Investing in Europe #35

Investing in Europe #35

Pernod Ricard, CCEP, a thread on quality investing, even the best make mistakes

Dear subscriber, I hope you are well. Thank you for reading, sharing and giving your feedback. I am enjoying interacting with many of you. As usual, you can comment below or DM me on Twitter.

A few things that happened in Europe this week 👇

Company news and results

Pernod Ricard 🥃 reported a +18.3% increase in organic EBIT in FY21. Better than the +16% guided last June, when they raised their guidance from +10%. Sales were up +9.7%, with a very strong increase in China (+44%), and the US (+16%). Recurring Free Cash Flow was more than €1.7bn, a historical high.

We know that spirits navigated the pandemic very well, as the off-trade channels remained strong. As for FY22, there is no explicit guidance but they expect “a very dynamic” first quarter.

Medium-term guidance unchanged:

+4 to +7% topline growth, leveraging key competitive advantages and consistent investment behind key priorities

Focus on pricing and building new operational excellence initiatives

Significant A&P investment, maintained at c.16% of Sales, with strong arbitration to support must-win brands and markets while stimulating innovation

Discipline on Structure costs, investing in priorities while maintaining agile organisation, with growth below topline growth rates

Operating leverage of c.50-60 bps pa, provided topline within +4 to +7% bracket

Finally, if you are worried about the potential of the “common prosperity” policies in China, this is what the CEO Alexandre Ricard said in the call:

Well, so regarding your question on China, listen, my understanding, my take on what I read over the summer and what I heard is that the intent of the country is really to support the emergence of middle-class households. And by the way, our strategy which we shared with you was to leverage middle-class Chinese households as they emerge and to increase our penetration in the Chinese market. So all in all, from that point of view, if indeed, we see increase -- an increase in purchasing power and the acceleration of the growth of middle-class households, I would say, in fact, it could be a positive. So obviously, I will keep on following very closely what happens from that point of view. But my take is the focus of the country is on the emergence of middle-class households and our focus is as well.

bioMérieux, the French in vitro diagnostics company, reported a +12.3% increase in sales in the first half of 2021.

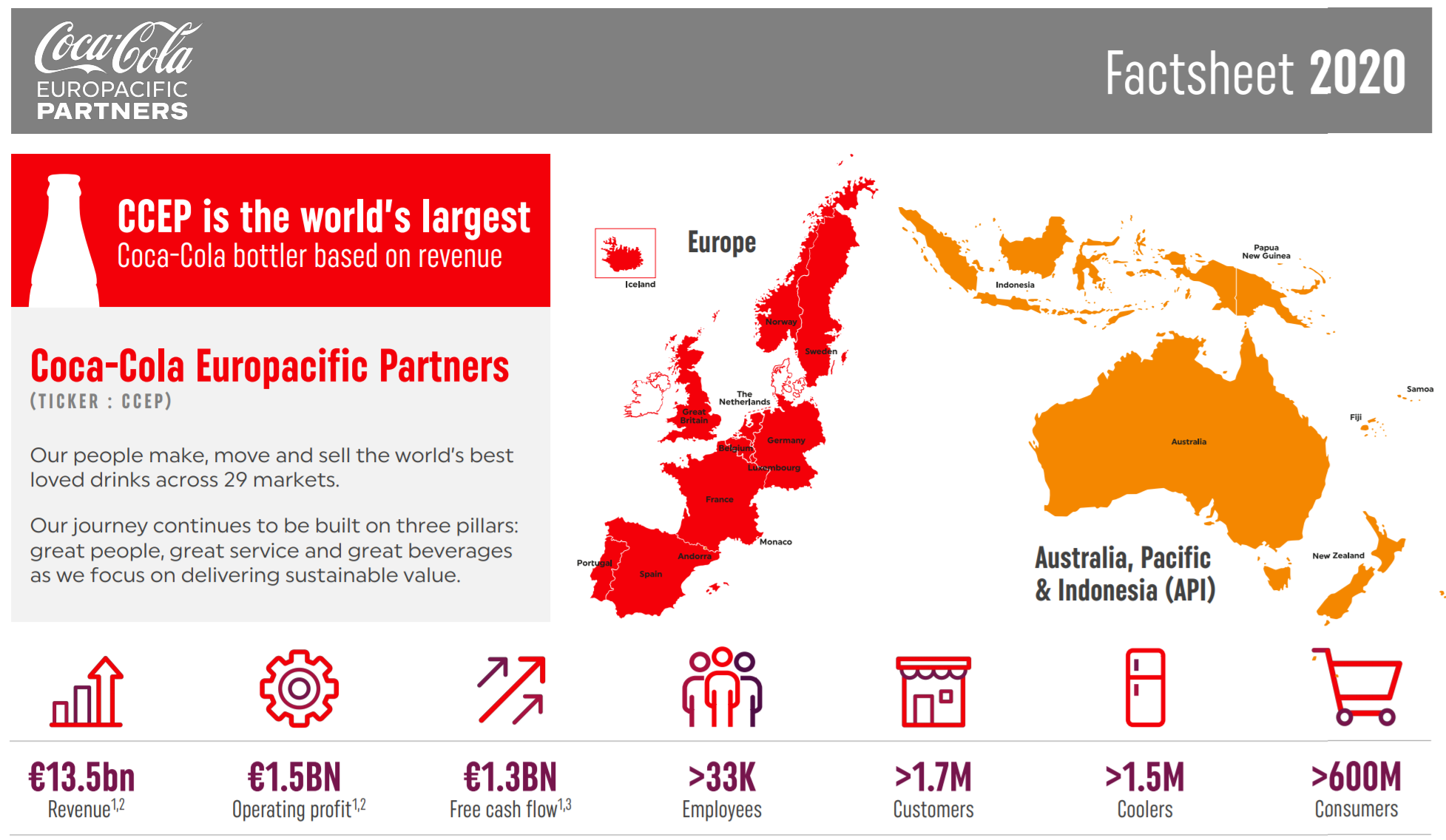

Coca-Cola Europacific Partners (CCEP) reported better than expected H1 2021 results, with sales up +11.5% pro forma, and issued a strong FY21 guidance:

The outlook for FY21 reflects our current assessment of the scale and magnitude of the COVID-19 pandemic, which is subject to change as we continue to monitor ongoing developments. Guidance is on a comparable basis, reflecting the timing impact of the acquisition of API which completed on 10 May 2021, and based on actual FX rates.

• Revenue: comparable growth of 26-28%

• Operating profit: comparable growth of 40-44%

• Comparable effective tax rate: ~20%

• Dividend payout ratio: c.50%

CCEP is the world’s largest Coca-Cola bottler by revenues, born by the combination of Coca-Cola European Partners and the Australian bottler Coca-Cola Amatil:

A thread on Quality Investing 📘

I had some extra time during last Monday's Bank Holiday to write a thread on the book Quality Investing. I am really glad people liked it. Lawrence Cunningham himself retweeted it! It is one of the books that helped me to understand how to recognise a good company.

Click on the tweet below for a list of common patterns and some examples 👇

Deals and IPO

Prosus acquires Indian payments giant BillDesk for $4.7B, will merge with its PayU fintech group (link)

Swedish drugmaker Swedish Orphan Biovitrum soars on $8 bln bid from Advent and Aurora Investment (link)

Other news

EssilorLuxottica announces launch of share buyback program (link)

Luxury billionaire Arnault sells out of retailer Carrefour (link) - even the best make mistakes:

…stake was sold at 16 euros per share, after Arnault, alongside Colony Capital and Axon Capital, first took a 9.8% holding in 2007 at an average price of 47 euros per share

Bill Ackman exercised the right to acquire another 2.9% of Universal Music (link)

A statistically insignificant poll on who is going back to the office: