Investing in Europe #27

Investing in Europe #27

Grocery robots. Another DHL upgrade. Twitter loves Aperol and more

Welcome to a new issue of Investing in Europe, a weekly curated newsletter on what’s happening in European companies and markets. Your feedback is very important. Please comment below or DM me on Twitter. If you are not a subscriber, please sign up to get full access and never miss an update. 🙏

Welcome new subscribers 👋 - thank you Ray 🙏

Dear friends and investors, this week I would like to start by thanking Ray for sharing my Substack. Twitter is a great place to meet thoughtful investors and Ray is a great person to interact with. For those of you who are still not following him, please do.

100+ of you subscribed to this newsletter after this tweet. My warmest welcome to every one of you. I hope you will find this newsletter useful and become a better, more informed investor.

You might still wonder: “ok, I received my welcome message but what have I subscribed to?” 🤔 Investing in Europe is a free, weekly newsletter focused on European companies. You will find mainly good businesses, stocks you might want to buy and hold at the right price, but also not so great businesses that might help you to understand what’s going on. It is about fundamentals, and while you will find plenty of quarterly earnings, the focus is long-term: “a journey of a thousand miles begins with a single step” and every step matters, I might add. So far, you will mainly find company updates and high-level commentary. Eventually, I might add some longer write-ups.

Please comment below or reach out for any feedback!

Disclaimer: this newsletter is for informational purposes only and does not represent investment advice. I might have a position in some of the stocks discussed. Always do your own research before investing.

Company news and results

Ocado reported its first-half results (December 2020 - May 2021). As a reminder, Ocado today is a combination of two businesses:

Ocado Retail - an online UK grocery retailer. This is how the business started and still the main source of cash

Ocado Solutions - an online grocery solutions provider. They are basically exporting their smart platform to other grocers (see Kroger) that want to optimise the entire online grocery delivery process. This is the key driver of future growth, but still in a development phase

The UK business boomed during the pandemic. You can find a quick recap here. As we reopen, the UK retail business continues to grow but the mix is changing, with the average basket size down and orders per week up.

In the first half of its fiscal 2021, Ocado Retail’s sales were almost up 20% year on year. The average basket size is normalising as we are no hoarder anymore: it was flat for the first half of the year compared to 2020, at £138, but down 23% in the second quarter (Mar-May 2020). Orders per week jumped +40% in Mar-May and were up 20% in the first half. Last year, Ocado had limited capacity to satisfy its customers demand but now capacity is increasing. They are adding in excess of 40% more capacity in the UK, with three new Customer Fulfilment Centres (CFCs) compared to 2020, one already operational from February. EBITDA% was 8.5% compared to 4.5% last year, thanks to sourcing benefits and better efficiencies.

The UK Solutions and Logistics business total potential capacity should increase to around 750k orders per week. As for the International Solution business, Ocado has now four operating CFCs outside the UK as Kroger launched last April. 8 more should go live from 2022. On a separate note, Ocado announced an agreement with Alcampo (Auchan group) in Spain.

Overall, at the group level, EBITDA tripled while operating cash flow was steeply down due to working capital investments. The full-year outlook has been maintained, despite higher investments.

Online grocery is here to stay and get bigger. Ocado seems to have a strong competitive advantage in the big warehouse business. The question is which business model will prevail, who will win. Ocado's CEO commented the immediacy offer (Getir, GoPuff...Ocado as well with Zoom) is interesting but "tiny market compared to the opportunity for the big warehouses".

An Ocado warehouse in South-East London

Fun fact: the 3D camera in the video is the Xbox Kinect 2.0, which wasn’t great for gamers but found new uses.

As for the (mostly) offline supermarkets, Sainsbury reported a +1.6% like-for-like increase in sales ex-fuel in the Apr - June quarter. Grocery was up +0.8%. Not much growth and no inflation here so far:

From today we are reducing prices by £50 million on everyday products from strawberries and cherries to bacon and potatoes, helping customers make the most of this summer

Sartorius, the pharmaceutical and laboratory equipment supplier, raised its forecast for the full year of 2021. They increased their topline guidance from +35% to +45% year-on-year growth, EBITDA margin from 32% to 34%.

The UK pub chain Wetherspoon issued a trading update: like-for-like sales from 17 May to 4 July, when pubs were fully open, were -14.6%. There is a negative impact from the Euro 2020 tournament, as numbers were -8.1% before it started. They televised only a few matches. Guidance: their best estimate for the next financial year (Jul 2022) is for sales to be in line with 2019 levels.

European auto manufacturers are stepping up their investments in electric vehicles. Stellantis, the company born from the merger of FCA and Groupe PSA, had an investor day focused on EV. They plan to invest more than €30bn and target over 70% of sales in Europe and over 40% in the US to be low emission vehicles by 2030. By comparison, this year numbers are respectively 14% and 4%. Stellantis aims to achieve double-digit adj operating income margin from electric sales by 2026.

Deutsche Post raised its guidance - again. I lost count but it seems this is the 5th time in a row they are increasing their outlook. 2021 EBIT is now expected to be in excess of €7bn (from €6.7bn), while Free Cash Flow more than €3.2bn (from €3bn). I have briefly discussed before what is happening in the logistic sector and showed how companies like DSV, Kuehne + Nagel, Deutsche Post itself and the shipping companies are having their best time. Simply put, supply chains remain disrupted and demand-supply unbalanced. How long will it last? The US administration is watching.

Volume trends persisted with B2C shipment volumes remaining on high levels and ahead of last year in all networks while the recovery in the B2B businesses continued. At the same time the tight capacity situation both in Ocean and Air Freight markets continued.

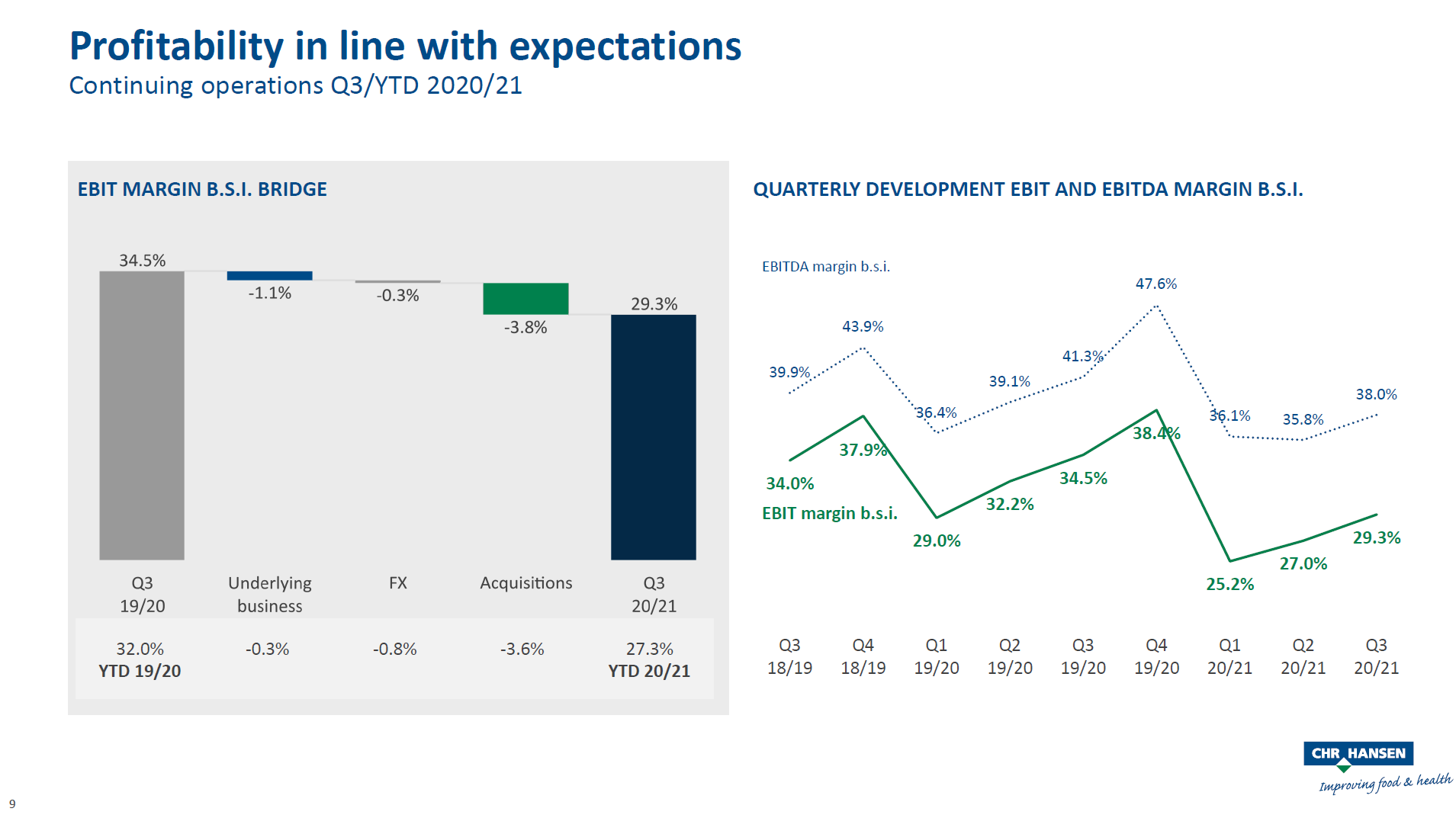

Chr. Hansen, which specialises in cultures and enzymes, reported its Q3 2021 results (Mar-May 2021). Organic sales growth decelerated from +10% last quarter to +4%. The full-year guidance has been maintained but M&A contribution increased, so there was an underlying downgrade. The Human Health division (dietary supplements and infant formula) was weak.

We remain on track to deliver on our ambition for the year and the outlook therefore remains unchanged. The overall outlook for Human Health remains positive but a changed mix between organic and acquisition driven sales which will keep Group organic growth below our original expectations in Q4

Chr. Hansen expects full-year 2021 organic growth in the 6-8% range, EBIT% before special items at 27-28% and free cash flow at €140-160mn.

The value retailer B&M issued a trading update. The UK business like-for-like revenues are slowing down but are still up +21.3% on a two-year stack.

Deliveroo issued an unscheduled positive trading update. Orders were up 88% year-on-year in Q2, with Gross Transaction Value (GTV) up 81% in constant currency. Deliveroo upgraded its GTV guidance from +30-40% to +50-60%, but gross profit margin is now expected in the lower half of the previous guidance of 7.5-8%, due to investments. The stock had quite a strong squeeze lately but is still trading 14% ca below the IPO price.

M&A and IPO

Wise started trading in London, now a good place to list tech companies after it was a bad place when Deliveroo listed 🤔. Stripe’s co-founder John Collison commented:

Philip Morris announced the acquisition of Vectura Group, a “provider of innovative inhaled drug delivery solutions” (link)

Rimac takes over Bugatti from Volkswagen (link)

Everyone wants the British supermarket Morrison (link) 🤷

Kering buys high-end Danish eyewear brand Lindberg (link). Kering made €600mn sales in luxury eyeware pre-Covid and its eyewear’s CEO Vedovotto thinks the market is worth €4bn.

Other news

Bulgari opens in Place Vendome (link)

What I learned from my most popular tweet: Twitter loves Aperol

If you are still reading, you deserve a Spritz!

Have a great week and good investing!

If you are not a subscriber, please sign up to get full access and never miss an update.

Disclaimer: this newsletter is for informational purposes only and does not represent investment advice. I might have a position in some of the stocks discussed. Always do your own research before investing. Your feedback is important - please contact me on Twitter