Investing in Europe #5

Investing in Europe #5

Reporting season, Corporate Events, M&A and IPOs

Hello. Welcome to Investing in Europe, a weekly newsletter on what’s happening in European companies and markets, filtered for what matters.

I have been investing in Europe for over a decade and here I share some of my thoughts. You can find me on Twitter.

This newsletter is for informational purposes only does not represent investment advice. Always do your own research before investing.

Subscribe to get full access and never miss an update.

Companies results

Unilever: the Food and HPC giant reported their Q4 and FY20 numbers. Markets didn’t like the miss on margins and the ongoing restructuring costs.

Underlying growth was in line with expectations, +1.9% for the year and +3.5% for the Q4. But margins disappointed, as underlying EBIT% was 18.5%, 60bps lower than 2019. They introduced five strategic points and reinstated their 3-5% underlying sales growth target. The same target they had pre-Covid. Again, markets were not impressed. They did 3% on average 2017-19.

Unilever still expects profits to grow faster than sales, implying some margins expansion, but they announced restructuring investment of around €1 billion for 2021 and 2022 (and lower thereafter). Recurring restructuring costs are not great, although not necessarily bad if growth will eventually accelerate, which is probably what markets want to see. Free Cash Flow was probably the best number in the release, at €7.7bn or a 6% FCF yield.

Carlsberg: another company impacted by the pandemic, reported organic revenues down -8.4%. They did better on operating profits, down only -3.1%. Western Europe was the weakest region due to restrictions and lockdowns, as revenues went down -12.8%. They expect 2021 organic growth in operating profit within the range of 3% to 10%.

Publicis, the French multinational advertising and public relations company had a mixed year with organic growth at -6.3%.

Infineon raised their outlook for the year.

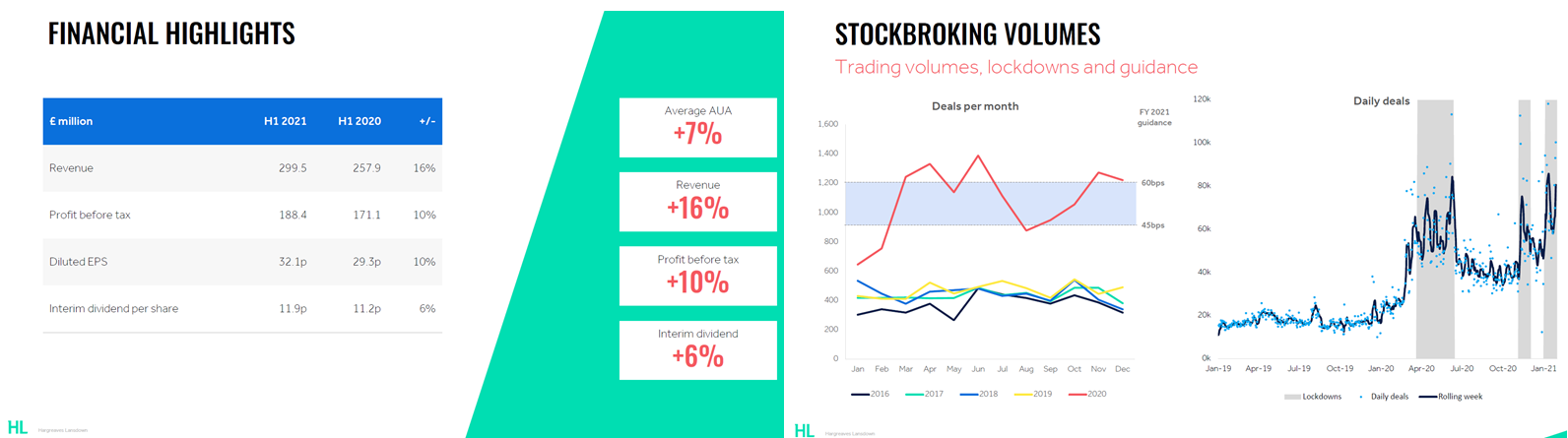

Hargreaves Lansdown, the UK’s leading investing platform for private investors, had a good year. They added more than 221k new clients, increased revenues by 16% and EPS by 10%. It seems people traded much more than usual, as volumes went up +123%.

Compass: the foodservice industry has been severely affected by the pandemic. They issued a trading update for the three months to December 2020 (Q121 for them), with organic revenues down -33.7%. A tiny improvement from the -34.1% reported in the previous quarter. On the positive side, profitability is improving as operating margins went from 0.6% in the last quarter to 2.7% this quarter.

Ryanair: just one slide to show the Covid-19 impact on traffic:

Corporate events

Just Eat Takeaway raised €1.1bn in a convertible bond offering. Link

M&A and IPO

Marston’s received and rejected a 105p-per-share takeover proposal from Platinum Equity Advisors. Link

Cellnex buying more towers

Moonpig and Auto1 had a good IPO debut

Thank you for your time and have a good week!