Investing in Europe #8

Investing in Europe #8

Ryanair vs Reckitt, Hotels, AB Inbev and others

Hello. Welcome to Investing in Europe, a weekly newsletter on what’s happening in European companies and markets, filtered for what matters. I have been investing in Europe for over a decade and here I share some of my thoughts.

You can find me on Twitter. Your feedback is welcome!

Subscribe to get full access and never miss an update.

Ryanair vs Reckitt Benckiser

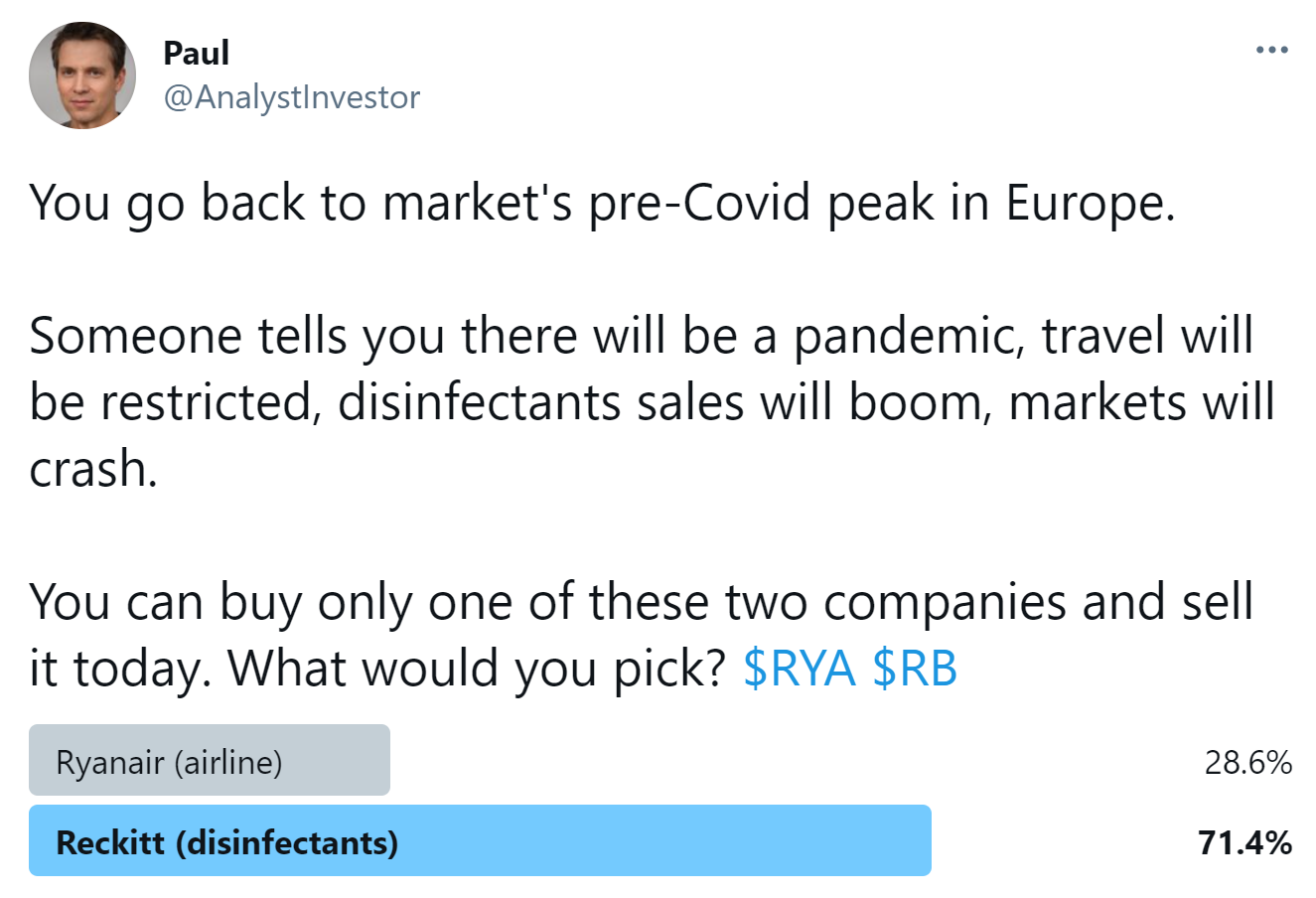

This week I asked on Twitter what seemed an obvious question:

I would have answered the same. Of course you want to be long disinfectants rather than an airline right before a global pandemic. The number of global travelers dropped 74% in 2020 while disinfectants sales boomed. You might actually want to be short airlines. And you would have been very right and rich, at least in the short term.

What if you had to wait a year before selling?

You would have LOST money on Reckitt Benckiser and you would have MADE money on Ryanair. Even better, you could have been long Ryanair and short Reckitt for a 17% return!

Is there a lesson here?

Disclaimer (1) - Stock picking matters: Ryanair is one of the best managed and most efficient airlines in Europe (World?). There aren’t many airlines trading above their pre-Covid peak (another one is Wizz Air).

Disclaimer (2) - Time horizon matters. I checked these stocks’ performances after a period of strong rotation into Travel & Leisure which started last November (vaccines). It could look very different in a few weeks or months.

The lesson: not only we can’t predict pandemics or any other exogenous shocks. We can’t even predict their impacts if we know they will happen.

The worst of the pandemic is luckily behind us. There is another macro risk everyone is talking about now: interest rates. Do you really think you can i) guess where rates will go and ii) pick the best stocks in that scenario?

As Buffett wrote in Berkshire Hathaway’s 2013 letter:

Forming macro opinions or listening to the macro or market predictions of others is a waste of time. Indeed, it is dangerous because it may blur your vision of the facts that are truly important.

Focus on what matters and you can understand. Study companies. Have a long term investment horizon.

Company results

It has been another busy week of results. I mentioned the overperformance of Travel & Leisure. A few companies reported in this area:

InterContinental Hotels Group (IHG): revenue per available room (RevPAR), a standard measure in the hospitality sector, declined 52.5% in 2020. Daily rates dropped 17% and occupancy almost 30%. There is quite a big gap between China, down 40% ca, and EMEAA, down almost 65%. This is a trend that seems to be continuing in early 2021. Americas RevPAR, the most important region for IHG, dropped 48.5%. Net rooms growth was up +0.3% on the year. (link)

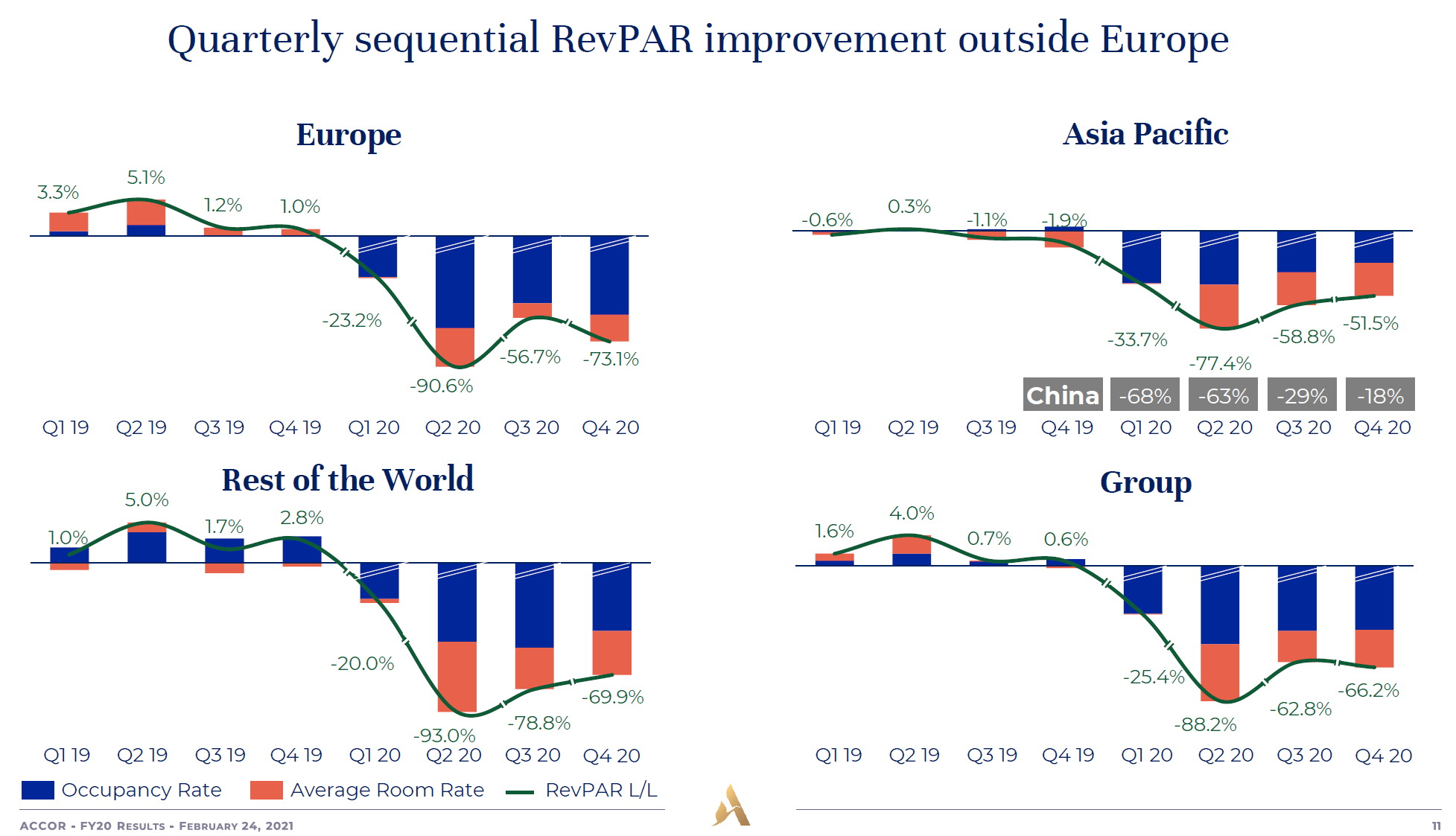

Accor, the largest hospitality company in Europe, had a deeper drop in RevPAR: -62%. Compared to IHG, Accor is more exposed to Europe. The underlying drivers are similar but the business models are slightly different. IHG’s portfolio is mostly franchised (71% of rooms) and managed (28%). Accor has more assets, more fees linked to profits, and in general more operating leverage (they are in the process of becoming a full asset light hotel company). (link)

Amadeus, the travel technology company which works with airlines, travel agencies and other travel players, reported a 61% decline in revenues in 2020. Travel agency air bookings dropped 81.5%, passengers boarded were down 65.4%. (link)

Let’s move to other sectors. Reckitt Benckiser, which now you know underperformed Ryanair since pre-Covid peak, had a very strong 2020 with sales up +11.8%. Great year for Lysol and Dettol. Free cash flow was more than £3bn. But growth is normalising in 2021, as the company expects revenues to be in the range of flat to +2%. Margins are expected to be broadly unchanged. (link)

AB Inbev, the world's largest brewer, reported a 3.7% decline in revenues in 2020. Last quarter was +4.5%. EBITDA was down 12.9%, or weaker underlying due to some one-offs. Net debt was down in absolute terms, but up relatively to EBITDA, to 4.8x. Outlook: “expect our top and bottom line results in FY21 to improve meaningfully”. (link)

Wolters Kluwer, the professional information service company, reported an increase in organic revenues of 2%. 2021 guidance: “mid-single-digit growth in adjusted diluted EPS in constant currencies”. They are buying back shares, up to €350mn this year (50mn done), which is the same amount as 2020. (link)

Teleperformance, the outsourcing company, increased revenues by almost 12%. They expect to growth at least 9% in 2021. (link)

M&A and IPOs

Car Dealer Cazoo Weighs London IPO (link)

Logistic company Kuehne & Nagel buys Asian logistics firm Apex International (link)

LVMH acquires 50% of Jay-Z’s Armand de Brignac Champagne (link)

Vegan milk maker Oatly eyes $10bn stock market float (link)

Vodafone could raise up to €4bn from Vantage Towers IPO (link)

EssilorLuxottica To Sell Assets for Grandvision Deal Approval (link)

Other news

Holiday bookings surge after lockdown exit plans (in UK) (link)

Investors Can’t Get Enough of Europe’s New SPAC Kingpins (link)

Have a good week and good investing!

Disclaimer: this newsletter is for informational purposes only and does not represent investment advice. I might have a position in some of the stocks discussed. Always do your own research before investing.