Investing in Europe #36

Investing in Europe #36

B&M, Exor, Ferragamo. Tons of stock offerings.

Company news and results

The private equity company Partners Group is having a record year, which is what you would expect in these markets:

Considering the strong results in H1 2021, Partners Group foresees the potential for performance fees to represent 40-45% of total revenues for the full-year 2021, assuming market conditions and the exit environment remain unchanged. This also anticipates the potential for some performance fees originally expected in 2022 to be brought forward as a select number of programs and mandates may meet their hurdle rates earlier than anticipated. For the full-year 2022, performance fees are expected to return within the range of 20-30% of total revenues. Over the mid to long term, the firm continues to expect its performance fee potential to grow in line with AuM.

The UK discount chain B&M issued a positive trading update:

Whilst Group revenues year to date have been broadly in line with market expectations, gross margins have been stronger than originally anticipated in the B&M UK fascia business

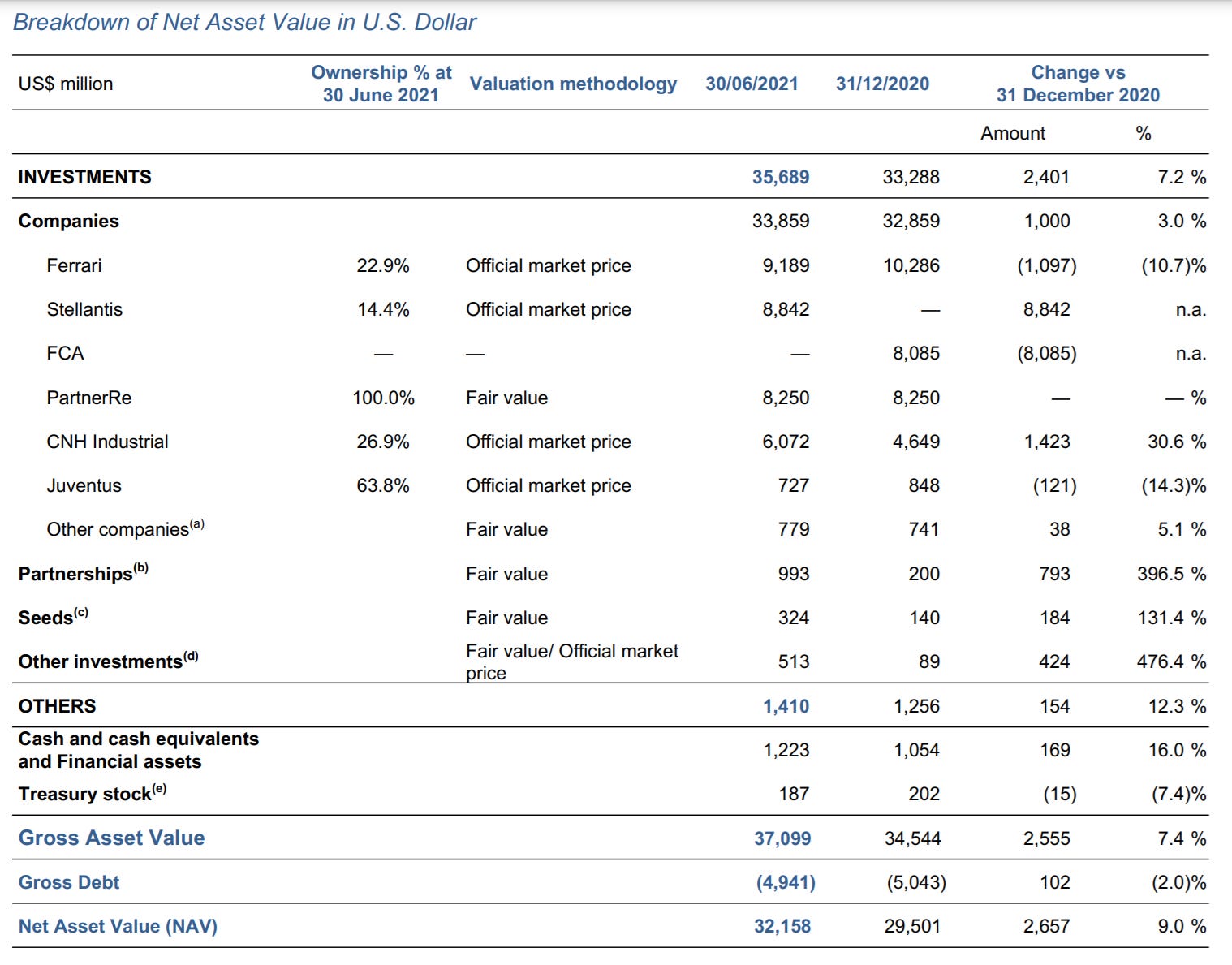

Exor reported its half-year results. NAV per share increased 9% to $136.54 (€114.89) compared to $125.26 (€102.08) at 31 December 2020:

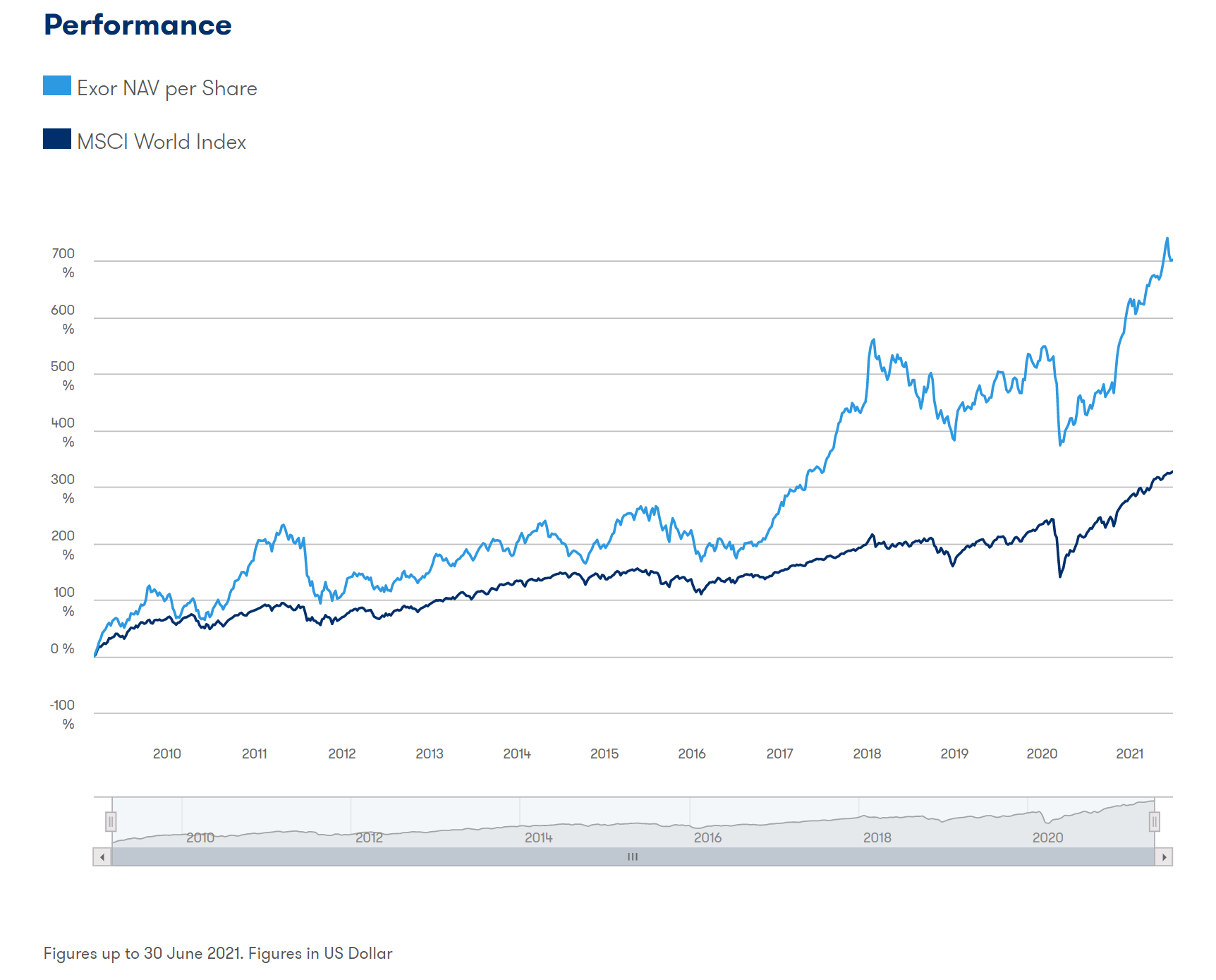

Whilst the 9% increase in NAV year to date is below the MSCI World Index performance of 12.2%, Exor’s historical outperformance has been amazing:

Ferragamo reported its full H1 2021 results (sales were reported - still below 2019). Margins were good, thanks to a better sales mix. Marco Gobbetti will join as CEO from Burberry in the next months, to revamp the strategy.

In other news, the Ferragamo family is opening its first London restaurant (Il Borro - the first one was opened in Dubai).

Safestore, UK’s largest and Europe’s second largest provider of self-storage, has reported an almost 20% increase in sales in Q3. Apparently, those storage units you might see while driving are 80%+ occupied. EPS are expected to grow 31%-32.5% compared to last year.

Deals and IPO

Things you don’t see at the bottom:

So many IPOs this week. I lost count, but here are a few names: Exclusive Networks, Azelis, Medmix, Babbel, Majorel, Neogames, Oxford Nanopore (to be launched) 🤷♂️

Back-To-School Season Has Stock Sellers Tapping Market in Droves ($link) - busiest start of September globally since 2012, according to Bloomberg 💰

Other deals:

EasyJet Rejects Wizz Air Takeover Bid (link) - this could have been an interesting one. Wizz is one of the lowest cost European airlines, with a strong presence in Eastern Europe. EasyJet has some strong positions in a number of key Western Europe airports

Deutsche Telekom lifts T-Mobile U.S. stake in SoftBank swap deal (link)

London Rivals Closing the Gap in Race for Europe’s Top IPO Spot ($link) - $17bn raised this year in London compared to roughly $11bn in Frankfurt and Amsterdam, according to Bloomberg

Other news

Airbus Sees Strong Order Intake, Delivery Stability in August (link) - August was the best month for sales since the onset of the pandemic

Delivery companies sue New York City over permanent 15% fee cap (link)

Hong Kong Moves to Reopen China Border, Boosting Retail Stocks (link)

Aperol launches on-the-go Aperol Spritz Kit (link)