Investing in Europe #18

Investing in Europe #18

Campari, Zalando, Ferrari, AB InBev and more

Welcome back to a new issue of Investing in Europe, a weekly newsletter on what’s happening in European companies and markets, filtered for what matters. Welcome to our new subscribers! 🥂 Your feedback is welcome, please DM me on Twitter 🙏

If you are not a subscriber, please sign up to get full access and never miss an update.

Company news and results

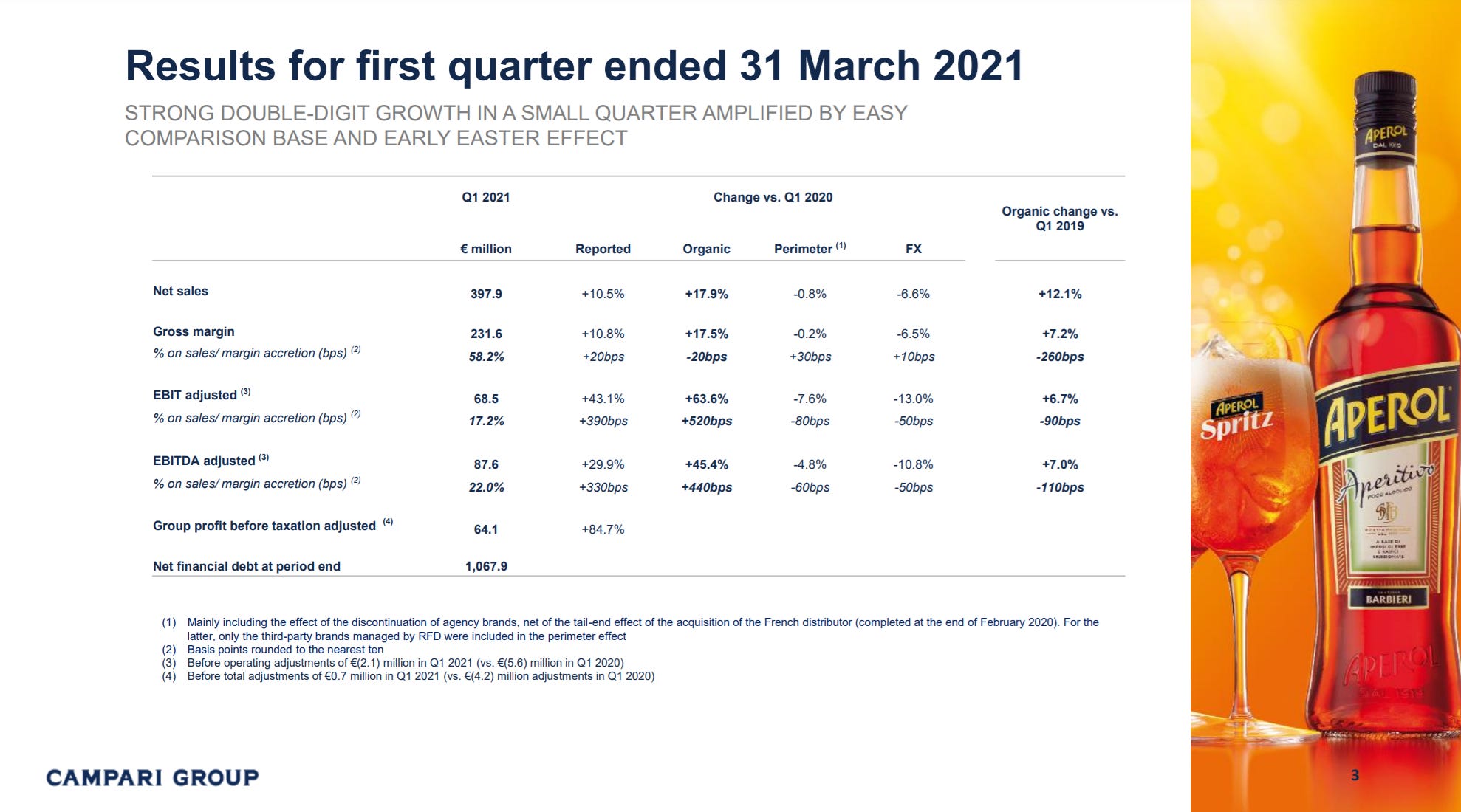

This week we start with a drink 🍹 - Campari reported a 17.9% organic increase in sales in the first quarter of 2021. Easy comp and some boost from early Easter, but still good numbers. Compared to pre-Covid level, sales are up +12.1%. Campari navigated the pandemic quite well, thanks to the US (its biggest market, 32% of sales) and the off-premise markets. Home consumption remains strong. “Southern Europe, Middle East and Africa” is still down as Italy is quite big in the region and has not recovered yet: Q1 2021 sales were almost -25% vs Q1 2019. On an absolute basis EBIT returned to 2019 level as well, while EBIT margin is still below due to sales mix (better margin in on-premise markets). There was no quantitative guidance for the full year, but Campari expects the positive brand momentum to continue.

HelloFresh reported a strong set of numbers in Q1. No big surprises following the recent guidance upgrade discussed in IIE #15.

Ferrari shipped 2771 cars and made €1bn in the first quarter, up 11% at constant currency compared to last year. With 26.3% EBIT%, this is not a car company. The market did not like they postponed the 2022 financial targets by one year. Not a demand issue. Due to Covid-19, they delayed some investments - from the call:

As we have communicated in 2020 and today, we have made a judicious choice of delaying expenditures and the reason we've done it is linked to the uncertainties we are still living through linked to COVID-19 which means that the mix and the deliveries of models are different than what we were expecting. Hence the reason why we are postponing to 2023 the results we were aiming to achieve in 2022. I would also like to make clear that we do have uncertainties on the brand diversification and Formula 1 which we are assessing very judiciously as the months go forward, but it is really on the back of lower expenditures which have a direct consequence on deliveries and mix.

I also would like to reaffirm that our objective being to build and continue building for the long term the value of our company, we as a founder and so Ferrari has always made clear we want to make sure that we manage well demand and that we keep disciplined in terms of how we manage demand.

Boohoo reported its preliminary results for the year ended last February. Revenues increased +41% in the year, +36% in the last quarter. UK and US did well, while Europe was weak. EBITDA margin was 30bps lower than last year. Boohoo expects a slowdown in sales in the next quarters as full-year 2021 guidance is +25% sales growth. They are also including a 5% boost from the brands they recently bought. Consensus had expected higher growth.

Deutsche Post raised guidance - again. We discussed how the logistics sector is booming last week.

Novo Nordisk's sales increased by 7% and operating profit by 3% in the first three months of 2021. For the full-year 2021, they are expecting a 6-10% increase in sales, and a 5-9% operating profit growth.

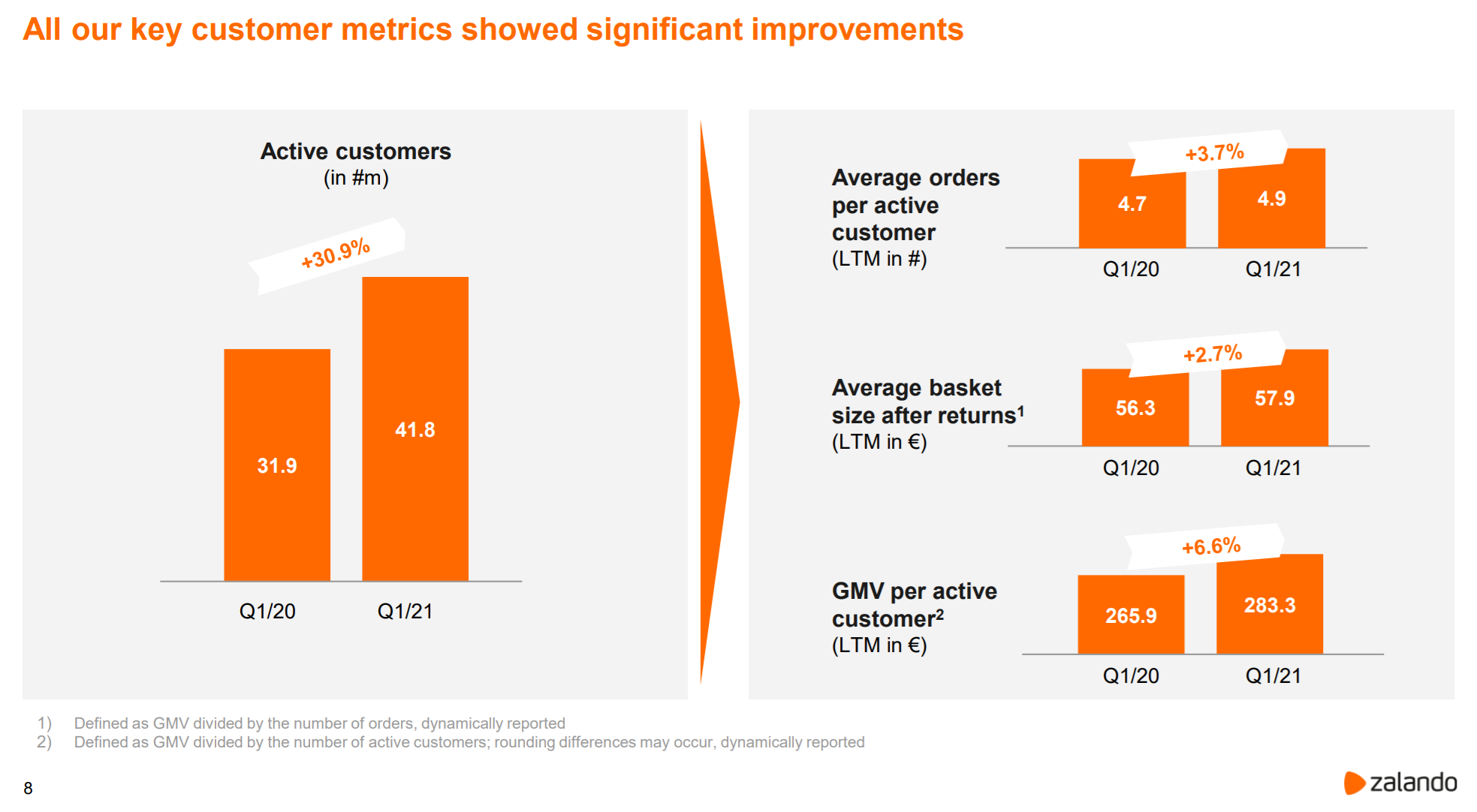

Zalando reported its Q1 numbers - the strongest growth since IPO - and upgraded the full-year 2021 guidance. When the company upgraded the Q1 guidance last month, many expected an upgrade of the full-year figures with this week reporting. They were right. In the first quarter, GMV increased 55.6% to 3.2 billion euros and they reached 41.8 million active customers, +31% since last year. The new guidance:

Zalando expects 31-36% GMV growth and 400-475 million euros adjusted EBIT for financial year 2021…

…revenues to grow 26-31% to 10.1-10.5 billion euros and an adjusted EBIT of 400-475 million euros in the same period.

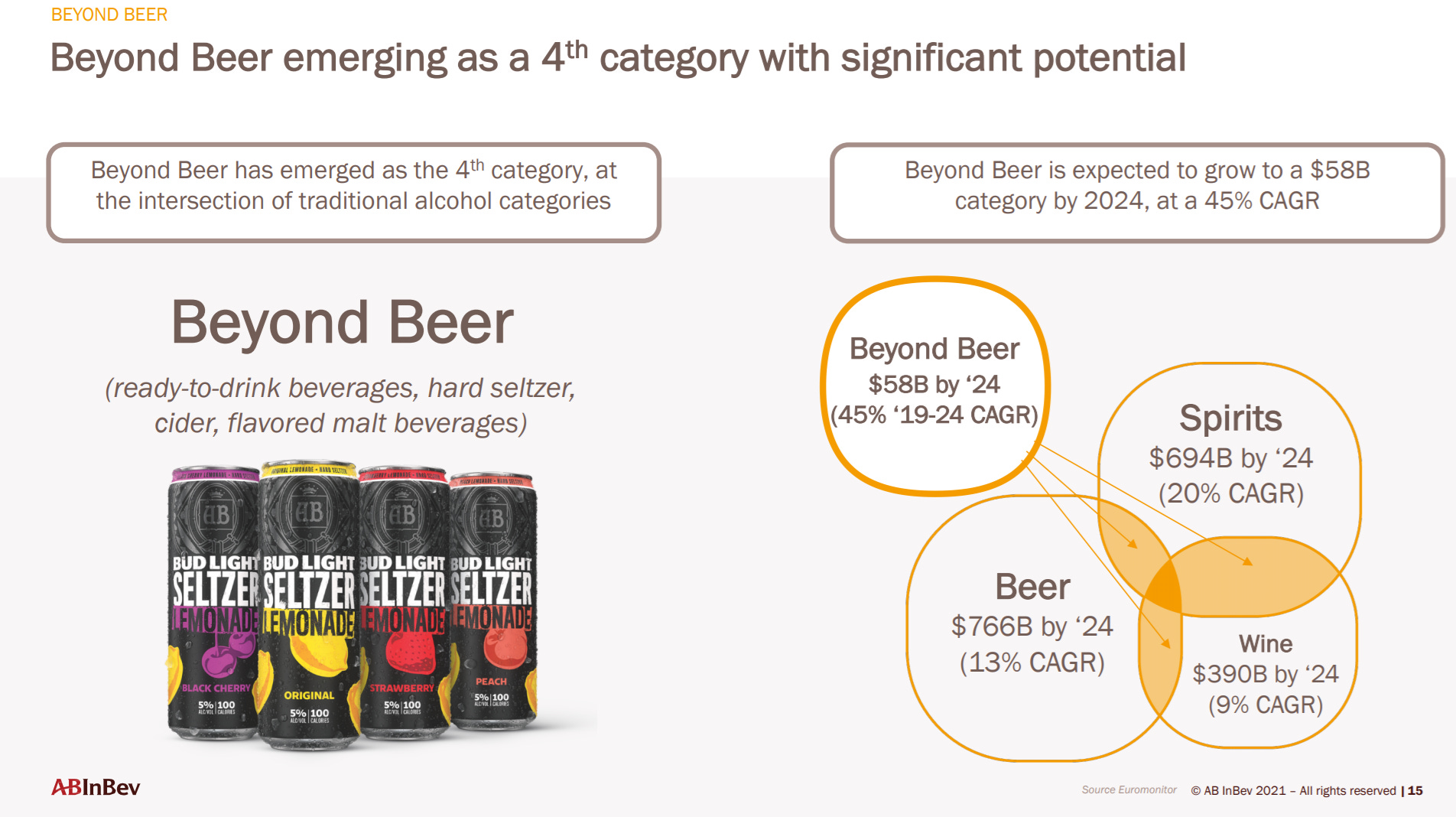

The beer giant AB InBev reported a +17.2% increase in sales in Q1 2021 compared to last year. The premium portfolio is growing faster, +28%. Beer volumes increased +13.3% compared to last year and returned +2.8% above Q1 2019 level. Non-beer categories, or as they call them “Beyond beer”, are growing even faster but they are still small, only low single-digit of total sales. Beyond beer is expected to grow at a +54% CAGR by 2024, compared to beer at +13%.

As for the full-year 2021, AB InBev is guiding for a 8-12% organic EBITDA growth.

Carlos Brito is stepping down after 32 years in the company and 15 as CEO. He will be replaced by Michel Doukeris, current head of North America. If you are interested in his story, Brito was in Patrick O’Shaughnessy podcast earlier this here:

Next’s retail sales are coming back as UK stores reopened. The company issued a trading statement this week. Sales guidance remains unchanged (+3% vs 2019) as "evidence from last year suggests that this post lockdown surge will be short lived".

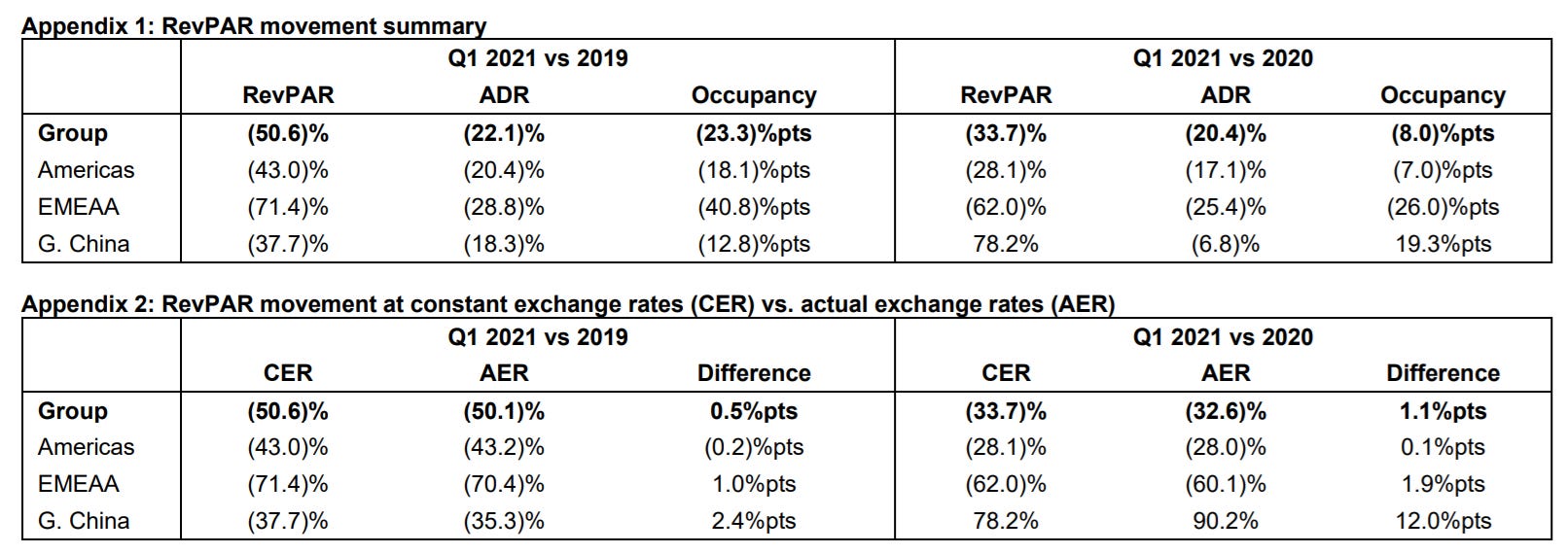

InterContinental Hotel Group RevPAR is still 50.6% below Q1 2019 level, but slowly improving. Mainly thanks to Americas and Greater China.

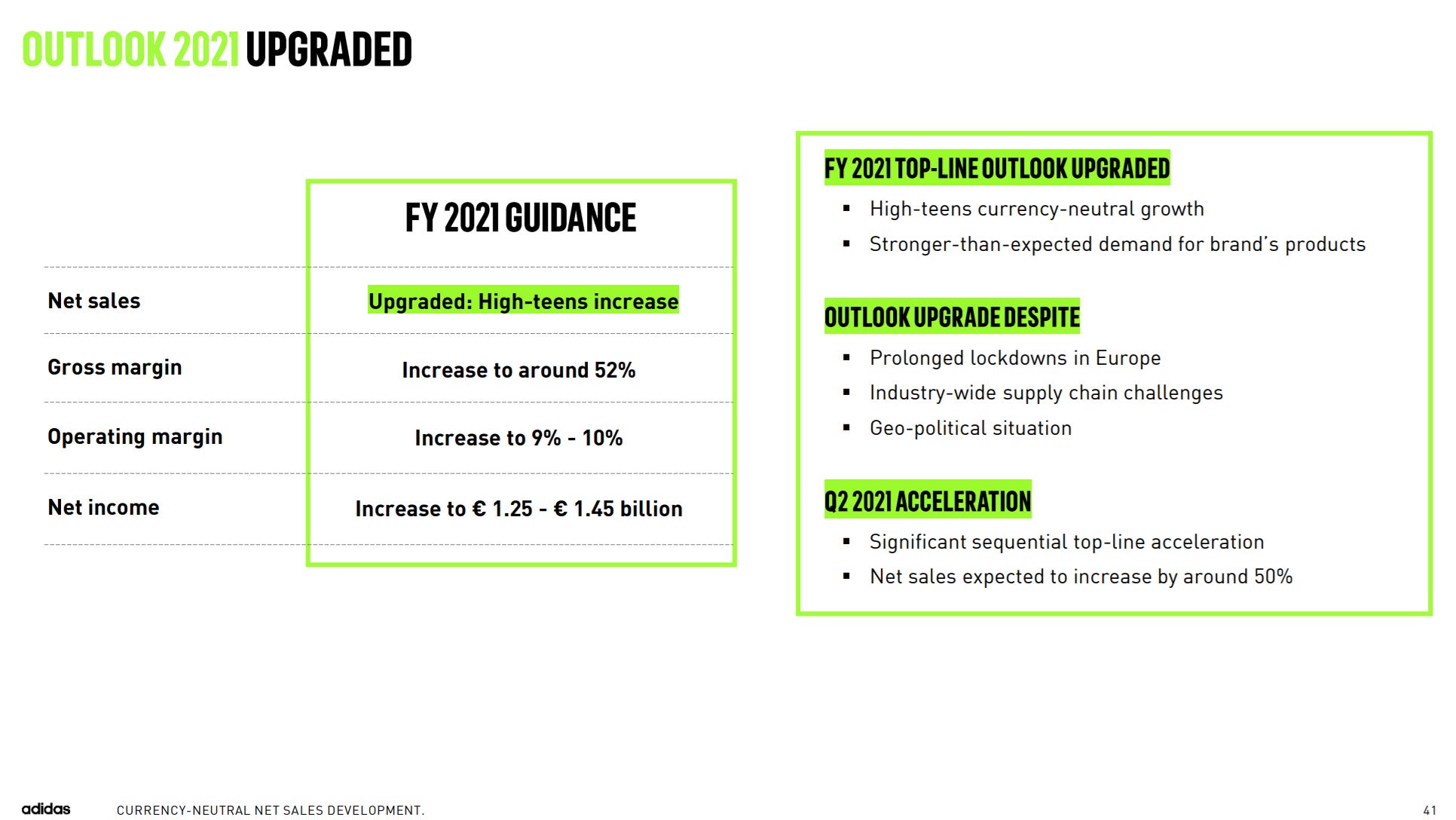

Adidas reminded us we should not trade headlines. The Chinese boycott scare was…a scare. Adidas reported strong numbers for the first quarter of 2021 and raised the full year guidance. They now expect net sales to grow high-teens compared to mid-to-high teens before (March).

M&A and IPO

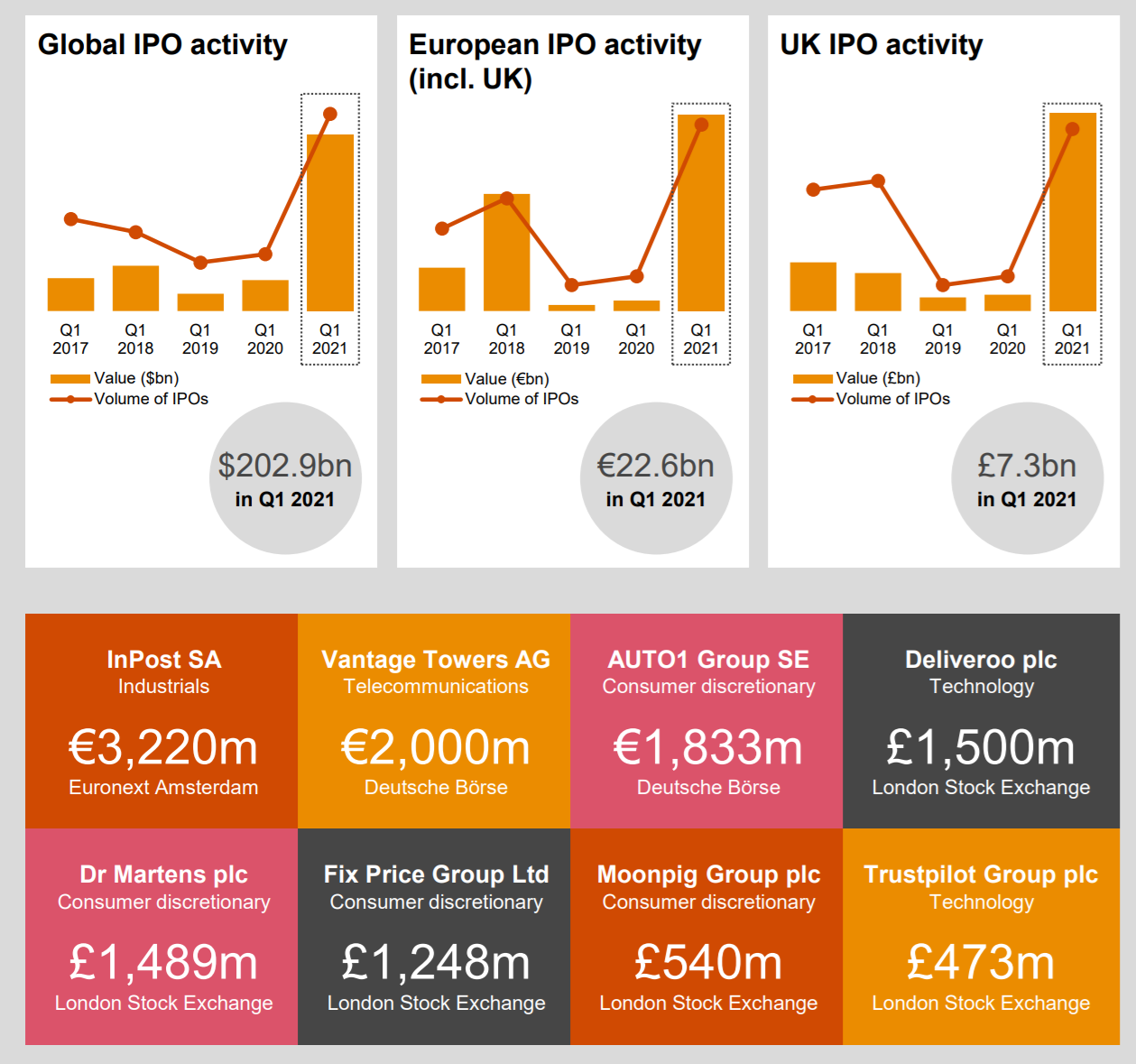

The European IPO market is having a great year so far. According to PwC, the first quarter of 2021 marked the best first quarter since…2000 (!) and surpassed the full year 2020 IPO issuance levels:

More deals coming…

Hg-backed MeinAuto sets IPO range (link)

Alphawave, Holders Seek $1.1 Billion in London Tech Listing (link)

Software firm SUSE seeks valuation of nearly $7 billion in IPO (link)

Montana Aerospace plans $481 mln Swiss IPO (link)

I wrote about behavioural biases and investing:

Have a great week and good investing!

If you are not a subscriber, please sign up to get full access and never miss an update.

Disclaimer: this newsletter is for informational purposes only and does not represent investment advice. I might have a position in some of the stocks discussed. Always do your own research before investing. Contact me on Twitter for any feedback or if you notice a mistake!