outlook:

EBIT before special items is expected to be in the range of DKK 13,750 - 14,500 million (previously DKK 12,500- 13,000 million). Approximately DKK 750 million of the upgrade is related to the expected impact from GIL, and the rest to the performance of the existing DSV business

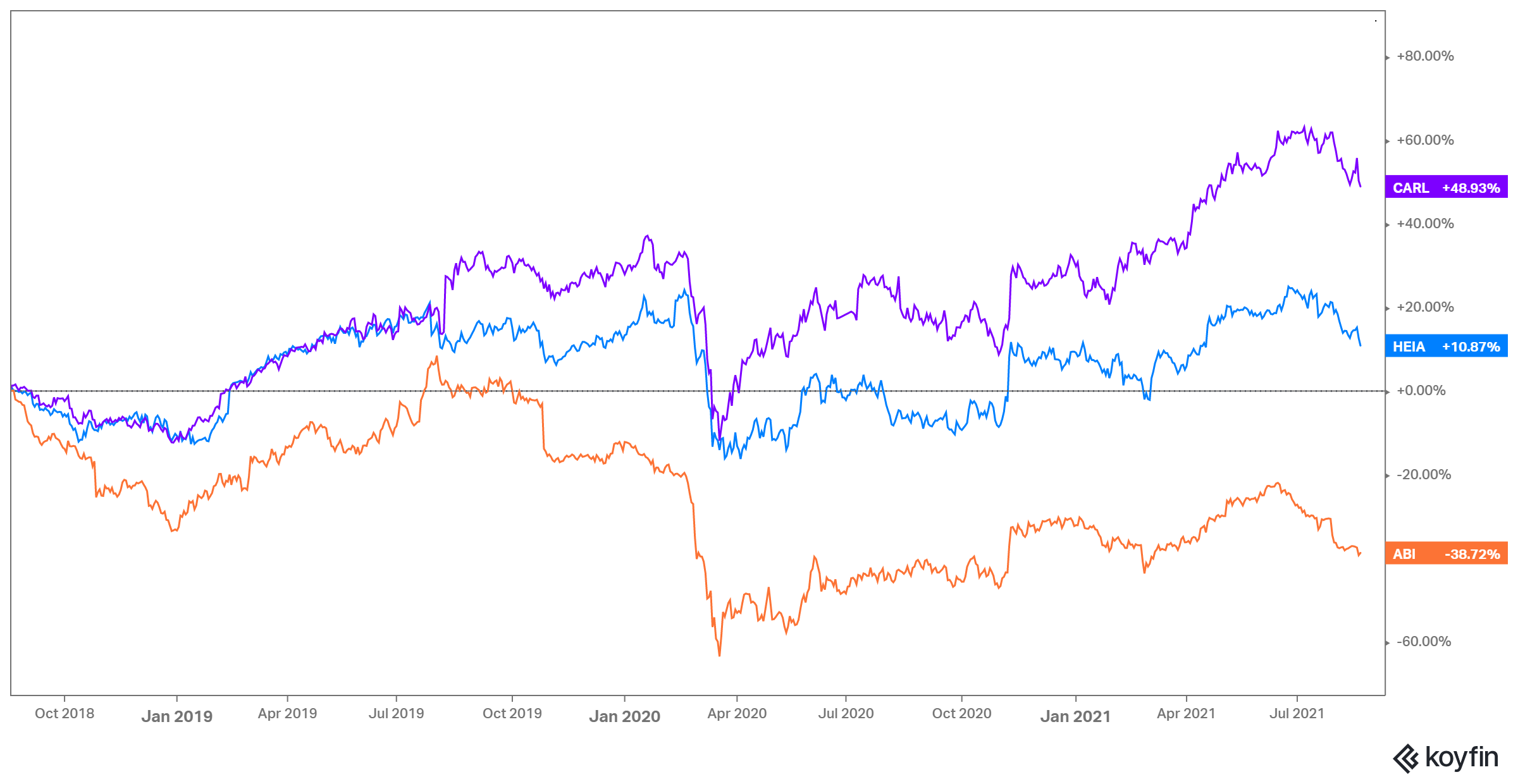

Carlsberg grew its sales by +14.3% in Q2, raised the 2021 earnings guidance and launched a new share buy-back programme:

The COVID-19 pandemic continues to impact business performance, and market volatility and uncertainty remain high. However, in light of the good results for H1 and the start of Q3, we upgrade the earnings guidance for 2021:

• Organic growth in operating profit within the range of 8-11% (previously 5-10%).

• A translation impact of around DKK -150m is assumed for 2021 based on the spot rates at 17 August (previously DKK -250m).

In contrast to other beer companies, volumes are already above 2019 levels as Carlsberg has been less exposed to on-trade heavy markets.

Adyen reported a very strong H1. From the shareholder letter:

We processed €216.0 billion during the period, up 67% year-on-year

Net revenue was €445.0 million, up 46% year-on-year

EBITDA margin was 61% for the period, up from 54% in H1 2020

Free cash flow was €246.4 million, up 60% year-on-year from €154.2 million in H1 2020

majority (>80%) of our growth coming from merchants that were already on the platform

H1 2021 POS volume was €22.8 billion, making up 11% of total processed volume. Despite global lockdowns impacting growth in the in-store segment, POS volume doubled in absolute numbers