Investing in Europe #6

Investing in Europe #6

Ocado, L'Oreal, Swedish Match, Pernod Ricard, Heineken, RELX

Hello. Welcome to Investing in Europe, a weekly newsletter on what’s happening in European companies and markets, filtered for what matters.

I have been investing in Europe for over a decade and here I share some of my thoughts. You can find me on Twitter.

This newsletter is for informational purposes only does not represent investment advice. Always do your own research before investing.

Subscribe to get full access and never miss an update.

Reporting season

Ocado had a great 2020. Group revenues increased by a third. The UK retail business grew by 35% while International Solutions started to show some revenues, as the first international CFCs1 were opened.

With a 15% share of the UK online grocery market, the Ocado Retail is the most developed part of the group today and accounts for a multiple of group profits. 2020 was an extraordinary year as the online share of grocery sales nearly doubled to 14% in the UK, an ongoing trend accelerated by the pandemic. Ocado had to limit capacity and focus on key customers. You can see what happened in the table below: the average basket size increased by almost 30% and the frequency went up 3%, while the number of active customers went down. They are expanding, adding 3 new CFCs which will add 40% more capacity when fully operational.

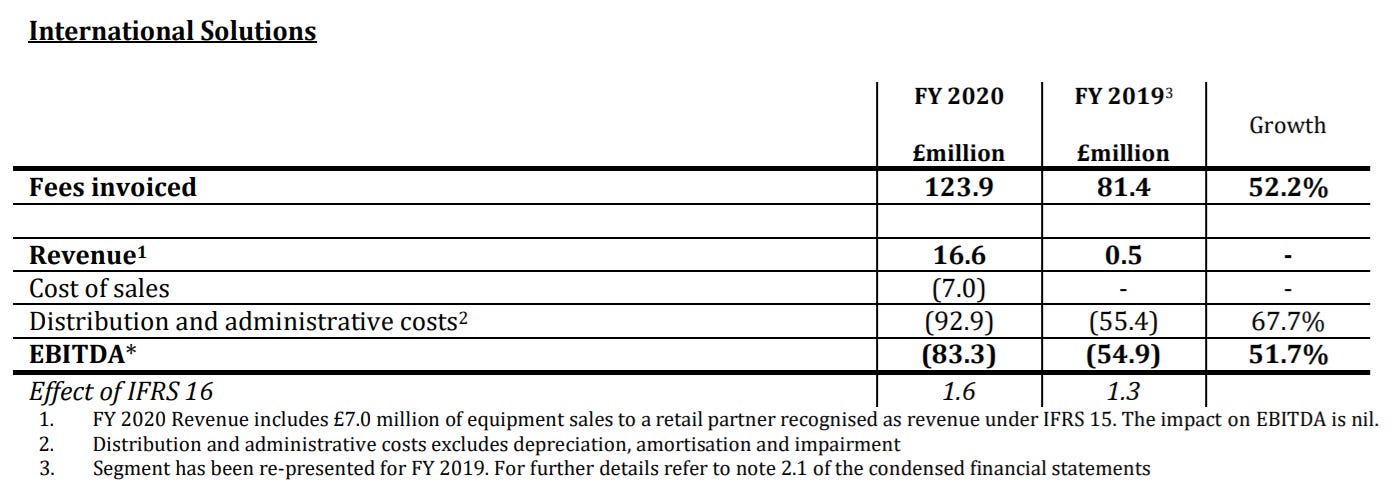

The International Solutions business is in its infancy and the key driver of future growth. Casino in France and Sobeys in Canada were the first international partners to open a CFC last year. Fees invoiced increased by 52% and are expected to grow 30% in 2021.

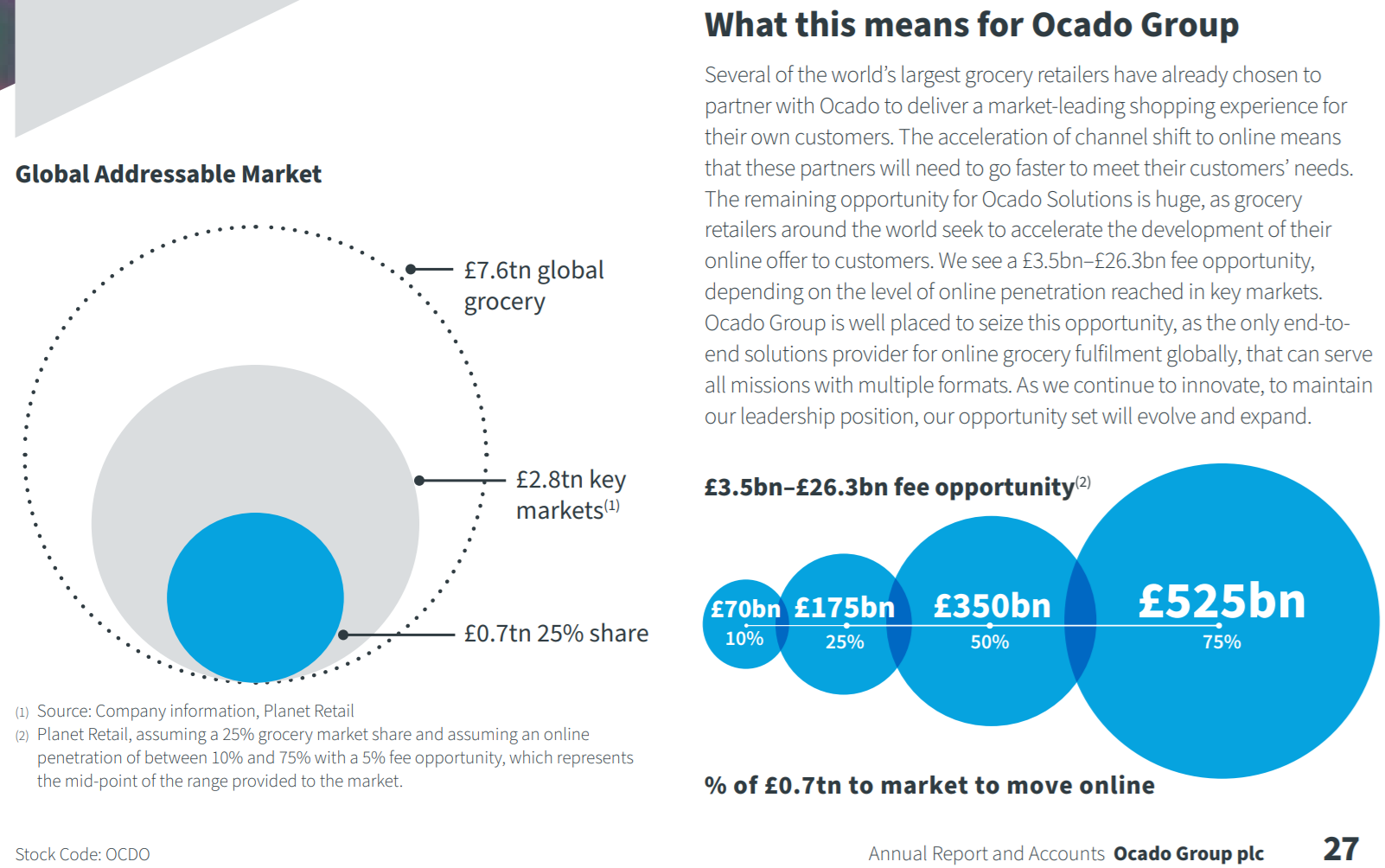

Ocado is not an easy stock to value. You can make your assumptions on the UK retail business with a certain degree of confidence. But what is the value of the International Solutions business? As you can see below, the addressable market is huge and Ocado sees a £3.5bn-£26.3bn fee opportunity.

L’Oreal sales declined -4.1% like-for-like last year. Ecommerce helped to offset the impact of stores closures:

Thanks to its strength in digital and e-commerce, which has again increased considerably during the crisis, L’Oréal has been able to maintain a close relationship with all its consumers and compensate to a large extent for the closure of points of sale. As a result, sales achieved in e-commerce 5 rose sharply by +62% 1 , across all Divisions and all regions, reaching the record level of 26.6% of the total Group’s sales for the year.

Ecommerce went from less than 16% to almost 27% of sales in one year. In the same period, Nestle went from less than 9% to more than 12% online in 2020. Unilever from 6% to 9%. P&G from 8% to 10%. Online penetration is even lower for spirits companies, at low single-digit. Selling cosmetics online is easier than food or beverages. Still, 27% is quite an impressive number.

Swedish Match sales from product segments grew by 17% last year, at constant currency. This is one of the fastest-growing consumer staples business in Europe. You would not expect that from a 106 years old company.

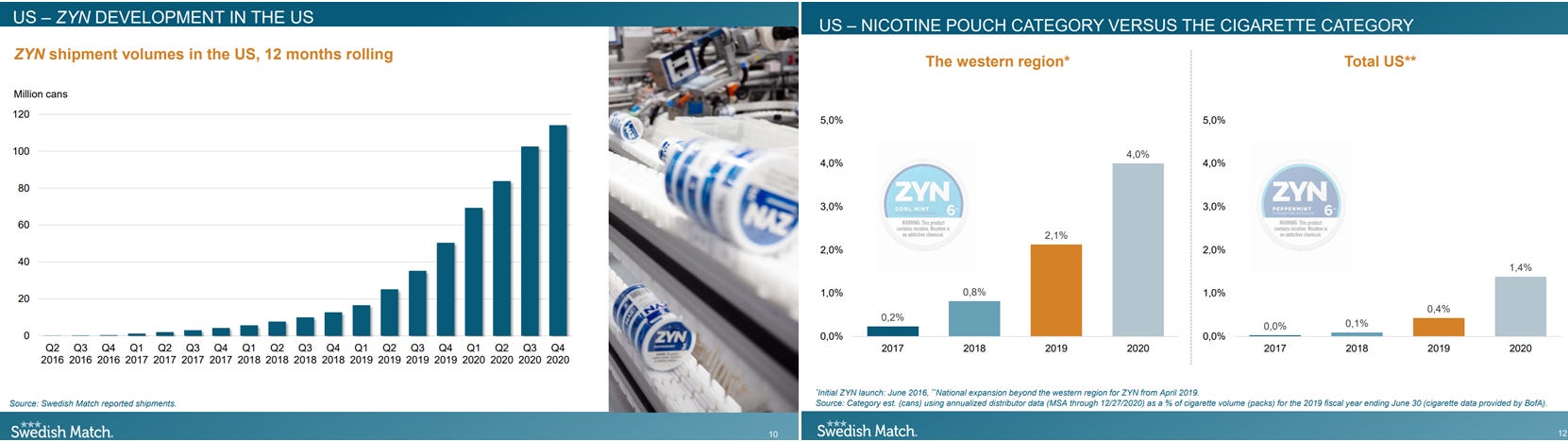

How are they growing this fast? The Smokefree segment (70%+ of the group’s operating profits) was the largest contributor to growth, with sales up 23% at constant currency. A few years ago Smokefree was about snus and Scandinavia. Today is about nicotine pouches and the US. Launched in 2015, ZYN nicotine pouches reached more than 114mn cans in 2020, more than doubling compared to 2019. Nicotine pouches are expected to continue to grow rapidly as customers switch from cigarettes and traditional oral tobacco. The category represents only 1.4% of the cigarette in the US, but already 4% in the western region where ZYN was initially launched.

Growth is only part of the equation in investing. You also need to make good returns on the capital invested. Swedish Match ticks that box too. Finally, you need a decent valuation. What about that? Make your own assumptions, but for a good framework, you can read @LibrarianCap’s article below. It also explains the negative market reaction and the long term potential return.

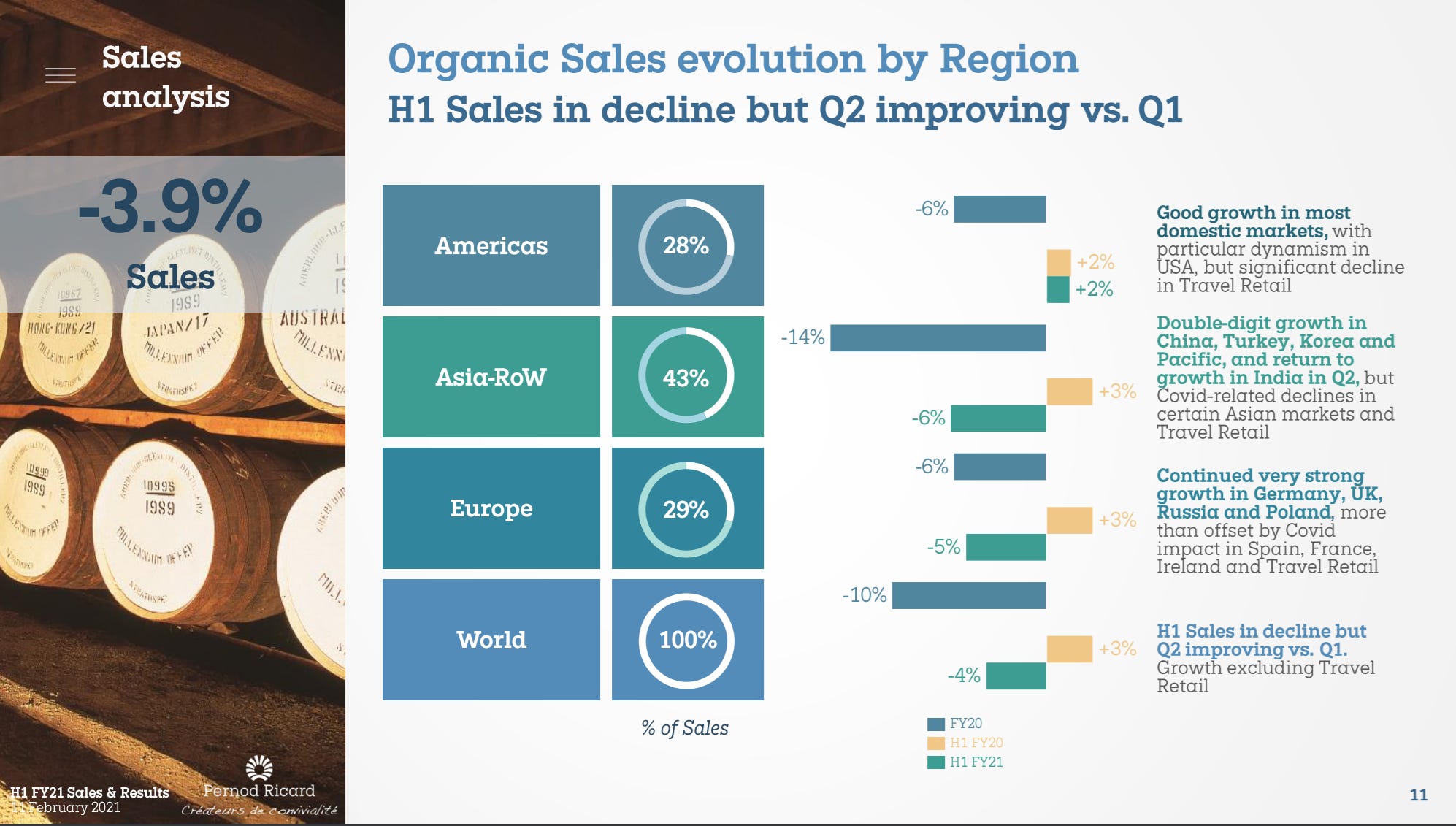

Pernod Ricard H1 (Jun-Dec 2020) sales declined -3.9% organically, with Q2 improving to -2.4% compared to -5.6% in Q1. Excluding the disrupted Travel Retail channel, sales were up +1%. Americas was the strongest region, growing +2%. They expect sales growth to be positive for the year.

Heineken organic revenues declined 12% with beer volume than 8%. They see a slow recovery of the on-trade channel in Europe, and expect to achieve an operating profit margin of around 17% by 2023.

RELX: 95% of the business continued to grow despite the pandemic. The remaining 5% is exhibitions, which has been severely disrupted.

Other news

CD Project was hacked

Another shareholder putting pressure on Danone

Vivendi will spin out Universal Music Group

The travel company TUI expects to run at a 80% capacity this summer. Some analysts think it is “optimistic”

The UK is discussing an online sales tax

M&A

Dialog Agrees to $6 Billion Takeover by Renesas Electronics (link)

Platinum drops Marston’s takeover bid (link)

Lonza strikes $4.7B deal to offload specialty ingredients business to Bain Capital, Cinven (link)

Thank you for your time and have a good week!

Customer Fulfilment Centres